Former Treasurer and Prime Minister Paul Keating has hit back at commentators that have claimed that he would back the Coalition’s company tax cuts, penning a strongly worded letter-to-the-editor in The AFR arguing that the Turnbull Government’s plan is unaffordable:

“Yes, I did cut the company tax rate from 49 per cent to 33 per cent but paid for those vast reductions by a massive broadening to the base of the tax system: capital gains taxation at full marginal rates, a comprehensive fringe benefits tax, the abolition of entertainment as a deduction, tax on company cars etc.

Tax reductions are desirable provided they are affordable. But I would never have countenanced a $50 billion impost on the budget balance with a discretionary unfunded tax cut.

The AFR has embarked upon this campaign in collusion with the Business Council of Australia, in the council’s camouflaged attempt to reduce the rate of company tax on foreign shareholdings. The AFR must be alone among national financial newspapers in urging so massive an impost on the national fiscal balance”.

Paul Keating has previously noted that cutting company taxes primarily benefits overseas investors. This is because the benefit of any company tax cut to domestic owners/investors would be offset by a commensurate reduction in imputation credits. By contrast, overseas investors who do not receive imputation credits would benefit fully from any company tax cut.

Here’s Paul Keating’s explanation:

“Australia’s dividend imputation system works such that the company tax is, in effect, a withholding tax – a tax temporarily held by the Commonwealth which is returned to shareholders when their dividends are paid. So, whether the company tax is withheld by the Commonwealth at a rate of 30% or 25% is immaterial – the Commonwealth is going to return the money to shareholders anyway, regardless of the rate. But the shareholders who will receive a benefit are foreign shareholders”.

Hence, a company tax cut would primarily benefit foreigners, and by extension larger corporations at the expense of small businesses. This is because around 98% of small businesses (i.e. those employing four or less people) are wholly Australian owned and, presumably, indifferent to slashing the company tax rate. By contrast, 30% of large companies (i.e. those employing more than 200 people) are at least partly owned by foreigners, who would be the primary beneficiaries from the Coalition’s policy.

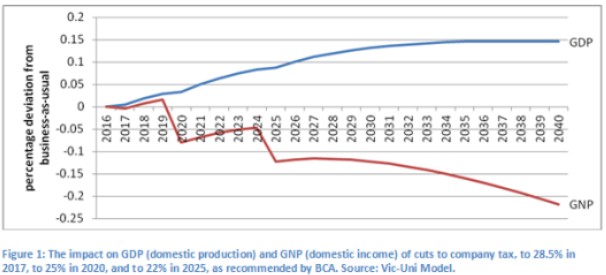

Indeed, recent modelling from Janine Dixon from the Centre of Policy Studies at Victoria University showed that cutting company taxes would actually reduce national income – the best measure of living standards:

Again, this is because foreign shareholders would benefit most from a company tax cut, reducing the income (welfare) of Australian residents.

Given foreigners would be the main beneficiaries of a company tax cut, and local residents would be made worse-off, why should we support it?