The Brent oil price is under pressure down hard from last week at $50.07. Henry Hub gas is still strong at $2.58mmBtu:

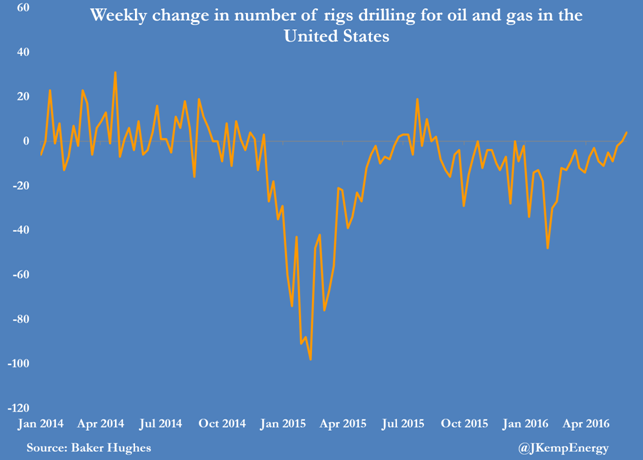

The causes of oil weakness are multiple: a firm US dollar, a rising US rig count, Brexit growth fears, impending resolution to some supply curtailments, from John Kemp:

There’s little change in either Nigeria or Libya. But Canada is slowly coming back on stream. OPEC’s monthly oil market report assessed disruptions at 1.4mbpd and it sees a balanced market by year end:

Turning to the oil market, world oil demand growth in the second half of the year is projected to continue rising by 1.2 mb/d y-o-y. The OECD is anticipated to add around 0.2 mb/d, with OECD Americas leading growth at 0.3 mb/d, while OECD Europe is seen flat and OECD Pacific contracting by almost 0.1 mb/d. Key factors impacting OECD oil demand growth will be retail price developments during the driving season and heating demand in the Northern Hemisphere by the end of the year. In the non-OECD, oil demand is anticipated to grow by 1.0 mb/d y-o-y in the second half of the year. Demand is projected to be supported by Other Asia with growth of around 0.4 mb/d y-o-y. Much of this growth is seen coming from India, where projections for macroeconomic indicators are currently solid. In China, support will come from transportation and petrochemical sectors, while industrial fuel consumption is expected to contract. On the supply side, non-OPEC supply in the second half of the year is anticipated to be some 140 tb/d weaker than in 1H16 and almost 1 mb/d lower compared to the same period last year. In the Developing Countries, supply is seen growing by 270 tb/d compared to the estimate in 1H16, which will broadly offset a 280 tb/d decline expected in OECD supply over the same period. FSU oil production in the second half is projected to decline by 200 tb/d, with Russian oil production contracting by 120 tb/d. Over the same period, China’s output is expected to increase by 60 tb/d and production in Brazil is expected to increase by 270 tb/d due to the start-up of two new projects. In the US, despite higher growth in the Gulf of Mexico, total US output will decline by 150 tb/d in the second half of the year compared to 1H16. With the recovery of production disrupted by wildfire, supply in Canada is expected to grow by 60 tb/d compared to 1H16. The above projections indicate that the excess supply in the market is likely to ease over the coming quarters. To some degree, this has started to be seen in the slowing pace of inventory builds in US commercial crude stocks (Graph 2). In May, commercial crude stocks saw a draw of around 8 mb, compared to an average 12 mb build over March and April, and a 19 mb increase over January and February. Provided that there is a clearer picture regarding oil supply and demand, the expected improvement in global economic conditions should result in a more balanced oil market toward the end of the year. In the second half, demand for OPEC crude is expected to average 32.6 mb/d.

My own outlook is less price bullish given things can hardly get worse in Nigeria and Libya and Canada is going to come back quickly:

Nonetheless, the trend is clear and barring new supply side resolution or another shock like Brexit I’d expect oil to hold $50 to inject more US rigs.

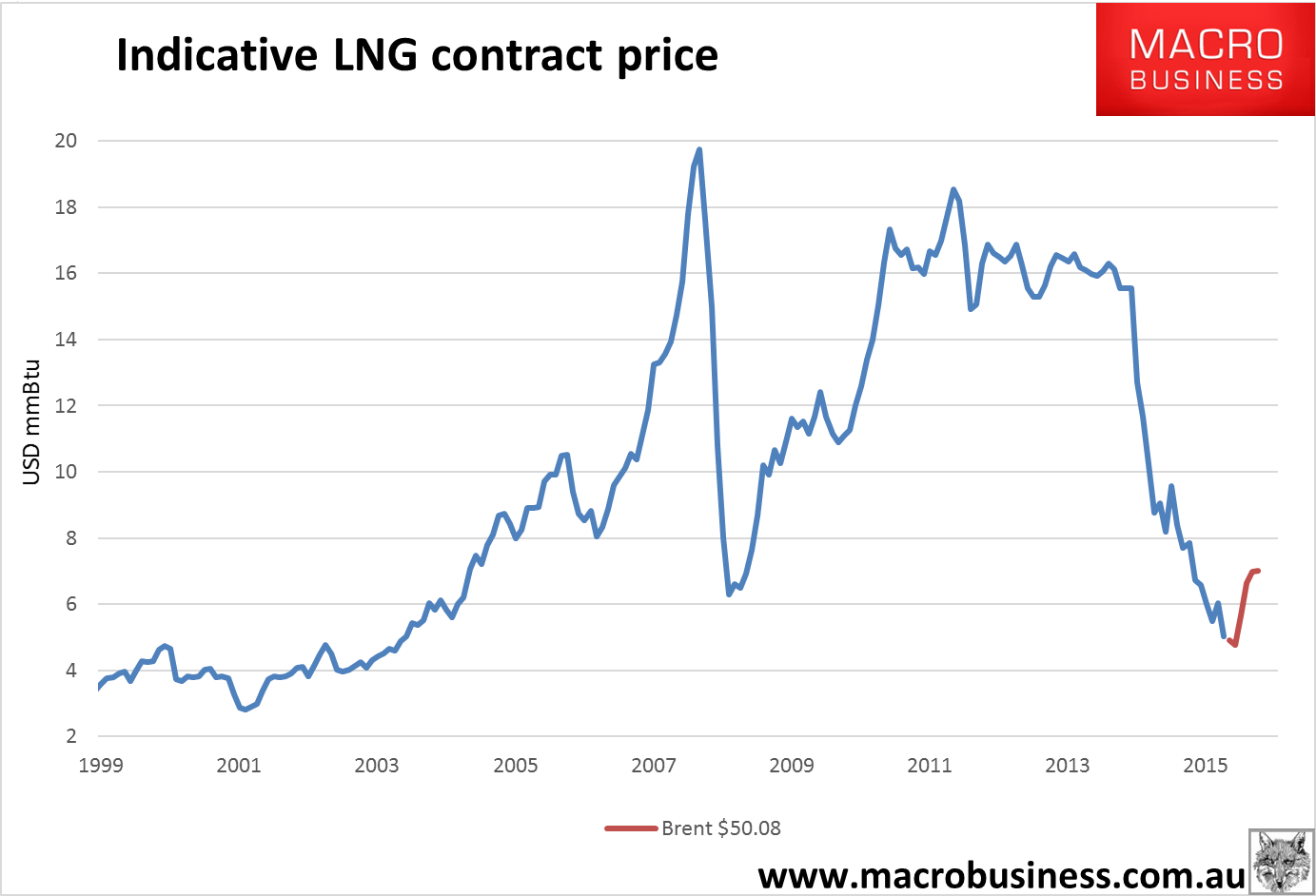

Turning to LNG, the oil-linked contract price was hit hard back $7.01mmBtu:

In news, FLNG is struggling, from Bloomie:

It’s longer than three soccer fields, heavier than two aircraft carriers and powerful enough to chill gas into liquid colder than the surface of Jupiter.

And its maiden voyage couldn’t have come at a worse time.

The world’s first modern vessel for producing liquefied natural gas was ordered by Petroliam Nasional Bhd in 2012 when LNG traded for more than $15 per million British thermal units. It was launched last month, with prices down by about two-thirds. Royal Dutch Shell Plc faces a similar problem with its version of a floating LNG plant, which will be larger than any ship ever built.

“At $15 and above you can do anything, so everyone went and did everything,” said Trevor Sikorski, a natural gas analyst for Energy Aspects Ltd. in London. “Now all these projects start to come online at the same time, and all of a sudden you have all this supply and now your margins are next to nothing.”

The plight of the PFLNG Satu, as the first vessel is known, reflects the larger struggle facing all producers. Projects approved years ago when energy prices were high are coming online now, adding to a global supply glut that has pushed spot LNG down to $4.62 per million Btu this week

Petronas, Malaysia’s state-owned energy company, is betting the cycles will even out over the long run. PFLNG Satu will produce about 1.2 million tonnes of LNG annually for the next 20 years from the Kanowit gas field, which is located about 180 kilometers (112 miles) north of the coast of Borneo.

“We are taking a long-term view for this project,” Petronas said in a written statement. “In terms of profitability, the project is still viable as an additional supply point within our larger portfolio of LNG assets.”

Puts a new spin on the phrase “sunk cost”.