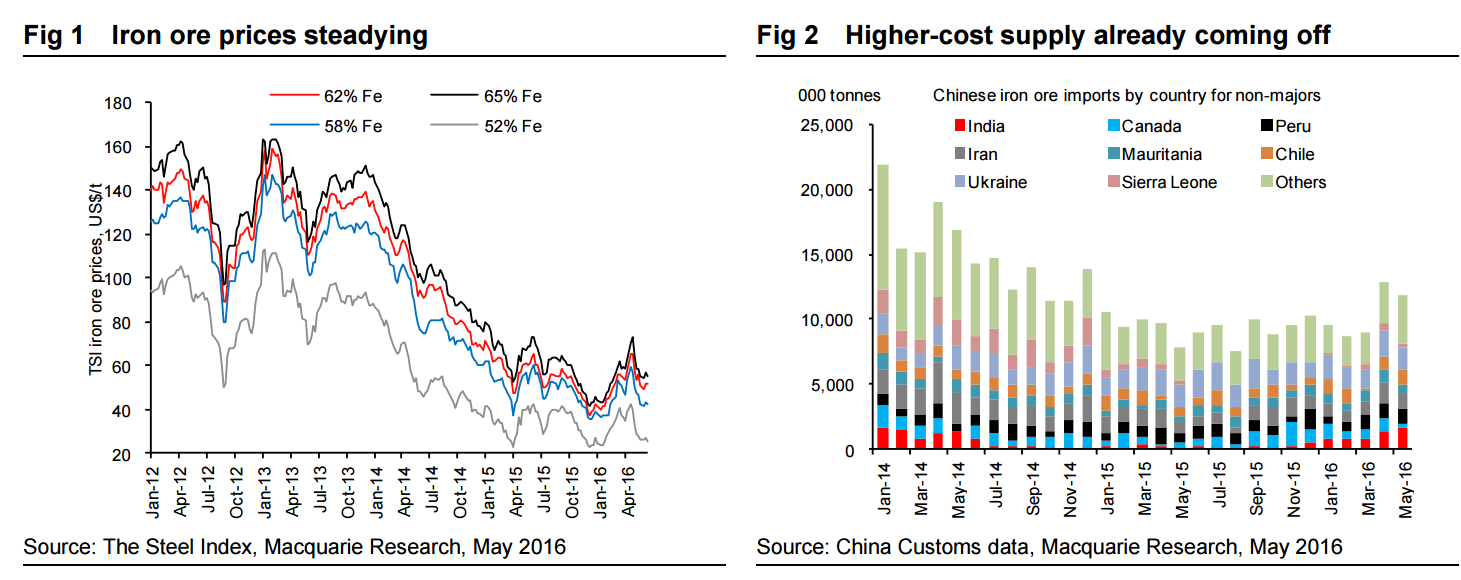

Spot iron ore prices have steadied in a $49–53/t CFR China range (62%fe basis) since late-May. While this is down sharply from their most recent peak of $68.7/t on April 21, according to data from The Steel Index, we believe the risks of a near-term collapse below $50/t have abated due to a continued, gradual destocking at steel mills and the quick disappearance of higher-cost iron ore supply that reappeared in the market in early-2Q16 in response to the price jump.

Iron ore imports in May rose to 86.8mt, their highest this year, and YTD imports are up 9% YoY. However, imports excluding Australia, Brazil and South Africa eased back to an annualised rate of 139mt, down from 156mtpa in April, with notable falls from Ukraine, Iran, Mauritania and Canada. As we highlighted last month, there had been a very quick response from some higher-cost suppliers to the price recovery in early-2Q16, as imports excluding Australia, Brazil and South Africa increased from an average run rate through 1Q16 of 110mtpa.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.