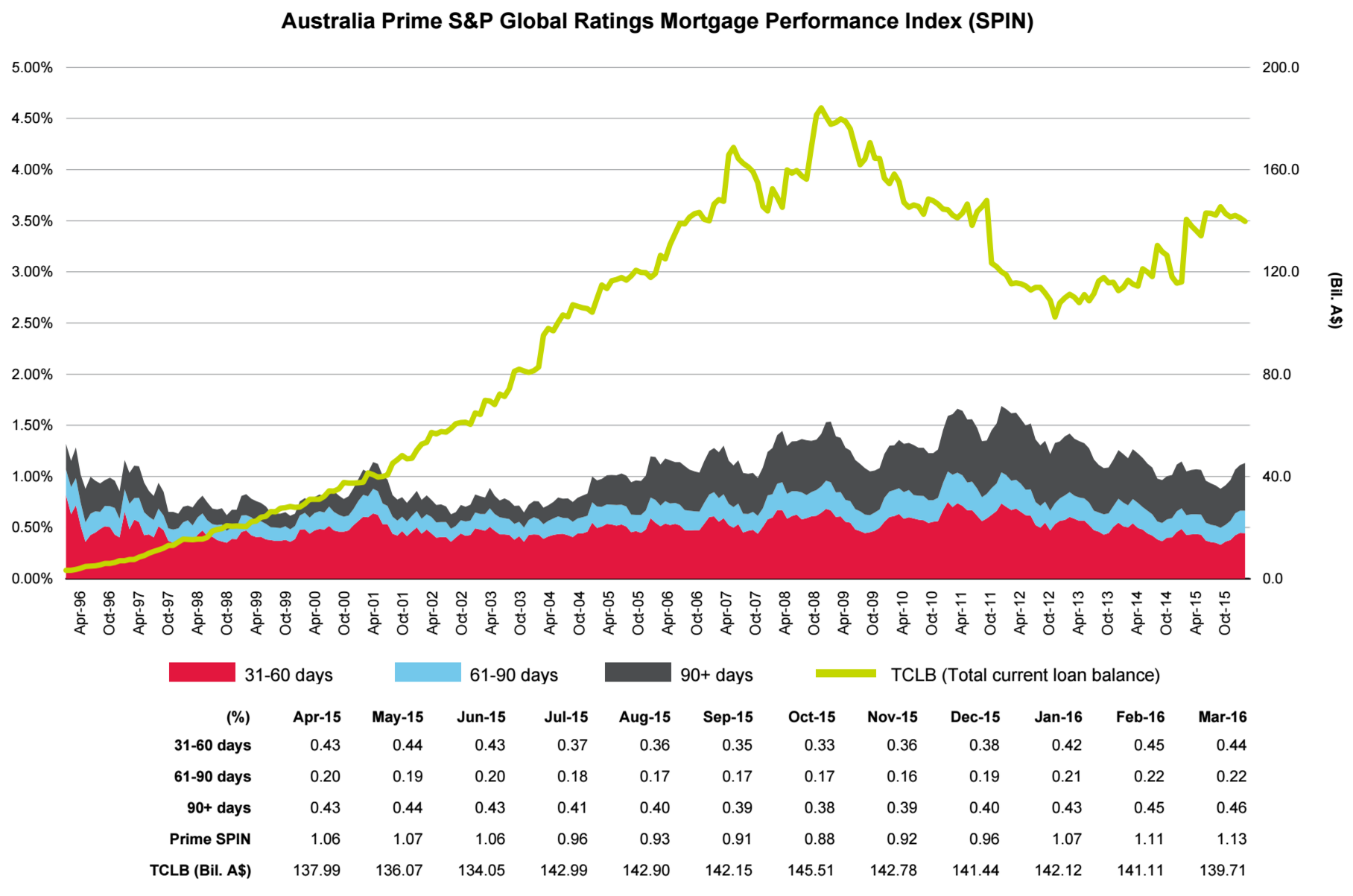

The number of Australian housing loans in arrears extended their rise into a fifth consecutive month in March for prime residential mortgage-backed securities (RMBS), as measured by Standard & Poor’s Performance Index (SPIN). The upward trend in arrears was not consistent across all product types, however, according to S&P Global Ratings’ recently published “RMBS Arrears Statistics: Australia.”

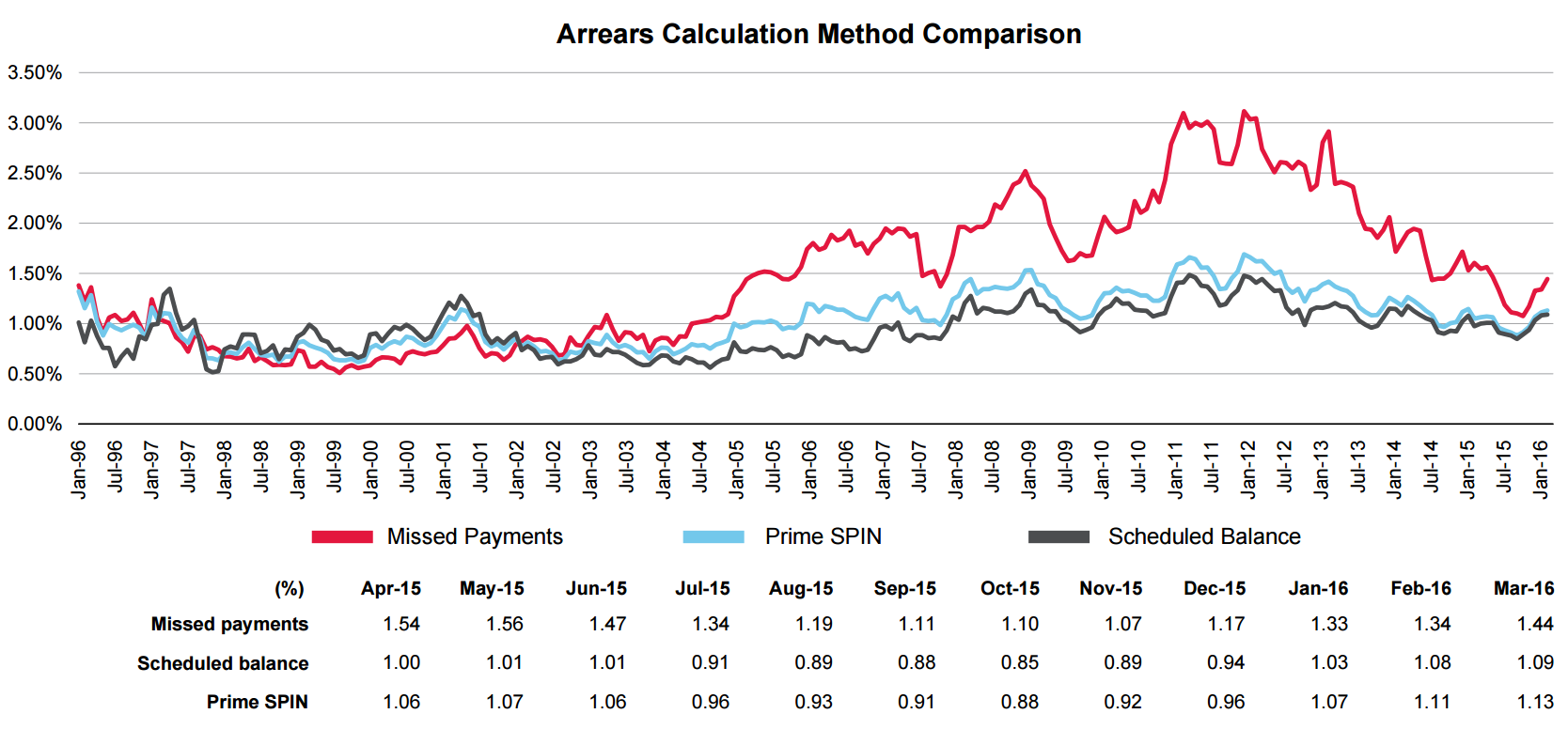

The prime RMBS SPIN increased to 1.13% in March from 1.11% in February. While a decline in outstanding loan balances during the month would have affected this movement, the dollar value of loans in arrears increased, resulting in prime arrears being up overall. The SPIN for full-documentation loans rose to 1.09% from 1.07% a month earlier, with some of the increase due to a decline in outstanding loan balances.

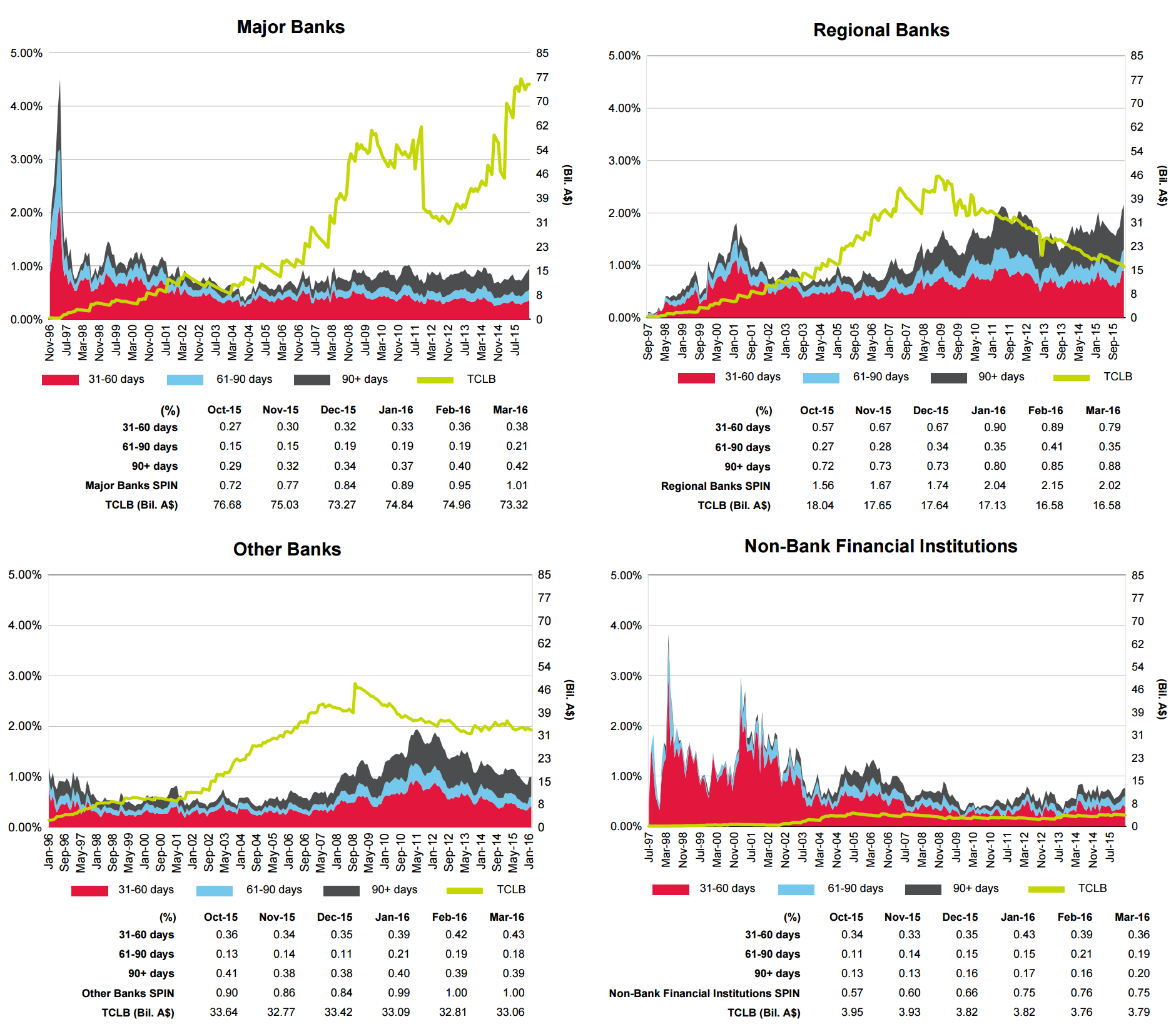

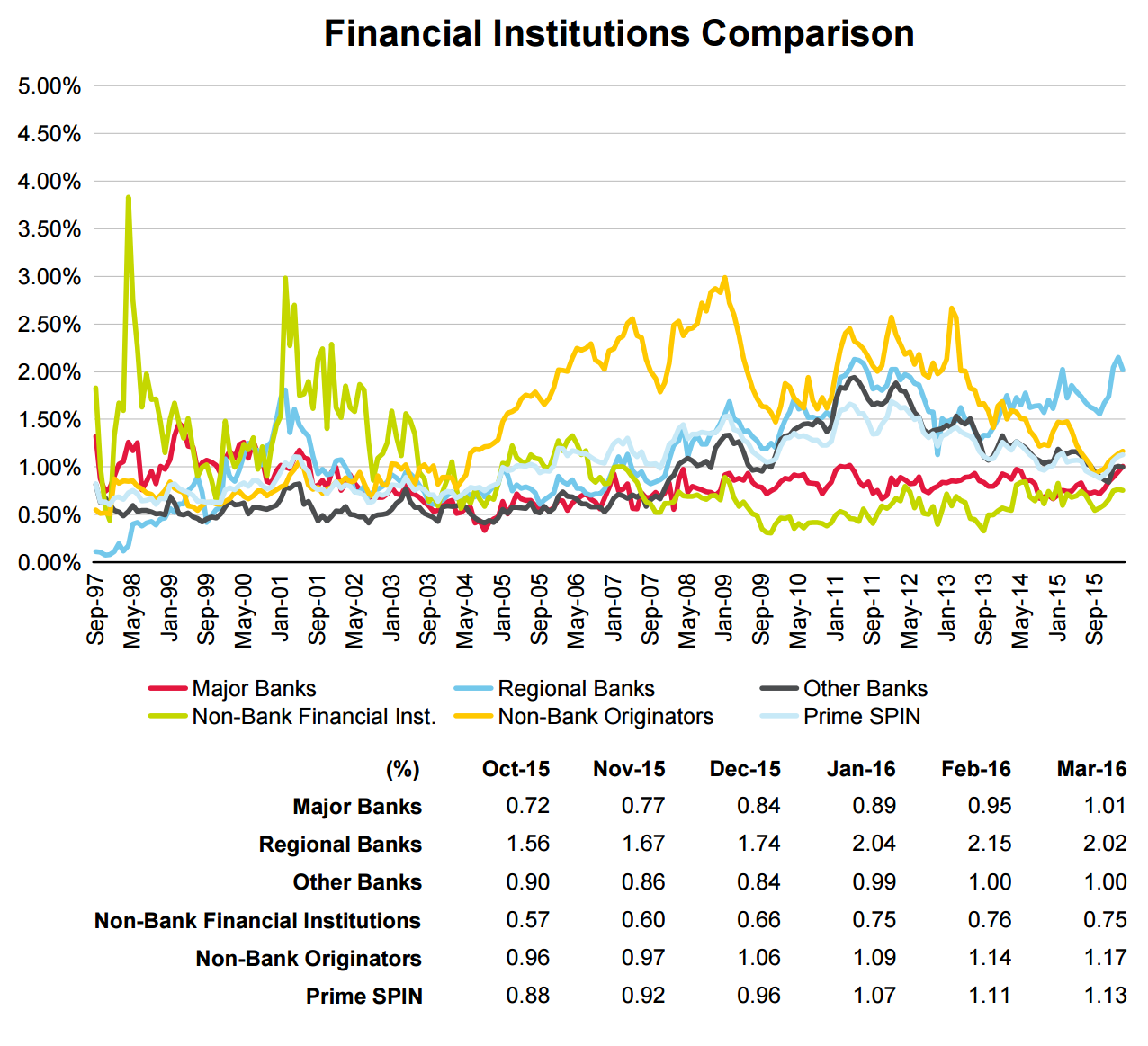

Regional banks experienced the largest decline in arrears in both dollar and percentage terms, with arrears falling to 2.02% in March from 2.15% a month earlier. At 2.02%, their arrears are still the highest of all originator types.

The major banks recorded the largest increase in arrears in March, with their SPIN rising to 1.01% from 0.95% in February. The level for the major banks is still relatively low, however, and remains below the SPIN.

The most recent rate cut–to the extent that lenders pass it on to borrowers–is yet to have an effect on arrears. Lower rates are positive for arrears, given a majority of loans are variable-rate mortgages, but the extent to which they can offset the effects of lower wage growth is still being worked out. Arrears remain below their decade-long average of 1.25%, and even if they do continue to rise from these low levels, we do not expect this to translate into higher defaults in the current economic climate of relatively stable employment conditions.

Nothing too alarming there but noteworthy that major bank arrears rates have climbed to the very top of their previous decade trading range. The first quarter is the worst in seasonal terms but even so a new cycle of bad loans is underway with clear potential to break onto higher ground. Full report.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.