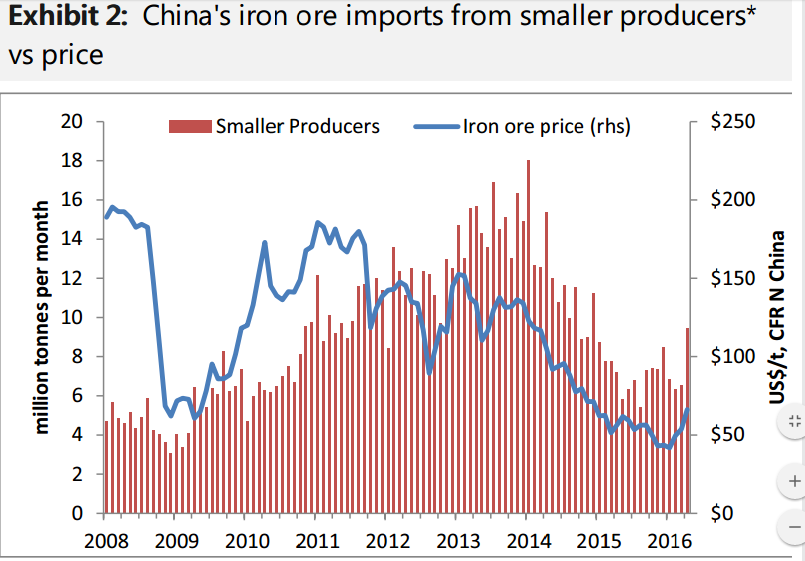

Smaller producers re-enter market: The lift in iron ore prices ytd has spurred there-entry of smaller producers into the seaborne market.Exports from Peru, Chile, New Zealand, Mauritania, Canada, Venezuela and Kazakhstan areall up so far this year. In addition, India is coming back into the seaborne market,annualizing 11Mt of exports to China vs. just 2Mt in 2015. Although individually minuscule compared to exports from Australia and Brazil, collectively thesetonnes are meaningful (annualizing 113Mt in Apr-16; +31% yoy).

China’s import dependency higher; but domestic output recovering: China’s imports of iron ore in Jan-Apr climbed 5.9% yoy (to 325Mt). Domestic ore production fell at the beginning of the year to a low of 80Mt/month on weaker steel production and low prices, which delayed the seasonal lift in output this year. However, local miners are again ramping up in response to robust steel production rates and buoyant prices–output lifted to 103Mt in April (-0.6% yoy).Feedback from our recent visit to China suggests that most remaining domestic mines are profitableata seaborne price >US$50/t.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.