Yesterday’s report released by the Australian Population Research Institute, entitled Sydney and Melbourne’s Housing Affordability Crisis: No End in Sight, contained a stark warning for investors in off-the-plan apartments, which are facing a massive oversupply of 123,000 in Melbourne and 59,000 in Sydney by 2022:

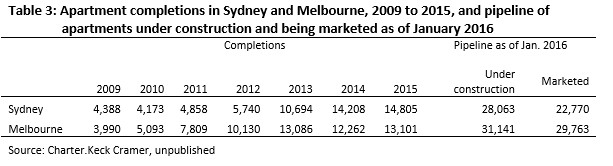

When we reviewed the Melbourne apartment scene in early 2013 it seemed that this initial boom would soon abate. Some of the smartest property people whom we interviewed thought that a glut of small apartments was imminent and that it would soon undermine investors’ confidence in the apartment market.It was not to be. There has been an extraordinary second surge of apartment approvals which is reflected in the approvals data for ‘other dwellings’ shown in Table 2 above. This time it has affected Sydney as well as Melbourne. Again, it will take several years for the full impact on the apartment market to show up in completions. Table 3 indicates that this impact is already occurring in Sydney. By 2014 and 2015 there were more apartment completions in Sydney than in Melbourne.

An apartment surge is about to hit the market

In 2016 and 2017 the consequences of the recent surge in apartment approvals will become apparent. Some approved projects take considerable time before marketing and construction begins. Others never go ahead. The best indication of what is about to hit market is the number of apartments in projects where marketing off-the-plan has begun and of course those projects where construction has actually begun. The data compiled by Charter.Keck Cramer and shown in Table 3 is limited to these two categories of approvals. As noted, these are for all projects of 10 apartments or more. However, as elaborated on in the discussion around Table 4 below, most of these projects are for high-rise apartments.

As Table 3 shows, the pipeline of apartments under construction and being marketed as of January 2016 in both cities was huge. It was just over 60,000 in Melbourne and near 51,000 in Sydney. Charter.Keck Cramer estimate that around 21,790 of this pipeline in Melbourne will be completed in both 2016 and 2017 and around 22,455 in both 2016 and 2017 in Sydney. This represents a huge lead of around 70 per cent in the annual number of new apartment completions in both cities in 2014 and 2015.

As is argued in Part Seven of this report below, a glut of high-rise apartments is inevitable. Yet developers are still searching for new apartments sites and, as Table 2 indicates, approvals for ‘other dwelling’ approvals continued to grow through 2014-2015…

According to Knight Frank, the minimum price of apartment construction is now around $9,000 per square metre in Sydney29 and $6,500 in Melbourne. As a result, even a tiny 50 square metre apartment built in Sydney will have to be priced at around $450,000 if the developer is to make a profit. In consequence any prospect of a surge in the production of family friendly apartments has receded further. Only those households capable of competing in luxury markets will have any interest in purchasing such a dwelling, or have the necessary funds to do so…

While we don’t want to put a date on it, the fact is that thousands of off-the-plan investors will soon be confronted with a market replete with surplus apartments. This will first become obvious in Melbourne. When it does, it will create a wave of uncertainty that will ripple across the residential property industry. As we have argued, the investor housing bubble has been driven by the expectation of endless increases in the capital value of dwellings. A downturn in the high-rise apartment market will undermine this assumption and in so doing is likely to take some of the heat out of the detached housing market.

How can we be sure? Our projections leave little doubt about the forthcoming surfeit in apartments, especially in Melbourne. As detailed in Appendix One, where the output of other dwellings (mainly apartments) is compared with dwelling needs, the comparison shows a massive surplus of other dwellings in 2022 of 123,000 in Melbourne and 59,000 in Sydney. Moreover, the output side of these projections is conservative. It was based on the average number of approvals for ‘other dwellings’ over the years 2010-11 to 2014-15. However, approvals for such dwellings (mainly in the form of high-rise apartments) have surged in Sydney and Melbourne since 2013, (see Table 2).

We will not have to wait until 2022 before a glut of apartments becomes obvious. It is already looming over Sydney and Melbourne. As noted in Table 3, completions are about to jump to around 21,000 to 22,000 in both 2016 and 2017 in Sydney and Melbourne, from 13,000 to 14,000 in both cities in 2014 and 2015.

For those wary about projections, let us summarise the argument. The current huge production of apartments is occurring at a time when the need is limited. This is because there will be little growth in the number of young adult Australian residents over the next decade. They are the main source of demand for apartment rentals while singles and couples. Their stay in apartments is temporary because the vast majority move to family friendly housing when starting a family. When they leave they vacate space for the next cohort. Most of the projected expansion in the need for apartments will come from of overseas migrants, especially those on temporary visas. However, as noted, the stock of these migrants is not expanding nearly as fast as was the case in the past decade.

This is not all that apartment investors will have to contend with. In Sydney, apartments are becoming more expensive because of the escalation in site costs described above. In Melbourne, price is not such an issue. But the transformation of the cheaper apartment precincts into dense enclaves of mobile tenants, large numbers of whom will be Asian temporaries, most certainly is. So too is the physical oppressiveness of these precincts as new developments create wall to wall blocks sheer to the footpath. In addition these precincts are largely devoid of community facilities and open space. This makes it all the more likely that Maureen McInroy’s prediction that they will be regarded as slums will come to pass. Who will want to buy such apartments?…

It is investors rather than developers who are taking on most of the risk, since it is the investors who will have to test the market to see whether there are enough owner occupiers or other buyers around on whom to offload their investment at a profit. This does not happen until several years after the initial off-the-plan purchase. As long as investors believe that real estate prices can only go up, they are likely to keep buying and developers will have an incentive to market new projects…

The off-the-plan investors are among the most financially vulnerable of recent dwelling investors. They are likely to find that the value of their apartment at settlement is worth considerably less than at the time of their purchase. The banks will only provide finance equivalent to their assessment of the value of the property. Faced with paper losses, some buyers may forego their deposit. Some Chinese investors may also face difficulty transferring the required Australian dollars to meet their obligation. In both cases this will add to the stock of apartments on the market, putting further downward pressure on their price.

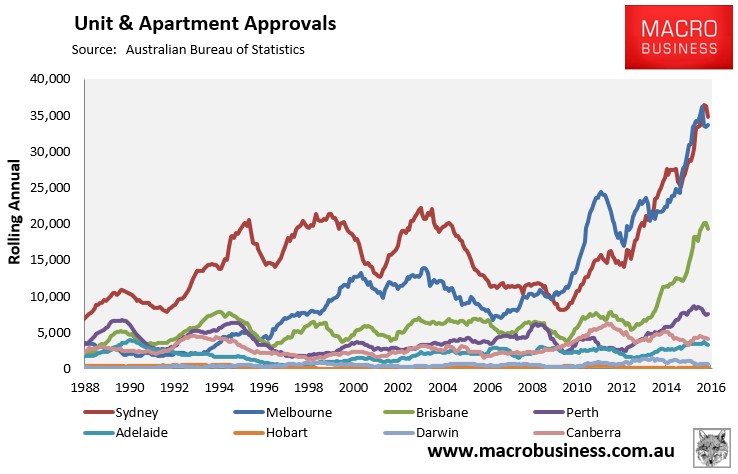

In reality, Brisbane should also be added to the list given it too has experienced a monumental surge in apartment construction (see next chart).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.