Another weekend, another batch of negative gearing lies from Prime Minister Malcolm Turnbull. From The Australian:

The Prime Minister said he had used negative gearing in the past, as do more than one million Australians today.

“What Labor is proposing will … reduce investment at a time we need more investment – they’re jacking up the tax on investment by increasing capital gains tax by 50 per cent – and what they’re proposing on negative gearing will reduce the number of rentable properties, it will jack up rents, and it will smash home values,” Mr Turnbull said.

“If you believe you can take up to a third of the buyers out of the residential property market, and not send prices south, and they’re pretty soft now, then you really are in cloud-cuckoo-land.”

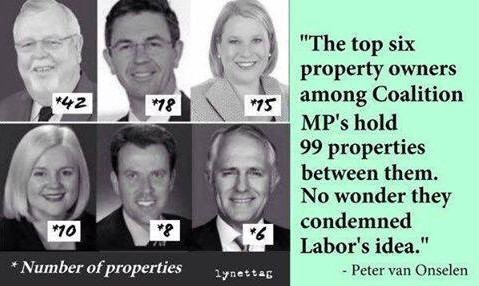

Turnbull is not kidding when he says that he used negative gearing to get ahead. He does own six homes after all, and together with the other top 5 Coalition MPs, they own an incredible 99 properties between them:

Moreover, as revealed over the weekend by the Parliamentary Library, Coalition electorates represent 80 of the top 100 negative gearing postcodes.

So it is fair to say that Turnbull and his Coalition cronies have a vested interest to retain negative gearing and the capital gains tax (CGT) discount, and in the process keeping housing values inflated.

Turnbull’s claim that Labor’s policy would “reduce investment” is also curious in light of his 2005 Tax Policy Paper, whereby he described negative gearing and the CGT discount as a “sheltering tax haven” that is “skewing national investment away from wealth-creating pursuits, towards housing”, and has caused a “property bubble”.

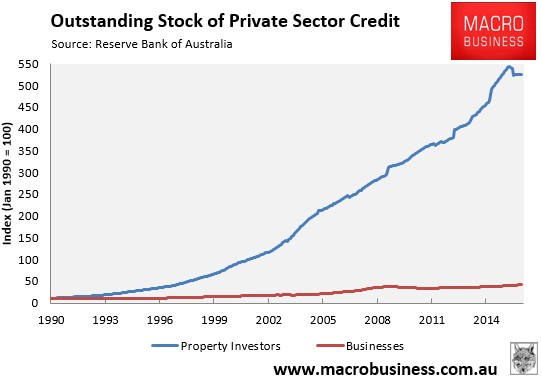

Therefore, it is highly contradictory for Turnbull to argue that Labor’s reforms to negative gearing would suddenly choke genuine productive investment, when this is already happening under the current rules. If you want proof, check-out the below chart:

As shown above, outstanding business loans have grown at a snail’s pace compared against outstanding property investment loans, which have skyrocketed. So if there is one segment of the economy that is losing-out from the current tax structure it is productive business lending, particularly lending to small enterprises, which is being crowded-out by housing lending.

Turnbull is also conveniently silent on why current tax rules allow individuals to claim unlimited negative gearing deductions for property investments into perpetuity, but if they invest in a productive side business, they must meet all kinds of criteria in order to claim losses against their wage/salary earnings, including showing a profit in three out of five years.

Moreover, in his 2005 tax paper Turnbull admitted that “Australia’s rules on negative gearing are very generous compared to many other countries” and that “the normal deductibility principles do not apply to negatively geared real estate such that the taxpayer is not obliged to demonstrate that the negatively geared property will generate positive cash flow at some point in the distant future”.

Turnbull’s claim that Labor’s negative gearing policy “will reduce the number of rentable properties” and “will jack up rents” is nonsensical.

Sure, there would be less “investment” (read transfer of ownership) in existing dwellings, but those homes would not magically disappear from the supply-demand equation. Rather, those homes would be purchased by an owner-occupier, thus reducing demand for rental properties by the same proportion as the fall in rental supply. Turnbull has completely ignored the fact that the pool of tenants will similarly decline as they become owner-occupiers.

More importantly, because Labor’s policy would channel negative gearing towards new builds, overall dwelling construction would increase, as will the supply of rental accommodation. And this extra supply would obviously lower rents, other things equal. It’s economics 101.

If Turnbull truly believes his spin, then why does his Government champion foreign investment in newly constructed homes, but preclude it from established dwellings?

Again, here’s the chair of the foreign investment inquiry, Liberal MP Kelly O’Dwyer, explaining the benefits of this ‘new homes only’ policy:

“Currently the framework seeks to channel foreign investment in residential real estate into new dwellings in order to increase the housing stock for Australians to build, buy or rent. Foreign investment is encouraged in new dwellings whether they be apartments, units or homes because in addition to creating more supply, it also creates more jobs for the building and construction sector – all of which helps to grow our economy”.

So, Turnbull’s opposition to Labor’s policy directly contradicts its own stance on foreign investment.

About the only part of Turnbull’s argument that makes any sense is the claim that property values would decline, but even on this point he’s being overly dramatic in an attempt to scare the electorate.

The fact that Labor’s policy grandfathers existing negatively geared investors means that there would be no “rush for the exists” and forced sales. Instead it would dampen investor demand going forward, thereby giving would-be first home buyers greater opportunity to become owner-occupiers.

With dwelling values nationally basically at all-time highs against incomes and rents, how is this “bad” policy?

Why is it desirable to see home prices rising further into the stratosphere, distorting the economy and eroding intergeneration equity even further?

And what about the Budget savings that would come with Labor’s policy, estimated at $32.1 billion over the decade by the independent Parliamentary Budget Office. Surely this is welcome news in the era of the “Budget emergency”?

No matter which way you cut it, Turnbull’s arguments against Labor’s policy makes little sense and contradicts his Government’s own policy on foreign investment as well as his previous written views on negative gearing and the CGT discount.