Easy money that’s led to housing bubble pales compared to current environment

Leverage has increased since the crisis

Wildly dovish Fed is causing “recklessness at the government and corporate level”

“The Fed has no end game”

Fed objective seems to be making sure the market doesn’t fall 20% in next six months

Fed raising odds of tail risk event they are trying to avoid

This feels like just before the financial crisis

Fed policy allows government to avoid problems like tax reform

Corporate sector is stuck in mismanagement, questionable capital allocation and growing indebtedness yet investors pay 18 times earnings

Basically, Drukenmiller is saying that an end of cycle stocks crash is coming so the Fed is going to reverse course and embark on QE4. Citi says that is already being priced:

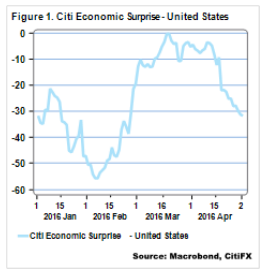

US economic data have been soggy, other than labor market data, which means that we get one positive data release a month followed by a series of disappointments. This is reflected in the Citi’s economic surprise index (Figure 1), which has been dropping since mid‐April and where a 0 level would be considered strong outperformance.

My conjecture is that investors have begun to price out June/July hiking risk they are beginning to reject the view that there is a high‐probability fed funds path that is as shallow as the market is pricing in.If you really think that a full hike is not likely until May 2017 (as is now priced in), you have to think there is a non‐negligible probability that the economy is so bad that you would want to cut.

Fed officials turn purple whenever anyone suggests that they might be facing negative rates and indications are that it would be supremely unpopular with the public.

Before you get to negative rates you would have the hail Mary of QE4 which would act mainly to push down long term yields. In the past the prospect of QE supported equity markets, but there is so much skepticism at this point that the equity market reaction is negligible and the brunt of the concerns are falling on USD and long‐term yields.

I don’t think we’re there yet but do agree that when the next end-of-cycle shock arrives that the Fed will print again. Negative interest rates appear to have already failed as a policy tool (though Japan may test that further yet) and if helicopter money is used instead of simple QE then it’s still currency debasement so the US dollar should still fall and gold rise, even if equities do not benefit quite so much.

Advertisement

Remember that, in the end, gold is about just one thing: the US dollar.

For Aussie investors, MB has been bullish on gold for roughly a year now, though we offer the one caveat that it is probable that gold will fall sharply during the next end-of-cycle stock market shock as money flows into the US dollar safe haven, at least until the Fed pulls the QE trigger. I’ve circled the last time that that happened in 2008:

Advertisement

For Australian domiciled investors that could be a good entry point, but, now is probably just as good a time because during any further period of US dollar strength, any weakness in gold is unlikely to outpace that in the Australian dollar as interest rates keep falling.

As a former gold trader, I always looked to play the cycle via equities which give you nice leverage to the price so long as they mine in Australia in local currency costs and do not hedge.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.