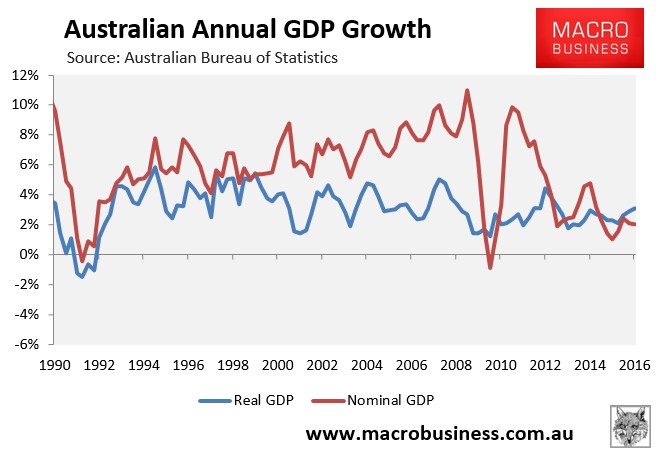

As summarised earlier, the Australian Bureau of Statistics (ABS) today released the national accounts for the March quarter, which registered a 1.1% increase in real GDP over the quarter and a 3.1% rise over the year, smashing economists’ expectations.

On a per capita basis, real GDP rose by 0.8% and was up by 1.7% over the year. But more importantly for living standards, real national disposable income per capita fell by 0.1% over the quarter and was down 2.6% over the year.

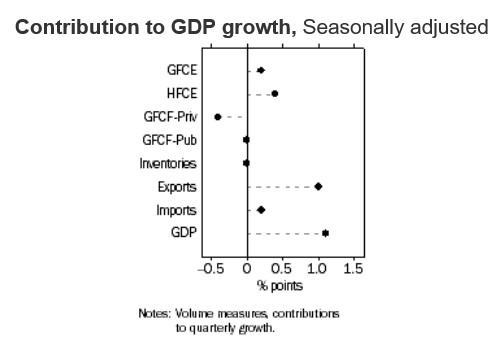

According to the ABS, seasonally adjusted GDP growth for the quarter was driven overwhelmingly by export volumes which contributed 1.0 percentage point, whereas household final consumption expenditure contributed 0.4 percentage points. These more than offset Private gross fixed capital formation which fell 2.2%.

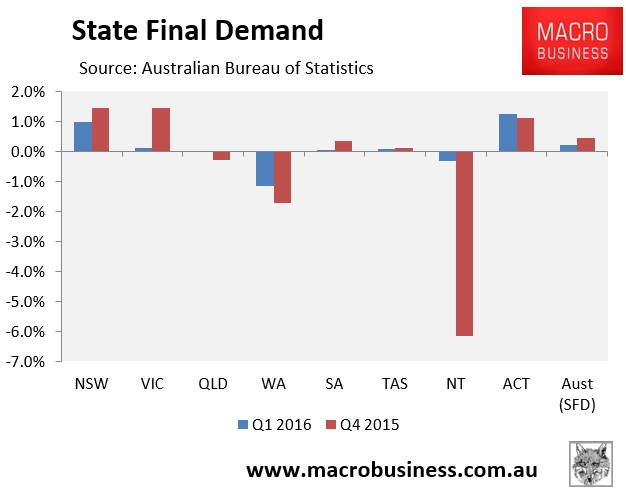

Quarterly final demand, which excludes export volumes, remains weak. It grew by only 0.2% at the national level in the March quarter, led by the housing bubble epicentres of NSW (+1.0%) and the ACT (+1.1%), with VIC (+0.1%) and TAS (+0.1%) also registering some growth. By contrast, final demand did not grow in QLD or SA, and fell in WA (-1.2%) and the NT (-0.3%):

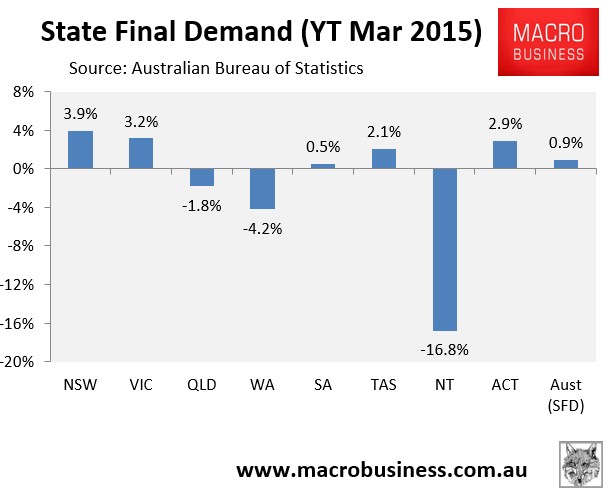

In the year to March 2016, final demand growth was also very weak (negative in per capita terms), growing by just 0.9% nationally. The bubble epicentres of NSW and VIC led the charge, whereas QLD, WA and the NT went backwards:

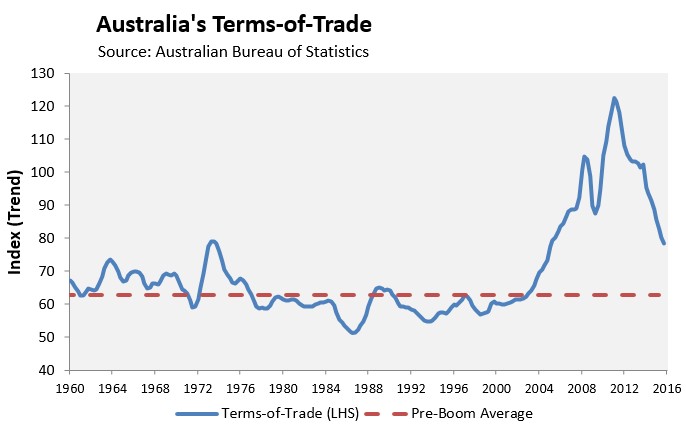

The terms-of-trade fell by a seasonally-adjusted 1.9% over the quarter and by 11.5% over the year, and is now tracking at its lowest level in 11-years, with much further still to fall:

And as expected, the falling terms-of-trade dragged-down income growth, with real national disposable income (NDI) rising only 0.2% over the quarter but falling by 1.3% over the year.

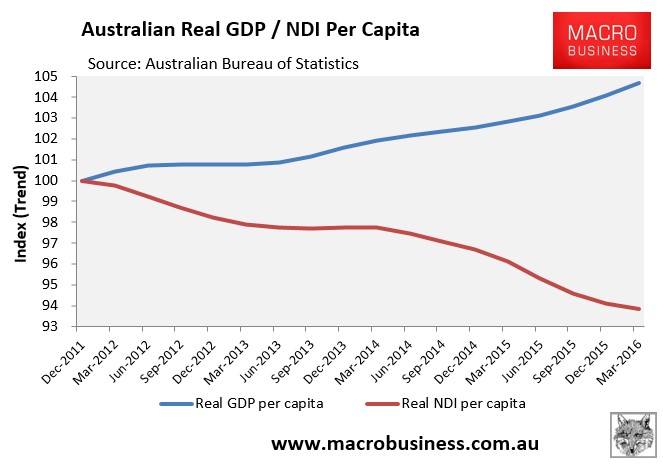

However, because of population growth, per capita NDI fell by 0.1% over the quarter and by 2.6% over the year, and will continue to be weak as long as the terms-of-trade unwinds from its current still high level (see next chart).

Indeed, the ongoing slump in per capita income – down 6.2% since December 2011 – as well as falling per capita domestic demand are the real stories of this release, not the meaningless rise in GDP volumes, which does nothing for living standards.

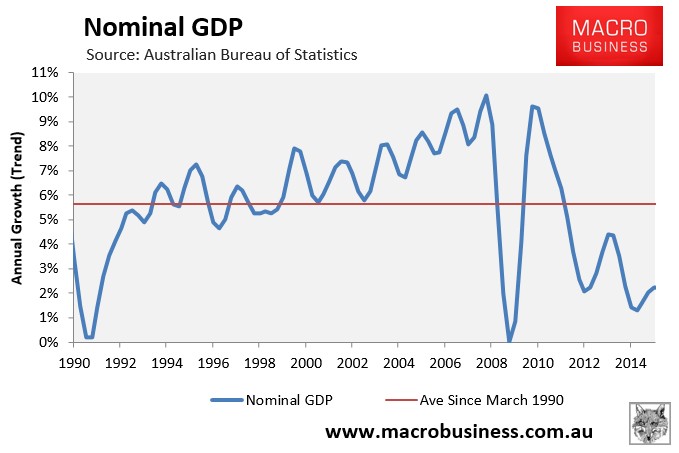

The fall in the terms-of-trade and national disposable income have also helped suppress nominal GDP, which rose by only 0.4% over the quarter and by 2.1% over the year, and is generally a negative indicator for government finances:

The below chart shows how nominal GDP is tracking well below the average since 1990, which is making things tough for the Government:

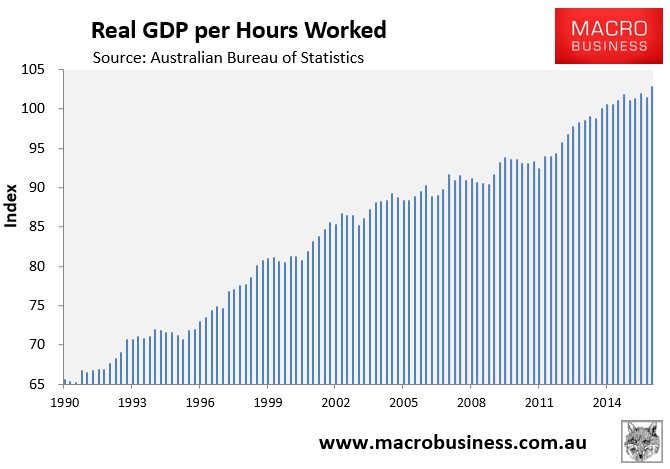

A positive from this release is that real GDP per hour worked rose by 1.4% in the March quarter and was up by 1.7% over the year, suggesting improved labour productivity:

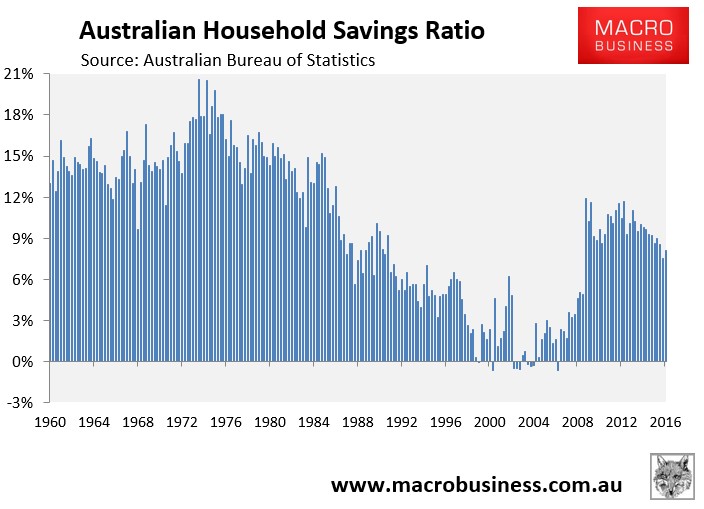

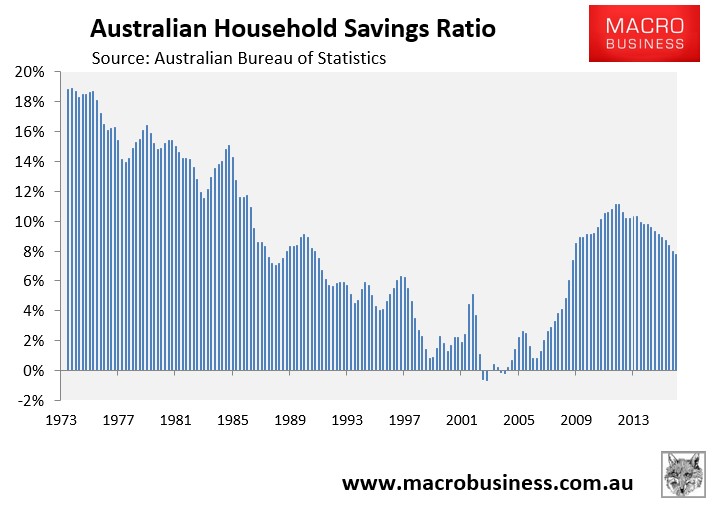

The household savings ratio also recovered to 8.1% from 7.5% in December:

Although it continues to fall in trend terms, commensurate with the ever-rising household debt:

As was the case last quarter, this is a worrying release once one scrapes below the stunning headline GDP number.

GDP volumes are being supported by rising export volumes selling at lower prices, along with housing-bubble fueled growth.

Meanwhile, the more important metrics of per capita national disposable income and domestic demand continue to shrink.

The outlook is also poor, with ongoing falls in commodity prices likely to continue dragging down per capita NDI over coming years – a trend that will persist as the terms-of-trade retraces back towards its pre-boom average.

The ongoing weak nominal GDP growth is also a bad sign for Budget revenues, which are already under immense pressure, and will haunt the next Federal Government.

What will drive the domestic economy once the bubble in house prices and construction activity inevitably reverses?