In this week’sSQM Research Newsletter, Luca Simms wrote an interesting analysis of Melbourne housing supply, whereby they argued that the city is facing a tightening rental market as evidenced by falling rental vacancy rates:

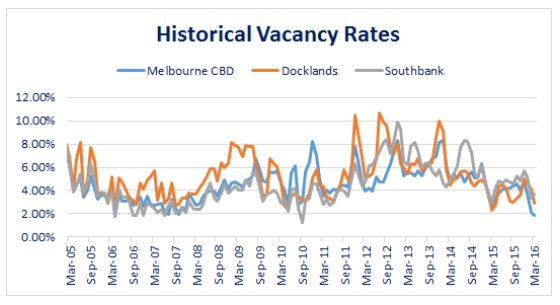

Vacancy rates are considered to be one of the best indicators of a market oversupply, however, amongst all the chat and hype of a potential oversupply has anyone really looked at the vacancy rate figures for these localities? As stated in last week’s newsletter, SQM Research data shows that vacancy rates for Melbourne have actually been in a downtrend since 2014 and are now below 2%. Those main areas of concern, CBD, Docklands and Southbank, show that the numbers have actually been falling to levels below their long term average.

I’m not saying that Melbourne’s apartment market won’t be subjected to an oversupply in coming years, I’m not saying it will either, however, if I were asked to comment on whether or not Melbourne is currently over supplied, I would have to say no as the vacancy figures continue to show that the absorption rate of new product placed on the market continues to be steady.

Fair enough analysis. However, it is important to note that SQM’s calculations of vacancies are based on online rental listings that have been advertised for three weeks or more compared to the total number of established rental properties. Calculations of vacancies are based on online rental listings that have been advertised for three weeks or more compared to the total number of established rental properties.

Advertisement

Therefore, SQM does not count the potentially very large number of homes withheld from the rental market.

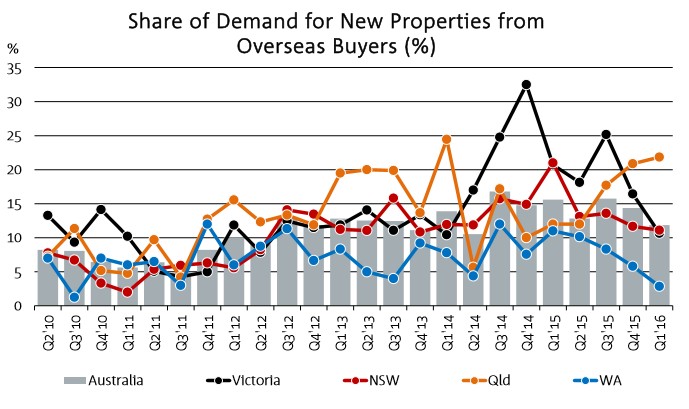

We also know that foreign investors have been a major source of demand for new dwellings in Melbourne (see below chart), most of which are located in the areas in and around the Melbourne CBD, and that buyers from China, in particular, prefer to keep their homes empty rather than renting them out.

Advertisement

Thus, while advertised vacancies might be tight, actual vacancies are likely not.

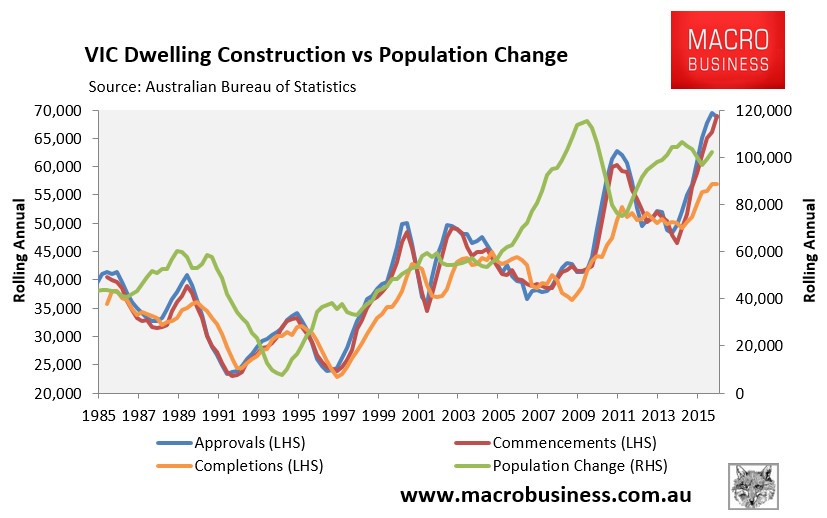

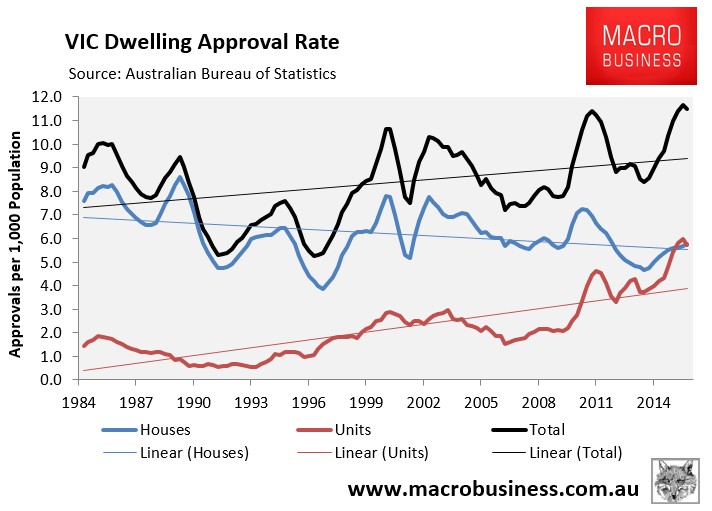

Given the huge construction levels across Melbourne over the past four years (see below charts), with much more in the pipeline, one wonders how long this rental tightness can last.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.