Fortescue is out with some more good news today:

Fortescue has continued its program of debt reduction, wiping $US500 million from a 2019 secured loan and reaping interest savings of $US21m as a result.

The move is the latest of several by the iron ore miner (FMG) to address its debt load within an iron ore market that has bounced off lows in recent months.

Fortescue made two repayments either side of the end of April that reduced debt by $US1.28 billion.

“Cashflow generation from our operational performance and cost reductions have allowed Fortescue to continue to repay debt,” Fortescue chief financial officer Stephen Pearce said.

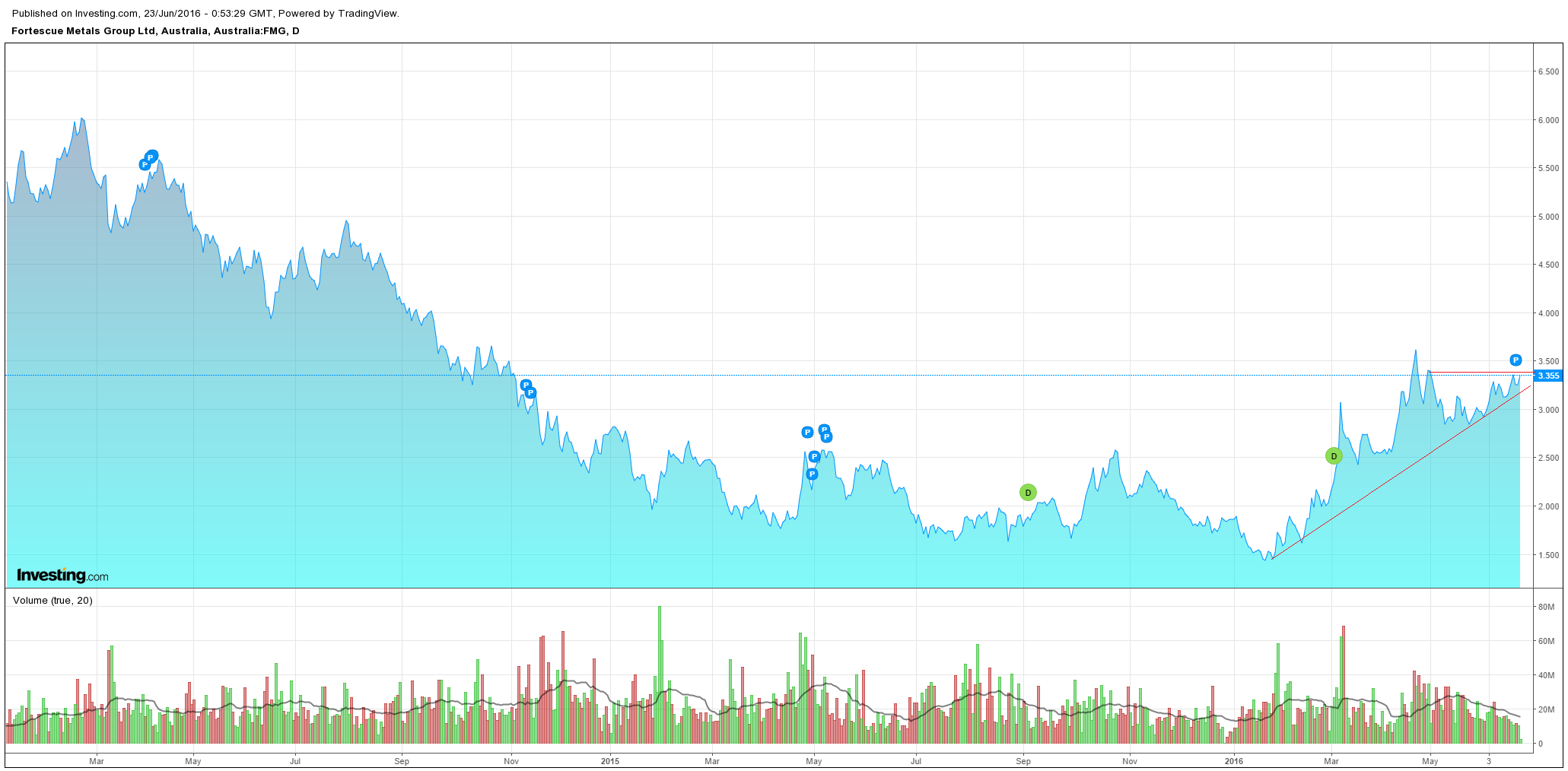

The share price is off to the races again today and it’s chart continues to form up a bullish ascending triangle pattern:

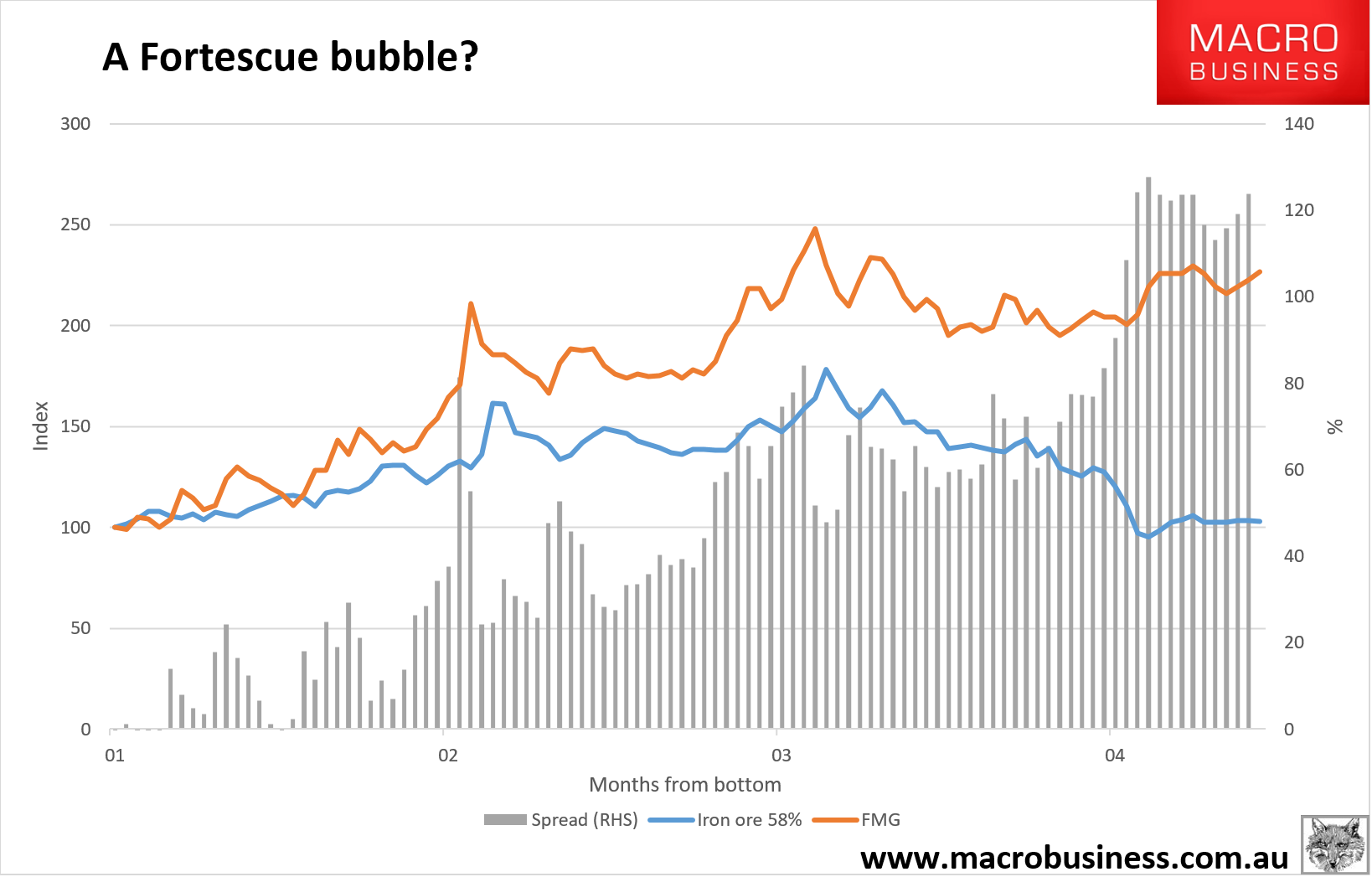

This is transpiring while the opposite happens to its iron ore sales price. The following chart includes its recent mushrooming grade discounts as it competes with the return of lower grade ores from India:

The share price is up 120% from the lows but the price achieved is barely up at all. Grade discounts are cyclical and will probably fall back but they also tend to persist as cycles turn which is where we are now. A glance at the company metrics on Bloomie fills out the picture. Consensus forward price earnings ratios are:

- 2016 24x

- 2017 11x

- 2018 25x

- 2019 23x

Bloody pricey already and clearly long an ongoing iron ore recovery which is quite unlikely given China’s stimulus is peaking as we speak and will fade through H2 just as:

- Roy Hill ramps up to 30mt;

- Sino ramps up to 24mt;

- India ramps up to 20mt;

- Africa ramps up to 20mt;

- S11D ramps up to 20mt.

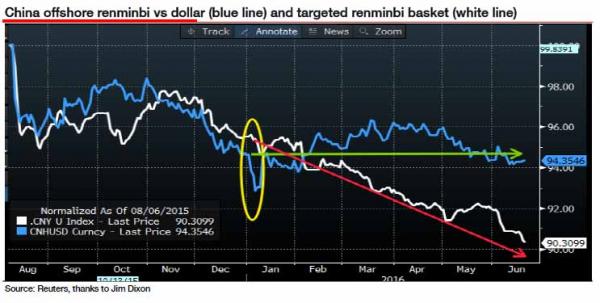

At least Samarco is delayed but only a quarter or two. Worse, the yuan has now fallen 10% against competing currencies:

So China’s own iron ore is getting more competitive including the 40mt that’s come on stream since late last year if you believe private surveys. The majors have taken roughly 60mt offline since H2 last year (including Samarco) but we’ve still got a net 90mt more ore in the market and its more competitive as well. Steel production should be better than 2015 H2 but only by 2-3% so that accounts for roughly 10mt of the new iron ore, at best.

Prices are going to fall again, especially when we add the H2 destock and high Chinese port inventories.

Yes, FMG management has done a terrific job of lowering costs but that is over now, at least until the Aussie dollar falls further and that’s not going to happen until the price of iron ore also falls again.

I personally think that the Vale JV is nonsensical once price falls resume so see no strategic game changer there, either.

The prospects for dividends are weak given the need to keep deleveraging. And the price of iron ore will keep falling as well so there is considerable balance sheet risk on the asset side.

FMG looks like a bubble to me.