The Reserve Bank of Australia (RBA) has released its private sector credit aggregates data for the month of March:

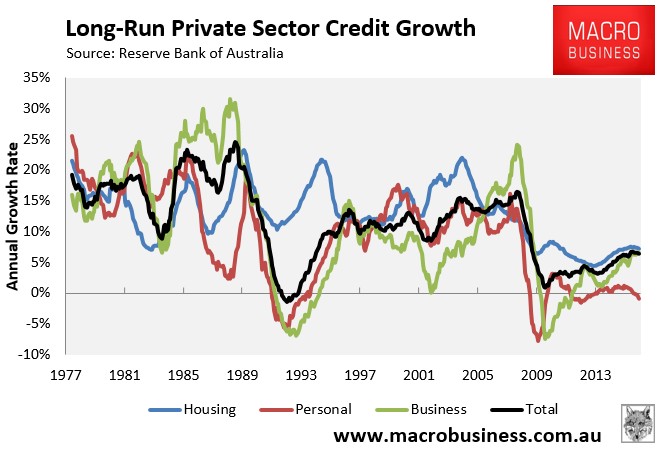

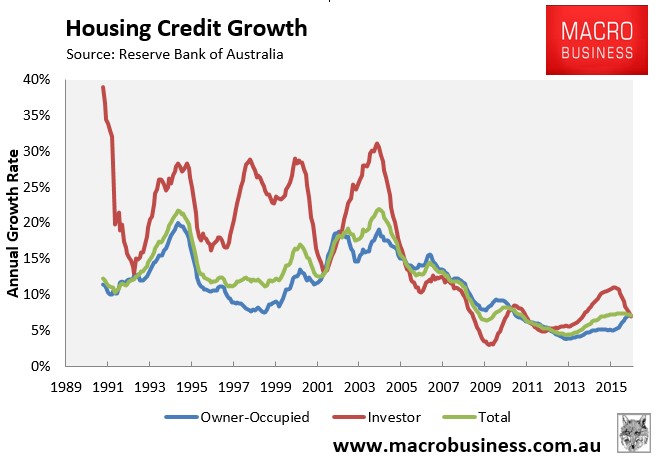

A chart showing the long-run breakdown in the components is provided below:

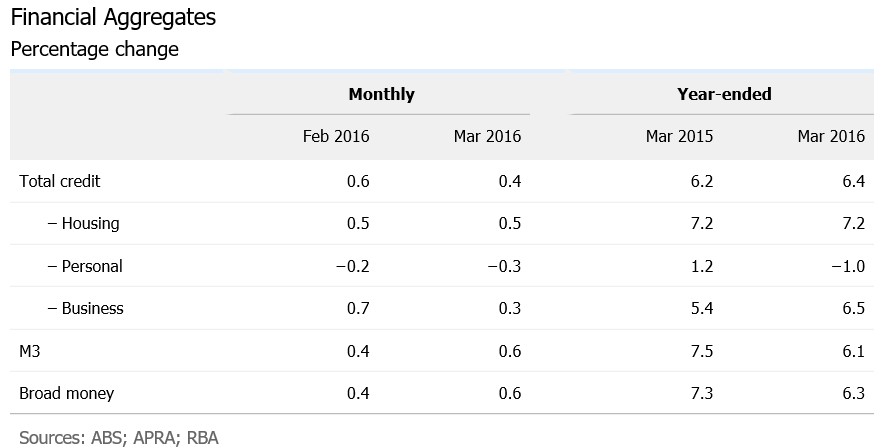

Personal credit growth (-0.2% MoM; -0.7% QoQ; -1.0% YoY) is still in the gutter, whereas business credit growth (0.3% MoM; 1.7% QoQ; 6.5% YoY) remains solid. Housing credit growth (0.5% MoM; 1.5% QoQ; 7.2% YoY) is stronger again, but remains below its long-run average growth rate (although in dollar terms it is near the highest level on record – see below).

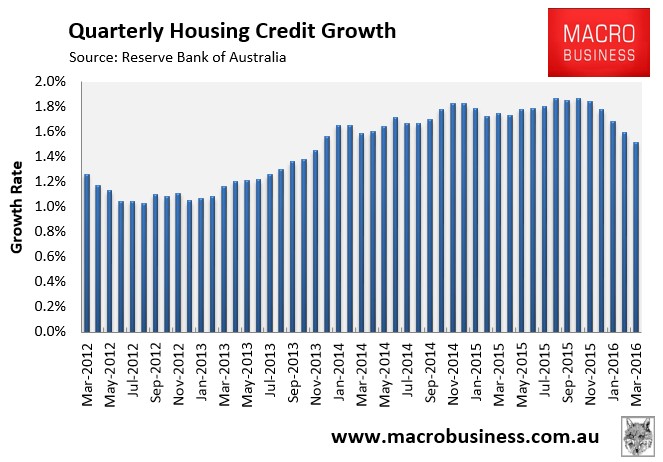

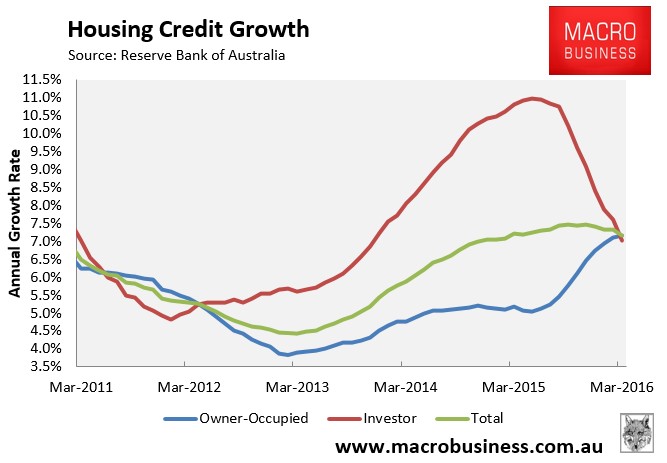

The below chart shows that quarterly housing credit growth continues to fall rather sharply:

A long-run breakdown of owner-occupied credit (0.53% MoM; 1.66% QoQ; 7.17% YoY) and investor credit (0.34% MoM; 1.25% QoQ; 7.04% YoY) is provided below:

For more than three years, the lion’s share of mortgage growth came from investors, leaving owner-occupied demand in its wake. However, investor credit growth is now slowing fast, whereas owner-occupied credit growth is rising, which suggests that APRA’s and the banks’ macro-prudential tightening against investors have worked:

An alternative explanation is that there has been a re-classification of loans from investor to owner-occupied.

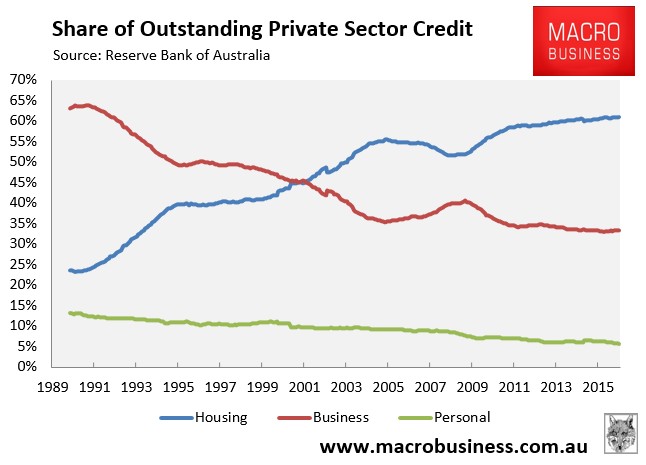

The share of loans going to housing was 60.96% as at March 2016, which is an all-time high. By contrast, the share of total loans to businesses was at 33.34% as at February, which is fractionally above June’s record low:

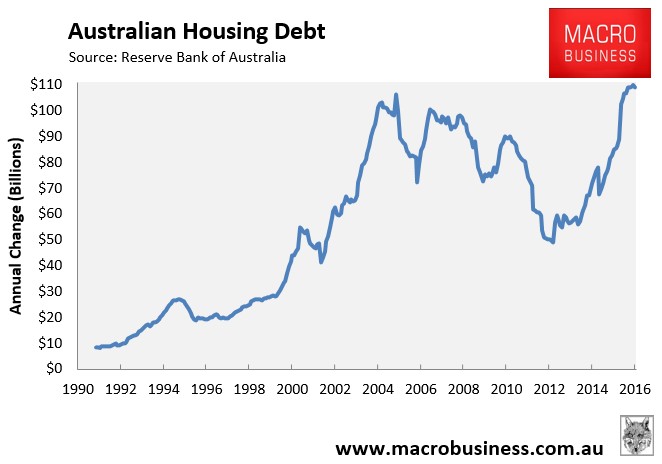

Finally, in nominal dollar terms, the annual change in outstanding Australian mortgage debt retraced marginally in March from February’s record high. That said, mortgage credit still grew by a whopping $108.8 billion in the year to March 2016: