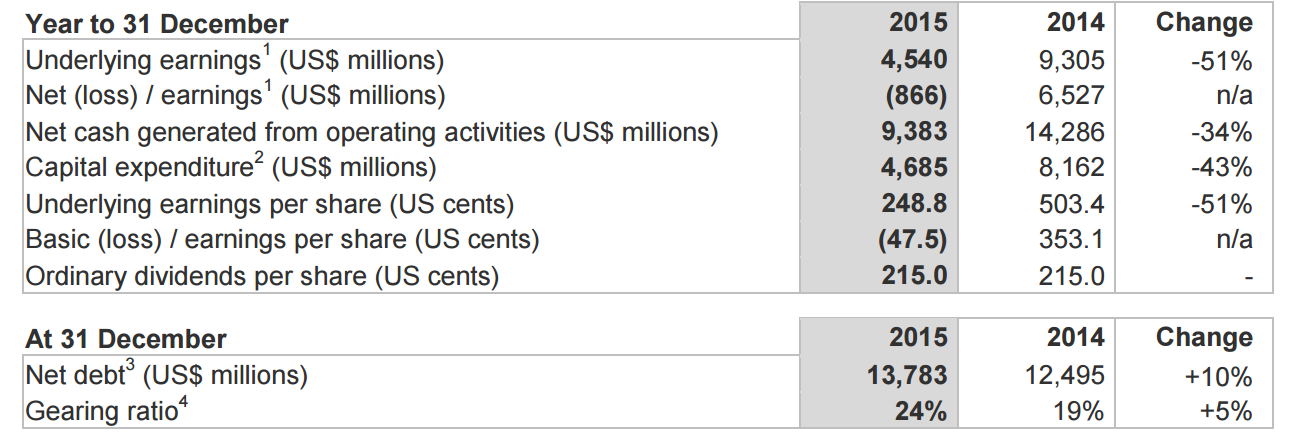

Reality is biting at RIO. Here is its full year profit:

Rio Tinto chief executive Sam Walsh said “Against a highly challenging environment, Rio Tinto delivered a strong performance in 2015 with underlying earnings of $4.5 billion. We continued to take decisive action to preserve cash through further cost reductions, lower capital expenditure and the release of working capital. This focus on cash resulted in operating cash flows of $9.4 billion.

“At the same time, we have significantly strengthened our balance sheet and finished 2015 with net debt of $13.8 billion, which is $700 million better than the $14.5 billion pro-forma position at the end of 2014.

“The continued deterioration in the macro environment has generated widespread market uncertainty. We are embarking on a new round of proactive measures to cut our operating costs by a further $1 billion in 2016 followed by an additional goal of $1 billion in 2017. We are also reducing our capital expenditure to $4 billion in 2016 and $5 billion in 2017, an overall reduction of $3 billion compared with our previous guidance.

“These significant actions provide us with the confidence that we remain robustly positioned to maintain both balance sheet strength and deliver shareholder returns through the cycle.”

Rio Tinto chairman Jan du Plessis said “The board has announced today a final dividend of 107.5 US cents per share, bringing the 2015 full year dividend to 215 US cents per share, in line with 2014.

“Over the past five years we have returned more than $25 billion to our shareholders, underlining our commitment to shareholder returns. However, with the continuing uncertain market outlook, the board believes that maintaining the current progressive dividend policy would constrain the business and act against shareholders’ long-term interests. We are therefore replacing the progressive dividend policy with a more flexible approach that will allow the distribution of returns to reflect better the company’s position and outlook. For 2016, we intend that the full year dividend will not be less than 110 US cents per share.”

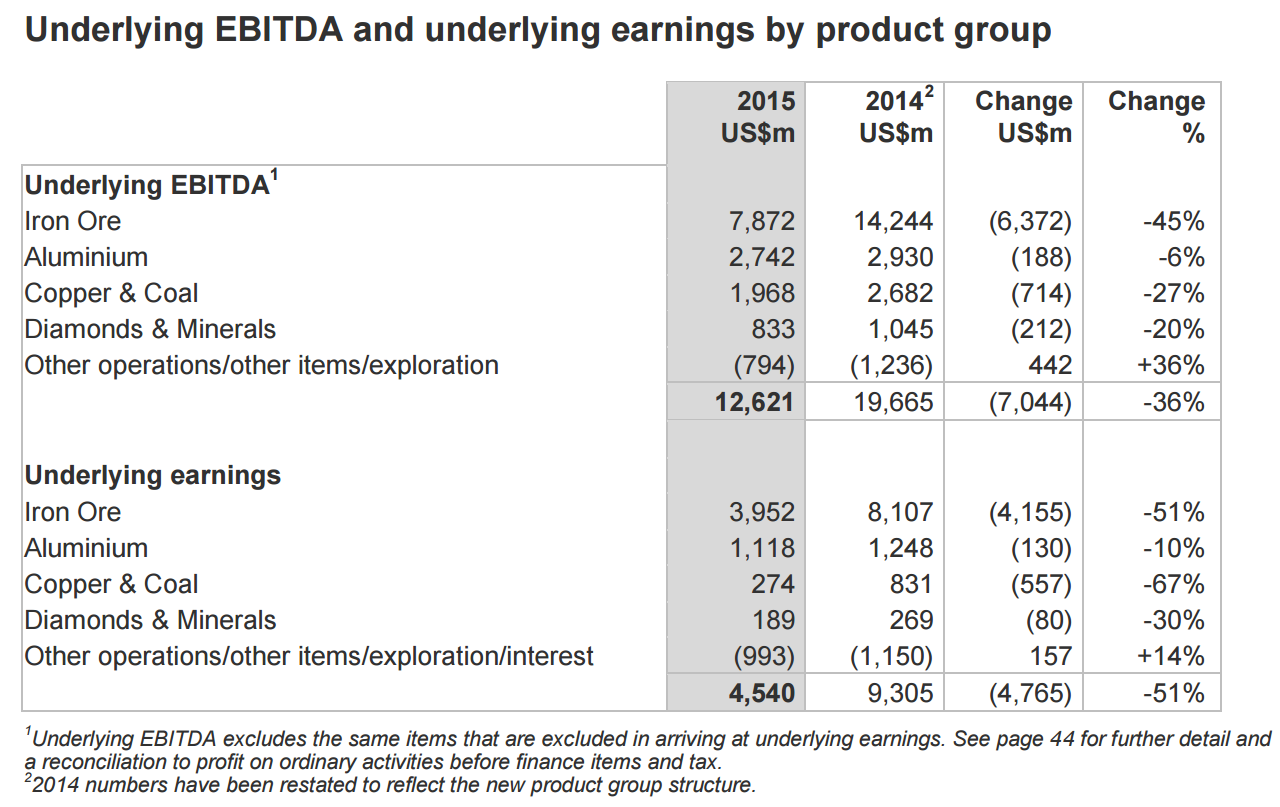

So, a net loss on halved underlying earnings and $1.8 billion impairment on Simandou and uranium. The progressive dividend is gone and next year’s has been virtually halved. Cost cuts galore. Here are the divisions:

Advertisement

Everything fell.

London hit it -3.5% but that is not enough. These earnings are garbage. There is no apparent growth in anything to offset the iron ore collapse which has much further to go. The writedowns of everything ahead are breathtaking. Capital management is history with no buybacks and a fading dividend.

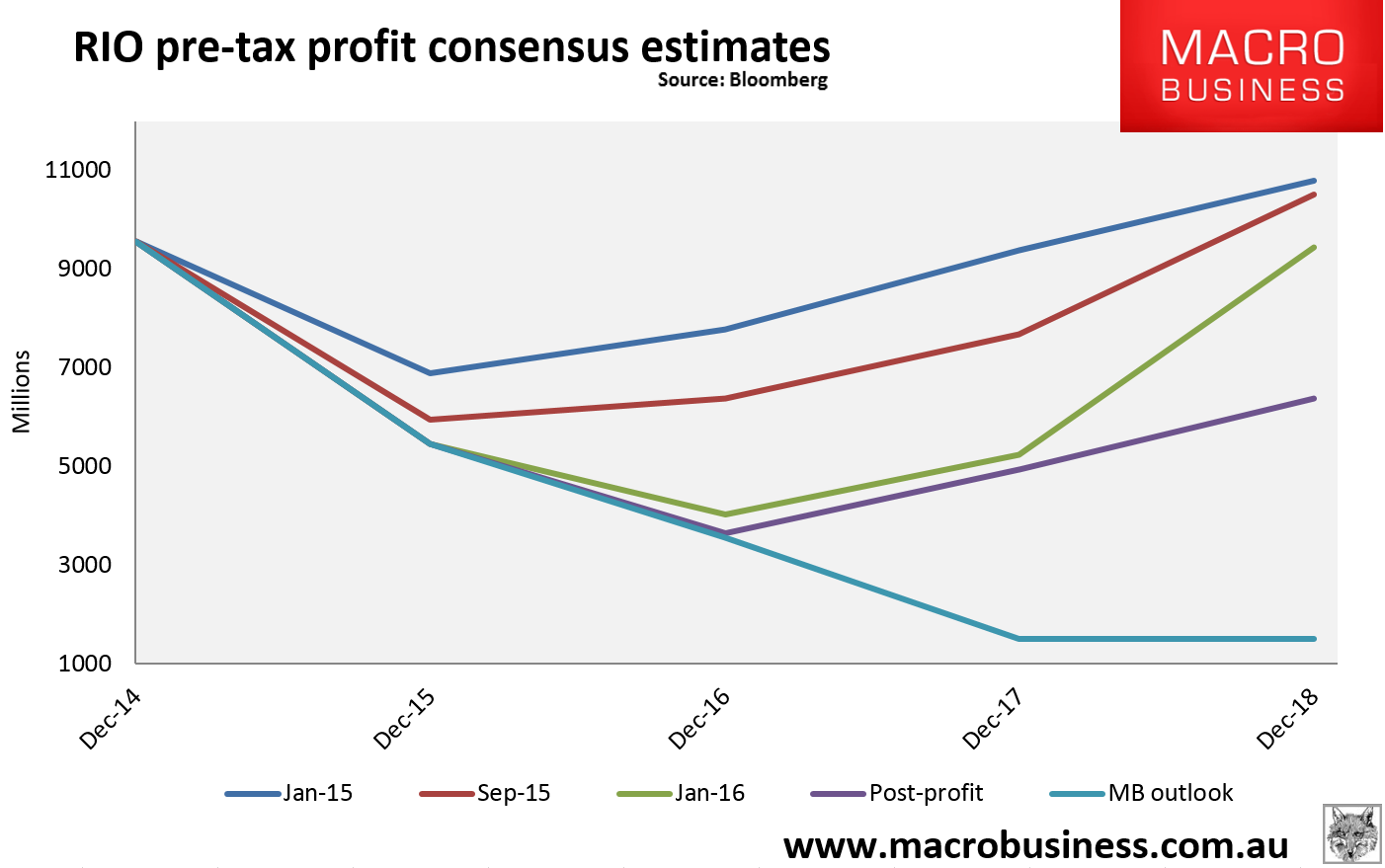

I have no idea why anyone would own this. It’s clearly a business getting sucked into a vortex which is quite plain in the evolution of consensus earnings estimates:

Advertisement

Consensus forecast earnings for 2018 just collapsed -40% yet the stock fell -3.5%?

I’ve also cut the MB outlook a little owing to the failure of non-iron ore earnings to pick up the slack and that outlook relies entirely upon a smooth Chinese rebalancing in which I no longer believe.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.