Gradually, Australian commentators are coming to the realisation that the Turnbull Government’s announced $48.2 billion policy to cut the company tax rate from 30% to 25% over a decade could actually leave Australians worse-off.

Today, Fairfax’s Mark Kenny has noted that further cuts to spending or tax increases would likely be required to offset the cost of the company tax cut, according to advice from Independent Economics relied upon by the government to justify the policy:

The tax cut will deprive Canberra of more than $8 billion a year in revenue while recovering only a fraction of that through the extra growth in jobs and wages predicted.

While the government expects more than half of the shortfall to be recovered from greater economic activity, the modelling reveals that nearly all of it is to be recovered from companies voluntarily deciding to do the right thing through a dramatic improvement in the level of corporate tax compliance, which has been described by some economists as “ambitious”…

“The major source of ‘self funding’ for the corporate tax cuts isn’t increased wages or employment, it is the assumption that companies will voluntarily engage in far less profit shifting … it’s bizarre,” said Richard Denniss, the chief economist of left-aligned think tank, the Australia Institute…

Meanwhile, Fairfax’s Ross Gittins penned a piece over the weekend backing his colleagues Peter Martin and Michael Pascoe who both believe that the benefits of any company tax cut would flow primarily to foreigners:

…the more economists think about the plan and examine the Treasury modelling supporting it, the less enthusiastic they become…

The first reservation comes from a factor peculiar to Australia: our system of “dividend imputation”…

To match their dividends, shareholders receive a “franking credit” set at the same rate as the company tax rate…

Trick is, only Australian shareholders in our companies receive franking credits; foreign shareholders don’t. In consequence, Australian shareholders (who include everyone with superannuation savings) have little to gain from the cut in company tax. It gives them no reason to change their behaviour.

Imputation has turned our company tax into little more than a tax on foreign shareholders. Which means almost all the benefit from the company tax cut goes to foreigners.

…the cut would leave the government short of revenue and thus needing to fill the gap somehow. Its least unrealistic scenario is that it would be filled by increasing income tax – say, by allowing years of bracket creep…

If you wanted to create jobs, cutting the tax on foreign investors isn’t the way to do it.

Labor’s Bill Shorten has also stepped-up his attack against the Coalition’s company tax cut, arguing over the weekend that it would represent a ‘gift’ to Australia’s biggest banks and foreigners:

[Shorten] said most of the benefit would be “absorbed by the big banks in extra profits, or it will go overseas”…

He said the $50 billion cost of the corporate tax cut would deliver “very little economic gain” while also leaving less money for education, healthcare and the “needs of middle-class and working class families.

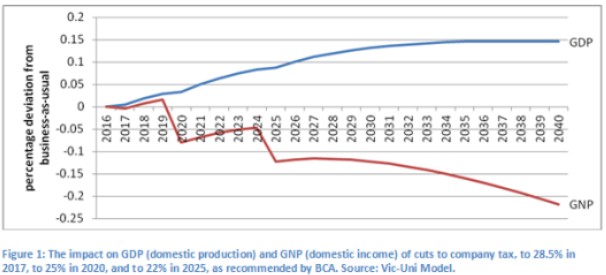

Again, these critiques follow modelling from Victoria University senior research fellow, Janine Dixon, which showed that cutting company taxes would actually reduce national income – the best measure of living standards:

This is because cutting company taxes would primarily benefit foreign owners/shareholders at the expense of Australian taxpayers, hence lowering national income.

Given that the company tax cut would primarily benefit foreign owners/shareholders, and come at the expense of spending on health, education, infrastructure and the like, each of which likely offers far more social and/or productivity benefits, where is the merit in cutting Australia’s company tax rate?