Fairfax’s Jessica Irvine has written an interesting article on the blow-out in Federal Government debt, which is projected to grow to $640 billion by 2026-27:

The blow out in government debt is the sleeper issue of this election. Both parties have decided to abandon the so-called “debt and deficits disaster”. But on it ticks.

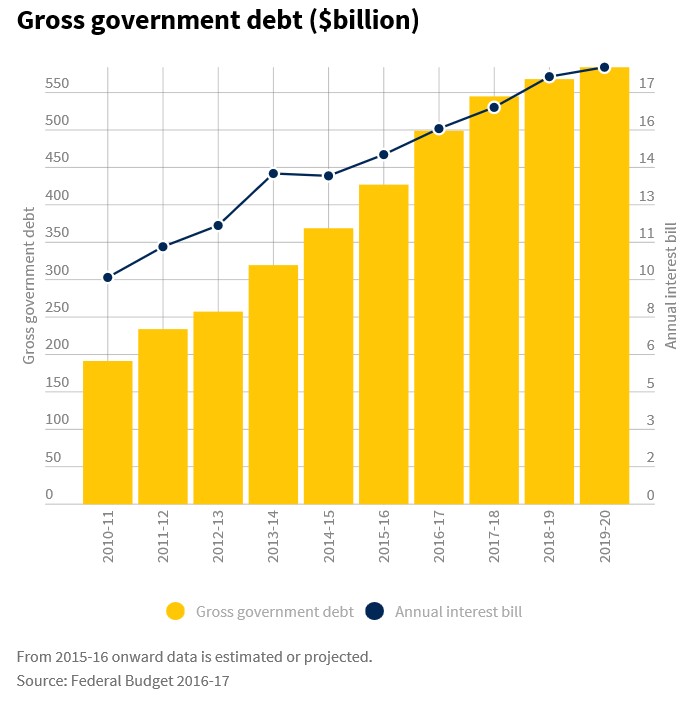

Whichever party takes power will, within its first year, be forced to issue a new direction to allow government debt to exceed the current $500 billion limit.

Today the government has $435 billion worth of securities – mostly bonds – on issue.

By 2026-27, this will hit $640 billion…

It isn’t a disaster. Our net debt position remains low compared to other countries. Six countries with AAA ratings have a higher net debt to GDP ratio than us, including New Zealand, Canada and USA. But our debt is growing more rapidly than most.

And there are hidden costs…

Borrowing to invest in things which increase the economy’s productive capacity, like infrastructure and education, makes sound financial sense…

But the federal government today is in debt simply to fund “recurrent” expenses, like pensions and welfare.

Readers might recall that in late-2011, the Reserve Bank of Australia (RBA) announced the creation of the Committed Liquidity Facility (CLF), in order to meet the Basel III liquidity reforms. Below is the RBA’s explanation of the CLF [my emphasis]:

The facility, which is required because of the limited amount of government debt in Australia, is designed to ensure that participating authorised deposit-taking institutions (ADIs) have enough access to liquidity to respond to an acute stress scenario, as specified under the liquidity standard…

The CLF will enable participating ADIs to access a pre-specified amount of liquidity by entering into repurchase agreements of eligible securities outside the Reserve Bank’s normal market operations. To secure the Reserve Bank’s commitment, ADIs will be required to pay ongoing fees. The Reserve Bank’s commitment is contingent on the ADI having positive net worth in the opinion of the Bank, having consulted with APRA.

The facility will be at the discretion of the Reserve Bank. To be eligible for the facility, an ADI must first have received approval from APRA to meet part of its liquidity requirements through this facility. The facility can only be used to meet that part of the liquidity requirement agreed with APRA. APRA may also ask ADIs to confirm as much as 12 months in advance the extent to which they will be relying on a commitment from the Bank to meet their LCR requirement.

The Fee

In return for providing commitments under the CLF, the Bank will charge a fee of 15 basis points per annum, based on the size of the commitment. The fee will apply to both drawn and undrawn commitments and must be paid monthly in advance. The fee may be varied by the Bank at its sole discretion, provided it gives three months notice of any change…

Interest Rate

For the CLF, the Bank will purchase securities under repo at an interest rate set 25 basis points above the Board’s target for the cash rate, in line with the current arrangements for the overnight repo facility.

Advertisement

In light of the federal budget deficit ballooning-out to $435 billion, and the deficit likely to keep on growing, the question for the RBA is: shouldn’t the CLF be unwound and the banks instead required to hold government bonds, as initially required under Basel III? Bonds on issue have more than doubled since the CLF was first announced, so surely the RBA/APRA should amend the liquidity rules so that Australia’s ADIs are forced to purchase government bonds, so that the size of the CLF requirement decreases?

The cost of the CLF is very low ie 15bps pa, compared to the alternative. The CLF allows ADIs to originate mortgage assets and create RMBS rather than buying government bonds. The net spread on mortgage assets or RMBS compared to government bonds is much greater than 15bps pa probably now in the order of 150bps if you could pull together a direct comparison including costs… This simple comparison demonstrates that the cost to the banks of 15bps is a direct subsidy to all ADIs.

…my advice to the RBA and APRA on the CLF is simple.

Advertisement

Significantly increase the cost from 15bps pa to better reflect the cost of the alternative of owning government bonds, and

Due the increase in government bond issuance and the likely sustainability of that issuance, ADIs should be required to hold a significant portion (maybe 50%) of those bonds as part of Basel III liquidity provisions in order to decrease the size of the CLF whilst the bonds are on issue.

Don’t expect any action, though, as RBA/APRA fluff their dumb bubble at our expense.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.