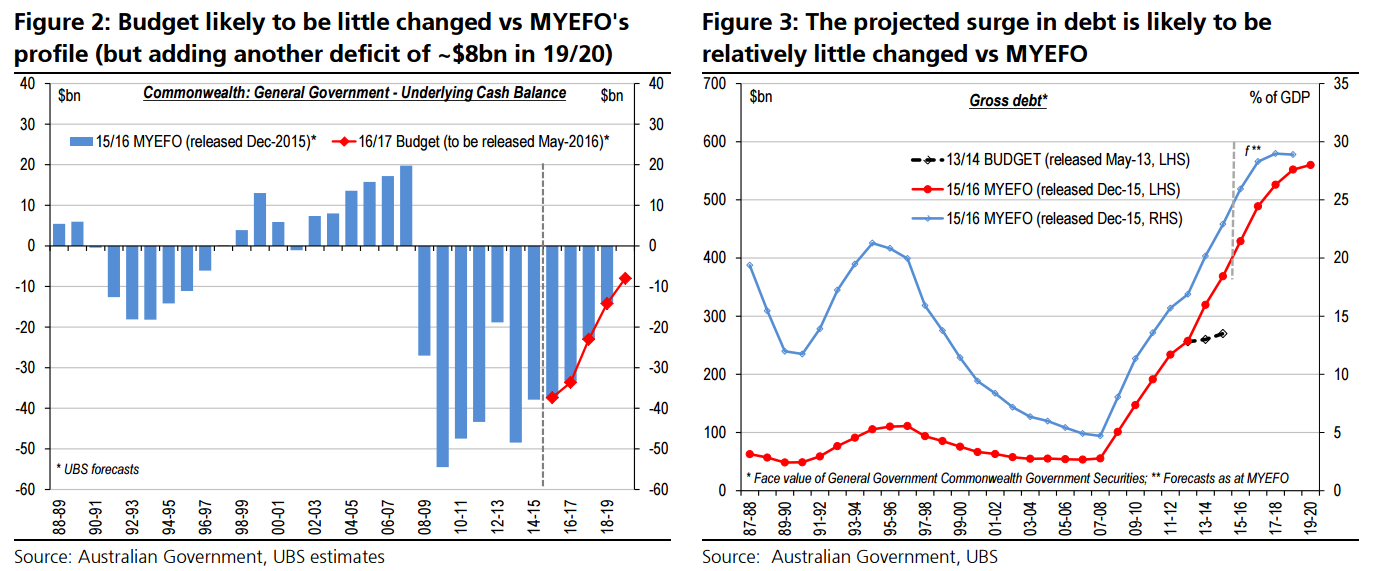

16/17 CW Budget Preview – the end of slippage? Treasurer Morrison will bring down the 16/17 Commonwealth Budget on May 3 (a week earlier than normal) – his 1st & the Coalition Governments’ 3rd. Overall, the deficits for the Commonwealth General Government sector appear to be tracking broadly in line with the MYEFO released in Dec-15 (Figures 1 & 2), which projected ongoing narrowing from $37bn (2.3% of GDP) in 15/16, to $34bn (1.9% of GDP) in 16/17, $23bn (1.3% of GDP) in 17/18, and $14bn (0.7% of GDP) in 18/19. The Budget also extends the deficits to 19/20, which we see at ~$8bn (0.4% of GDP). Notably, this could be the first Budget/MYEFO for a number of years that has minimal fiscal slippage – albeit after the projected peak in gross debt had already surged by a massive ~$300bn, or ~12%pts of nominal GDP, in the prior few years. The MYEFO projected the face value of Commonwealth Government Securities for the General Government sector would surge to a peak of $552bn or 29% of GDP in 18/19 (but with another ~$8bn deficit in 19/20 set to increase the peak of debt further to ~$560bn). This compares with the May-13 Budget which projected a peak in debt of ~$270bn or 17% of GDP in 14/15 (Figure 3).

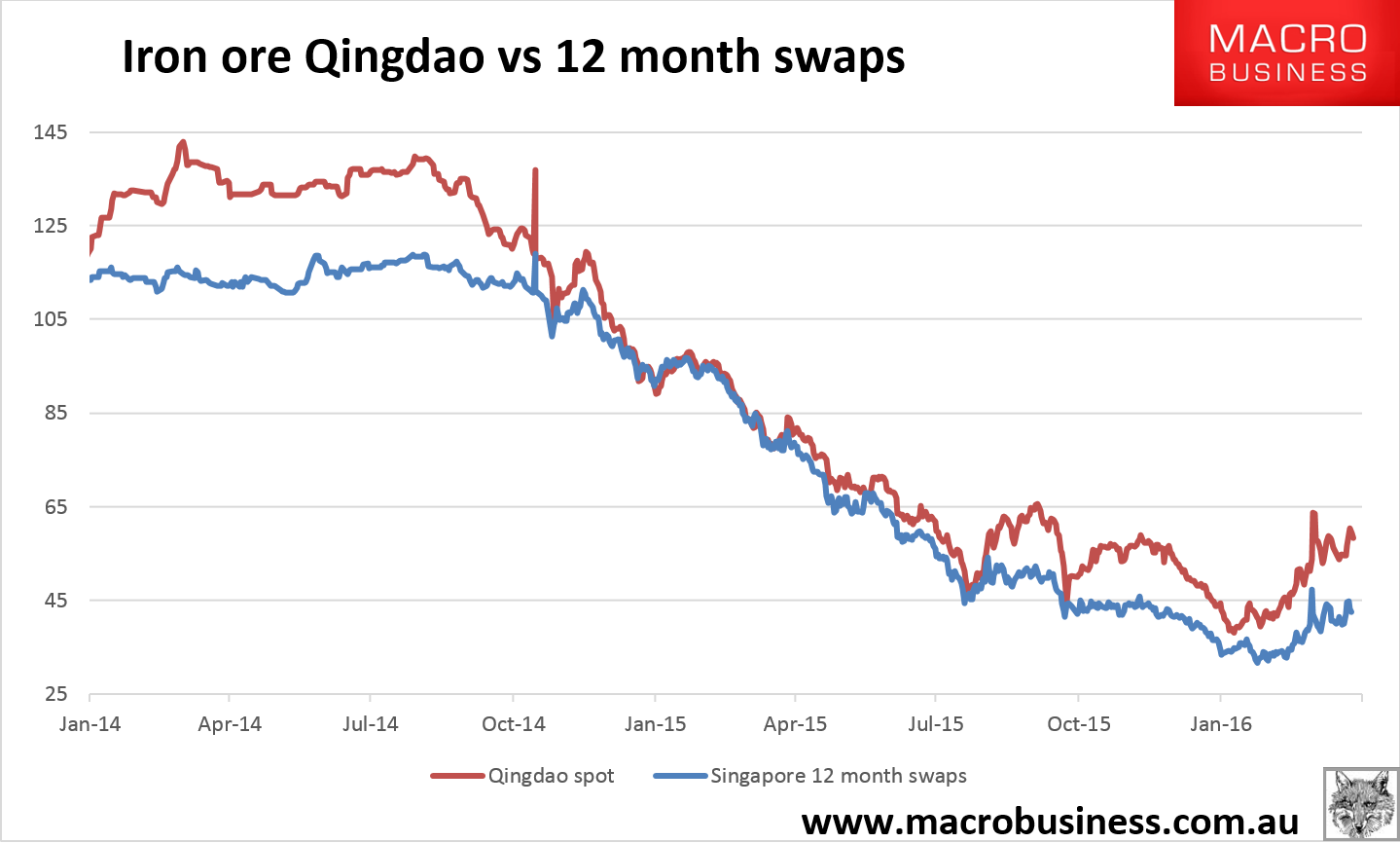

A likely key support to this Budget is a surprising bounce in the iron ore price to an average of ~USD$50-55USD FOB in recent weeks, which is well above the Government’s MYEFO assumption of USD$39 FOB (Figure 4). Sensitivity analysis presented in last year’s Budget showed that each USD$10 rise in the iron ore price should raise tax revenue by $2.1bn in the current year and $4.4bn in the following year. Hence, we estimate this recent price move – if projected to be sustained – could improve the budget up to ~$8bn p.a., or a cumulative ~$27bn over 4 years. However, we expect this boost to be broadly offset. Firstly, the Government will probably decide to stall at least some of the unlegislated ‘savings’ from policy measures announced in prior Budgets – which the independent PBO estimates have a cumulative fiscal impact of $13.3bn over the 5 years to 19/20 (and a cumulative impact of $36.5bn over the decade to 25/26). Secondly, despite a recent bounce in commodity prices and real GDP, we still expect Budget forecasts for nominal GDP growth to be trimmed by a further ~¼%pt p.a. across the forecast horizon (Figure 5). Based on Treasury sensitivity analysis – where each 1%pt cut to nominal GDP deteriorates the budget by $2.7bn in the current year, and $5.7bn in the following year – we estimate the total hit to the budget is a cumulative ~$11bn over 4 years.

The Singapore 12 month swap (which the government should be using as its forward price) is today at $42.48:

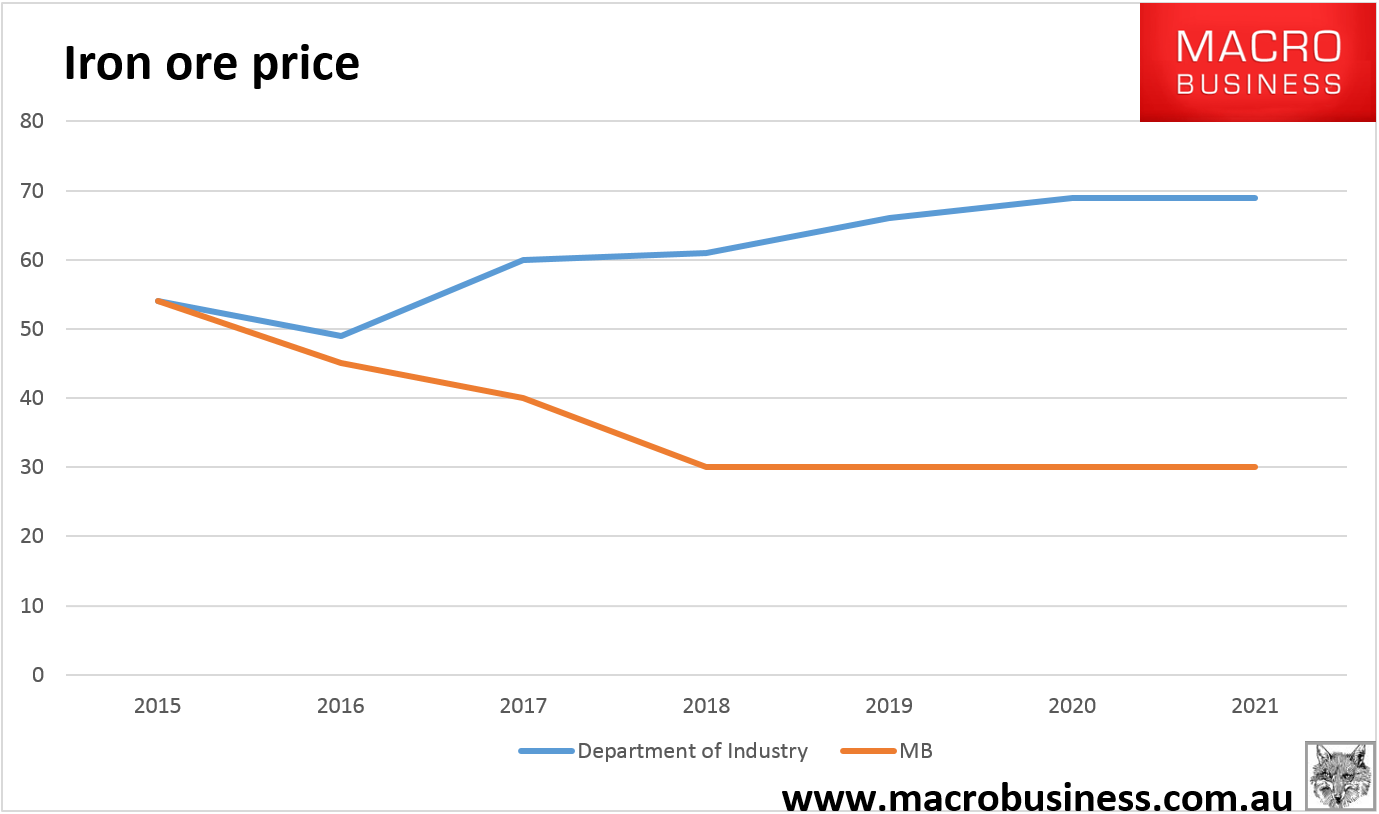

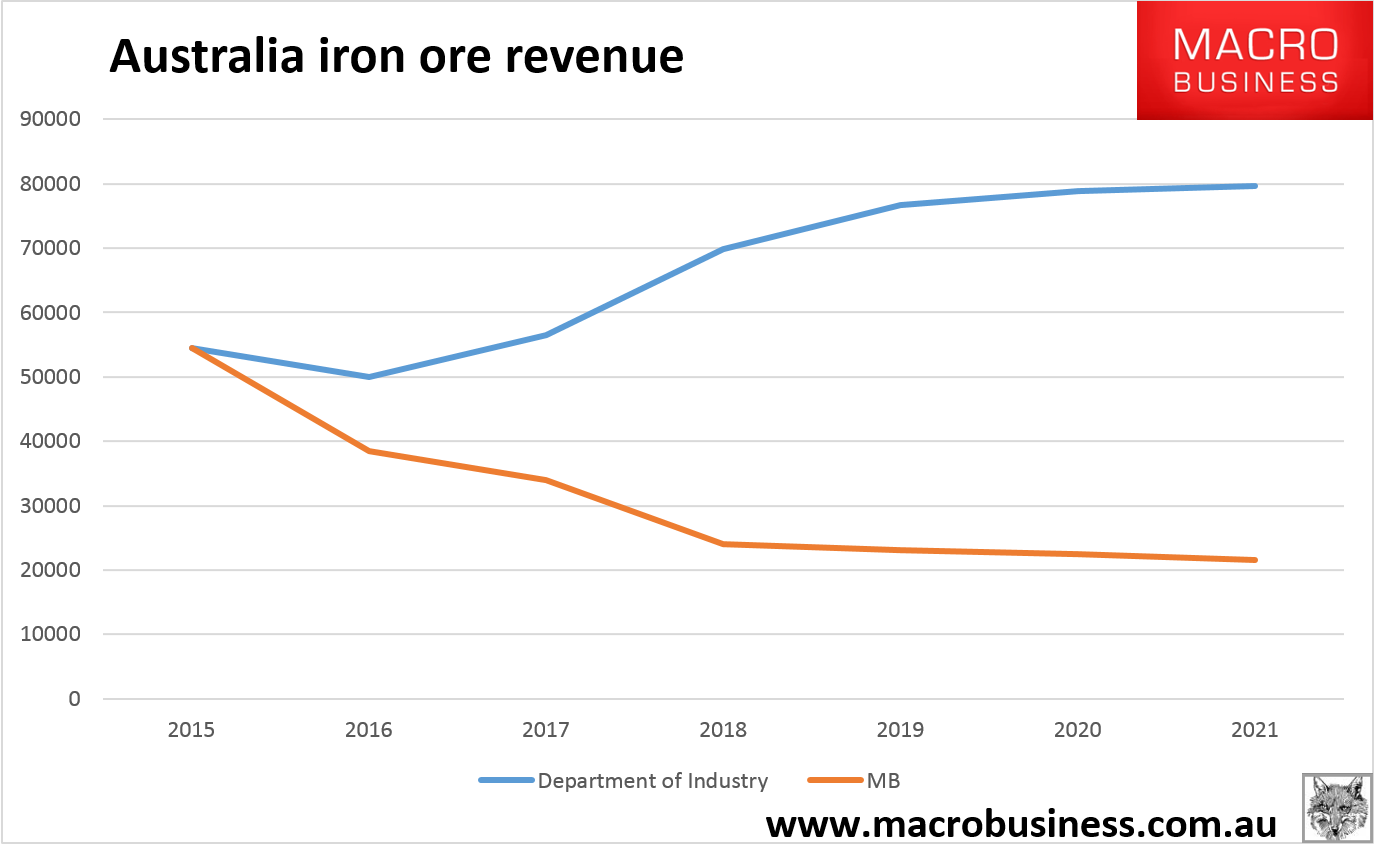

Subtract freight charges of $5 and ScoMo should be downgrading his Budget forecast from $39 to $37.50FOB. Alternatively, ScoMo could go with the Department of Industry forecasting propaganda:

Advertisement

All ScoMo need do is change nothing in Treasury’s currently spastic iron ore forecasting method so I give the truth very long odds.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.