Watching Prime Minister Malcolm Turnbull tie himself in knots over negative gearing is like watching a slow motion train wreck.

At the start of the week, Turnbull attacked Labor’s negative gearing and CGT policy because they would not raise enough Budget revenue – despite the independent Parliamentary Budget Office (PBO) estimating that the policies could save the Budget some $32 billion over 10 years once they come into force, albeit back-ended:

“As far as Labor’s announcement is concerned, I will make a couple of observations: one is that it raises relatively little money in the near term, over the next four years, and they acknowledge that. So it doesn’t address the big deficit…”

Turnbull also argued that Labor’s policy would “distort” the housing market:

“The policy as described has been criticised and I think fairly, as likely to really distort the housing investment market, so it is not a well-designed policy (and) it doesn’t provide any budgetary relief, at least any time soon.”

Yesterday, Turnbull took this “distortion” argument to another level, claiming that Labor’s policy would ruin the market for new homes:

“The value of a new property is obviously a function of what you can sell it for. You can negative gear a new apartment, for example, but you can’t negative gear that apartment when it is sold,” he said.”That obviously reduces the number of people considerably who would be potential buyers of it. The impact on the value of new properties, and therefore the viability of developments, will be affected.

“This is yet again an example of Labor rushing out with an announcement that they thought sounded good, they thought they could get a headline for but they haven’t thought it through.”

Mr Turnbull’s remarks about causing a distortion are curious on a number of levels.

First, the current negative gearing and CGT discount are already causing a big market distortion by channeling excessive investment into housing, most of it pre-existing dwellings. Even the timid RBA acknowledged these distortions in its June 2015 submission to the Home Ownership Inquiry:

The Bank believes that there is a case for reviewing negative gearing… the interaction of negative gearing with other parts of the taxation system may have the effect of encouraging leveraged investment in property. In particular, the switch in 1999 from calculating CGT at the full marginal rate on the real gain to calculating it as half the taxpayer’s marginal rate on the nominal gain resulted in capital gain-producing assets being more attractive than income-‐producing assets for some combinations of tax rates, gross returns and inflation.

This effect is amplified if the asset can be purchased with leverage, because the interest deductions are calculated at the full marginal rate while the subsequent capital gains are taxed at half the marginal rate. Since property can usually be purchased using higher leverage than other assets that produce capital gains, property is especially affected by this feature of the tax system.

Turnbull’s new found concern about the impact of Labor’s policy on “the value of new properties, and therefore the viability of developments” is also curious given the Coalition’s recent review into foreign investment championed rules restricting overseas buyers to new dwellings only because it boosts supply and creates construction jobs. Here’s chair Kelly O’Dwyer’s justification of this regime:

Currently the framework seeks to channel foreign investment in residential real estate into new dwellings in order to increase the housing stock for Australians to build, buy or rent. Foreign investment is encouraged in new dwellings whether they be apartments, units or homes because in addition to creating more supply, it also creates more jobs for the building and construction sector – all of which helps to grow our economy.

Non resident foreign investors, while they can purchase new dwellings cannot generally purchase existing dwellings. Applications to purchase new dwellings are therefore generally granted, while applications to purchase existing homes are only granted if the purchaser is a temporary resident.

Here’s a question for Mr Turnbull: why is foreign investment in new dwellings encouraged by the Government because it boosts dwelling construction and jobs, and helps grow the economy, but Labor’s property tax policy – which would achieve exactly the same result – dissuaded? Surely, precluding foreigners from purchasing established dwellings also “reduces the number of people considerably who would be potential buyers of it”, thereby reducing “the viability of developments”?

Clearly, Mr Turnbull’s opposition to Labor’s plan is full of contradictions and has been made on the run for political purposes rather than sound policy judgements.

Finally, we know that Mr Turnbull believes that current tax settings favour richer older people over younger working Australians. He said so in 2014:

“Looking at Australia’s tax regime you would say that it is too tough on people earning income… but is incredibly concessional to older people who have made their money…

All of these areas are very hard to deal with because any change invariably… [leads them]… to become very angry. That’s why reform is very difficult…”

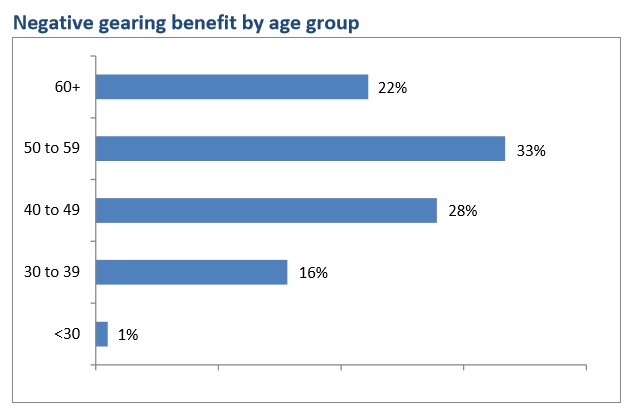

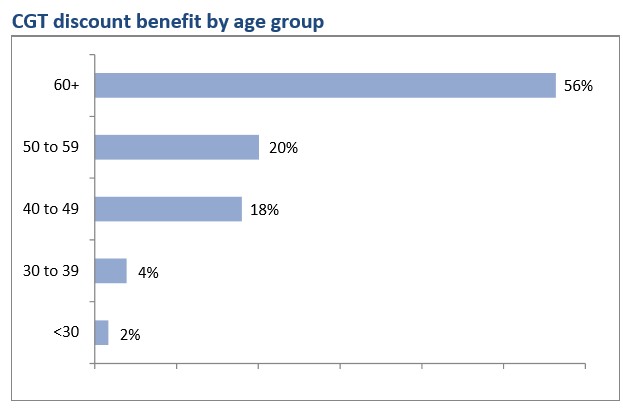

Well, here we have two policies – negative gearing and the CGT discount – which overwhelmingly favour older Australians over the young:

Here is Mr Turnbull’s chance to announce his own reforms to negative gearing and the CGT discount to both improve the Budget and inter-generational equity and fairness.

Does he have the ticker to act, or is he going to follow Tony Abbott’s path of opposing reform for short-term political gain?