From an incredulous Credit Suisse who was the one investment bank to see fundamentals at work in the iron ore spike:

■ The physical steel market in China went from buoyant to frozen in a week. We were looking for steel prices to ease, but not capitulate. Tangshan billet prices surged up 53% from RMB 1720/t on 1 Mar to RMB 2640/t on 21 Apr and back to RMB 1970/t by 9 May. We may not have seen the floor yet. This rapid change is not fundamentals, its sentiment.

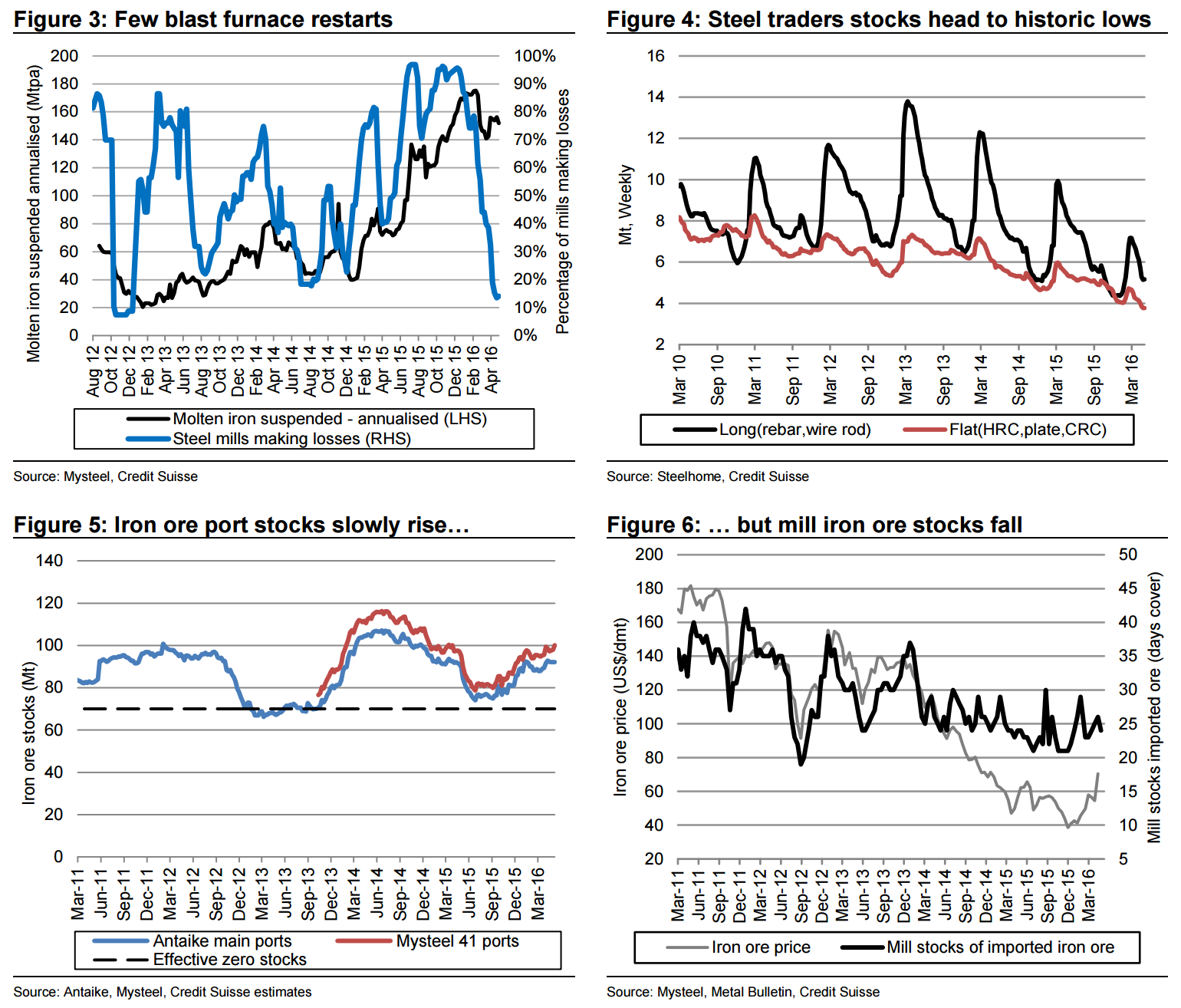

■ What’s next? Not much has changed in the physical market – China’s construction season continues, infrastructure projects are still in the starting phases, and steel traders’ inventories are still at historic lows. We await fresh statistics releases, but doubt that April steel production swamped demand. The rapid price fall looks to be a steel buyers strike as sentiment turned sour. But a buyers strike is a destock event, and a restock must follow. Steel prices should lift again, although perhaps not to the previous lofty heights.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.