While Mortgage Choice CEO, John Flavell, hilariously tried to claim on Monday that Australian housing was “under-leveraged”, LF Economics has released a new report entitled Australia’s Addiction to Debt: Imbibing the Beverage but Ignoring the Leverage, which analyses Australia’s debt and finds that our household debt load is now tied with Switzerland for the highest in the world but with a worsening trend.

Below are some key extracts from this report.

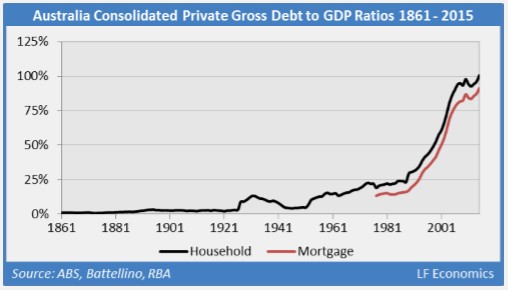

The long-run trend in household debt demonstrates a near exponential rise beginning in the late 1980s, amplified by the privatisation and deregulation of the banking and financial sector. This has provided lenders greater autonomy in issuing debt, most of which has found its way into the household sector…

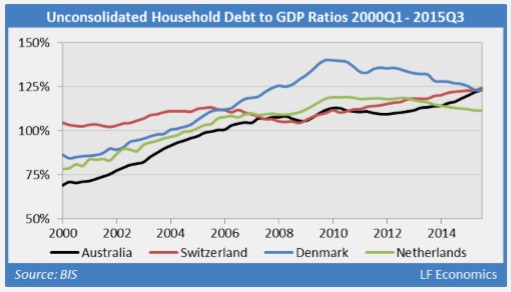

Internationally, Denmark had long held the unholy accomplishment of having the highest unconsolidated household debt to GDP ratio but has slowly deleveraged since its housing bubble peaked and burst during the GFC. Its ratio peaked at a record 140%. Slight falls in nominal GDP has slowed the descent of Denmark’s ratio, while Switzerland, suffering from the same malaise, has risen steadily on the back of moderate increases in household debt.

Australia now vies with Switzerland for the world’s most indebted household sector. The Netherlands is in fourth place, the only other nation having a ratio above 100%. Annualised mortgage debt growth of around 7% in Australia and nominal GDP and household income growth of around 2% implies a credit gap of 5%. Indications are the unconsolidated household debt to GDP ratio will continue to rise in the near future.

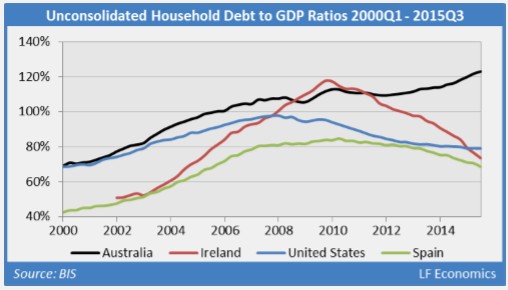

Australia’s ratio has grown above peaks established in countries where housing bubbles formed and burst, as in Ireland, Spain and the United States. The ratios can rise even as the household sector deleverages in absolute terms due to negative nominal GDP growth (the denominator). This typically occurs during a debt deflation, along with the rate of inflation turning negative. The phenomenon is known as Fisher’s paradox, where debt burdens actually increase in real terms during an economic downturn.

The ratio has risen by approximately 150 basis points each quarter over the last year, mirroring the rise in the growth of housing prices. This runaway growth heralds financial instability as the stock of debt becomes ever larger. Absent further cash rate cuts, there is little room on household balance sheets to leverage further…

The report, which contains 32 graphics and detailed commentary, can be downloaded here.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.