MOU blending upside likely at the operational level: The plan to blend tonnes with Vale is yet to be implemented, but we have made a first pass at quantifying the upside. The scenario work suggests US$5-50mn of annual cash flow at a US$50/t index price. The real impact is likely in the operational and capex savings; the scenario work on this generates A$0.45/sh in value if each can be reduced by US$1/t over the life of the mine. This highlights the leverage effect of volume and longevity, and the risk to our UW stance.

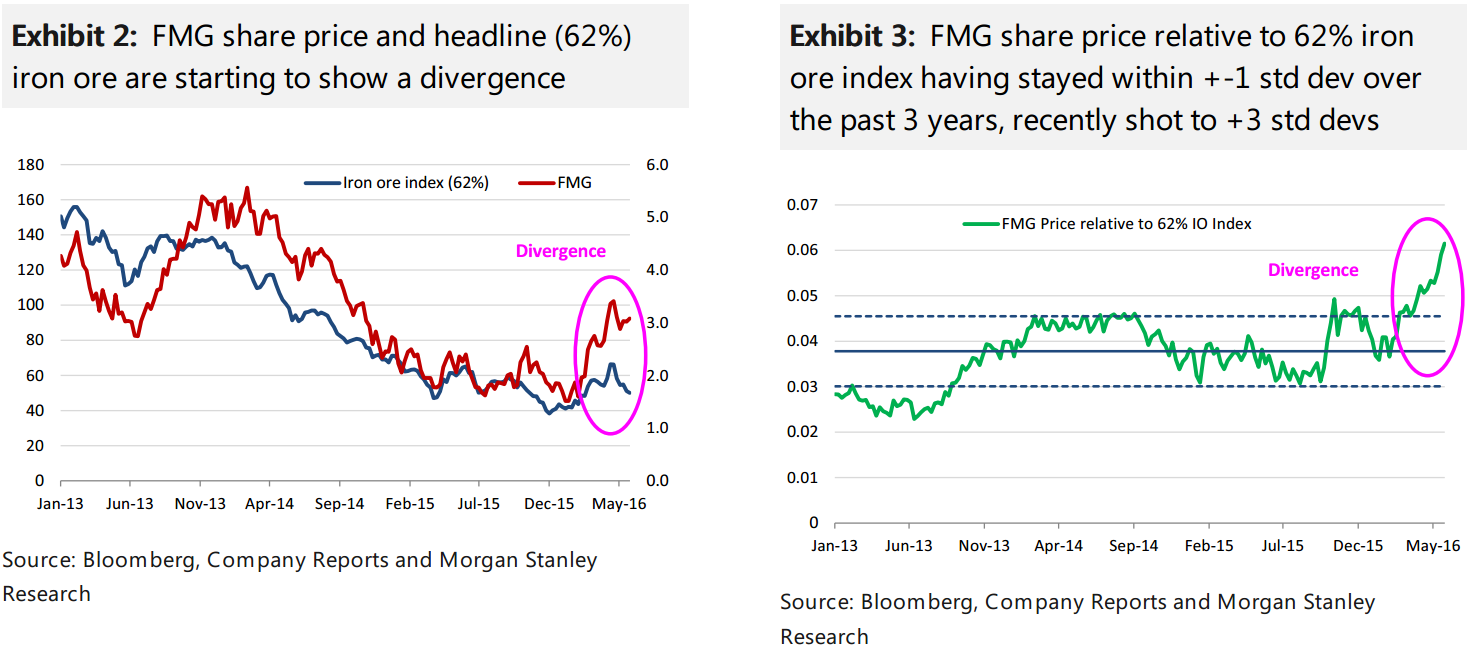

Dislocation from iron ore price unusual: The relationship between the FMG share price and the iron ore index price is diverging; the simple ratio between the two is three standard deviations from the norm (Exhibit 2 and Exhibit 3). Cost reduction has been impressive but margins are at normal levels (Exhibit 5), so we expect the equity price to move lower to be aligned with the index price. That said, the balance sheet strengthens at the current iron ore price, bringing the prospect of more debt reduction and conversion of net debt to market cap within the EV.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.