Remember all of those splendid RBA charts that used to forecast an endless boom in Chinese steel demand owing to low steel-intensity per head versus Western nations?

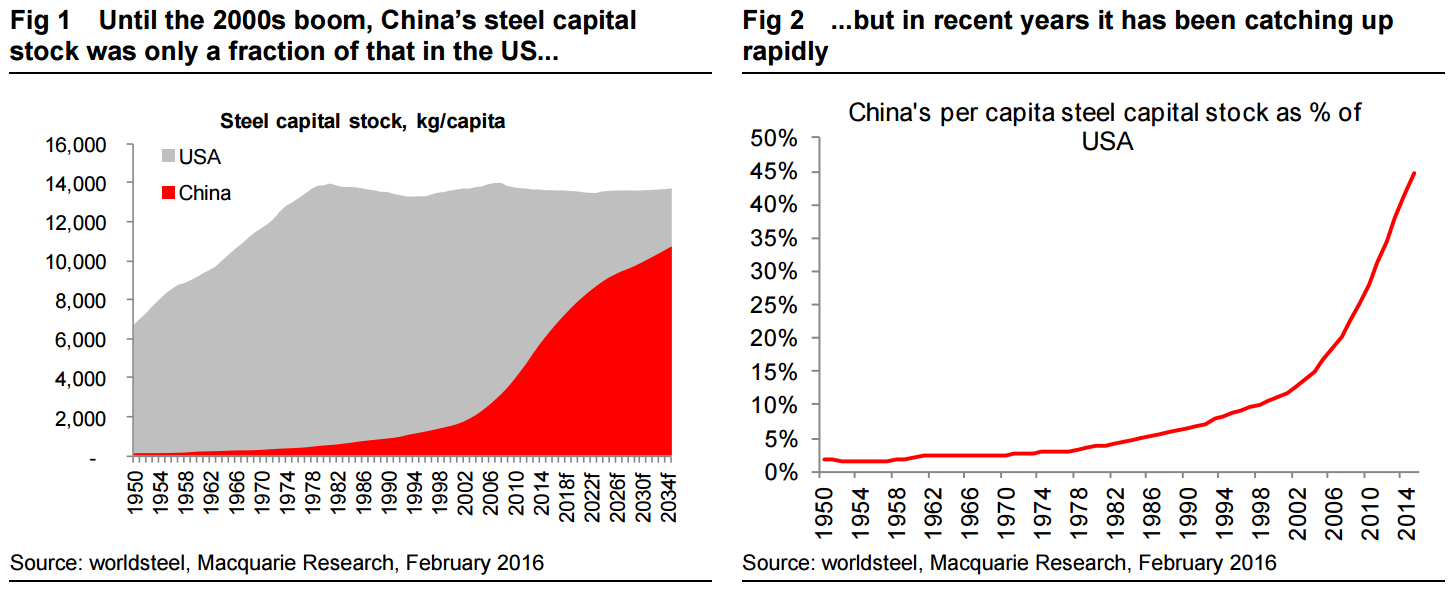

Until 2000, China’s capital stock of steel per capita barely registered. However, since then the rapid growth in demand has seen a build of stock at a level never before seen. While Chinese steel has now passed peak rates of consumption, the rate of consumption of course still remains elevated relative to history. This, when coupled with the fact that scrap generation in China is still in its infancy (owing to the youthfulness of the steel economy) means capital stock is still on the rise, a trend which will continue in the coming years. Fig 1 Until the 2000s boom, China’s steel capital stock was only a fraction of that in the US.

With this, it is fair to say China is not yet a fully developed steel economy. While total capital stock in terms of absolute tonnes surpassed the US in 2009 (and Japan in 1990), given the larger population the per capita level is much lower. However, having been only ~10% of the US level back in 2000 it was 45% in 2015 based on our calculations. Moreover, actual consumption per capita is currently around 1.5x that of the US.

So, how quick will China catch up with the US and Japan? When does it become fully developed in steel terms? We have run three scenarios here, keeping US and Japan capital stock per capita relatively fixed (but accounting for expected US population growth). The first is the ‘peaking out’ scenario favoured by global miners where Chinese consumption rates remain at peak for the foreseeable future. Here the catch up to US/Japan takes 20-25 years. The second is to assume our 2020 China consumption estimate (~12% lower than peak) into the future. Here it is a 25 year catch up to Japan, and 29 years to the US. Lastly, we have looked at a scenario where the drop from peak to steady state is 35%, which puts Chinese steel consumption at 500mt per annum. Under this scenario, China would have to wait 36 years to hit Japan’s level and 42 years for the US.

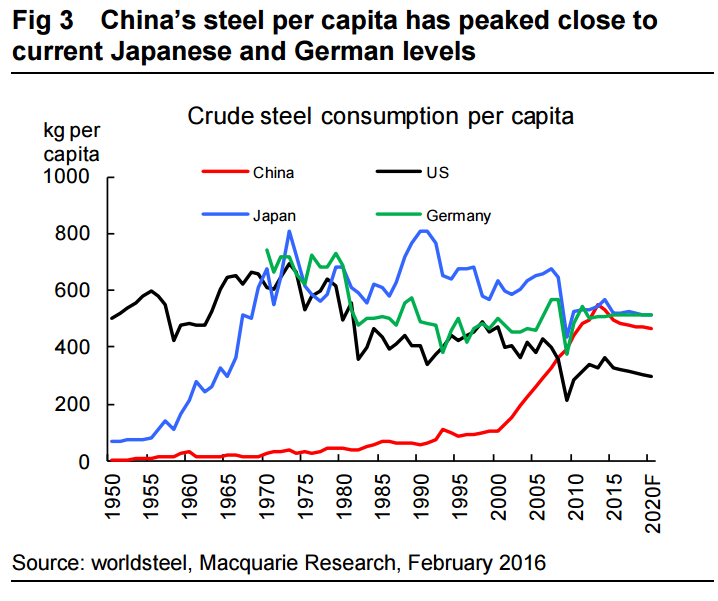

Certainly, it is fair to say China still has a way to go to become fully developed under the capital stock analysis metric. It should be noted however that we do become more efficient in using steel and other materials over time, perhaps best demonstrated by the fact that Chinese consumption per capita has peaked out lower than the precedents in Japan, Germany or even the US. As a result, comparison with the precedent capital stock may also give a false result. This can be important, as were we to use 80% of the previous peaks as a ‘developed’ level, on our current consumption estimates China would be more or less there by the middle of the next decade. Thus, understanding China’s development will still be key to global metals and mining markets for years to come.

Looks mostly caught up, especially since its steel-intensity and steel capital stock has hugely outstripped its relative wealth.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.