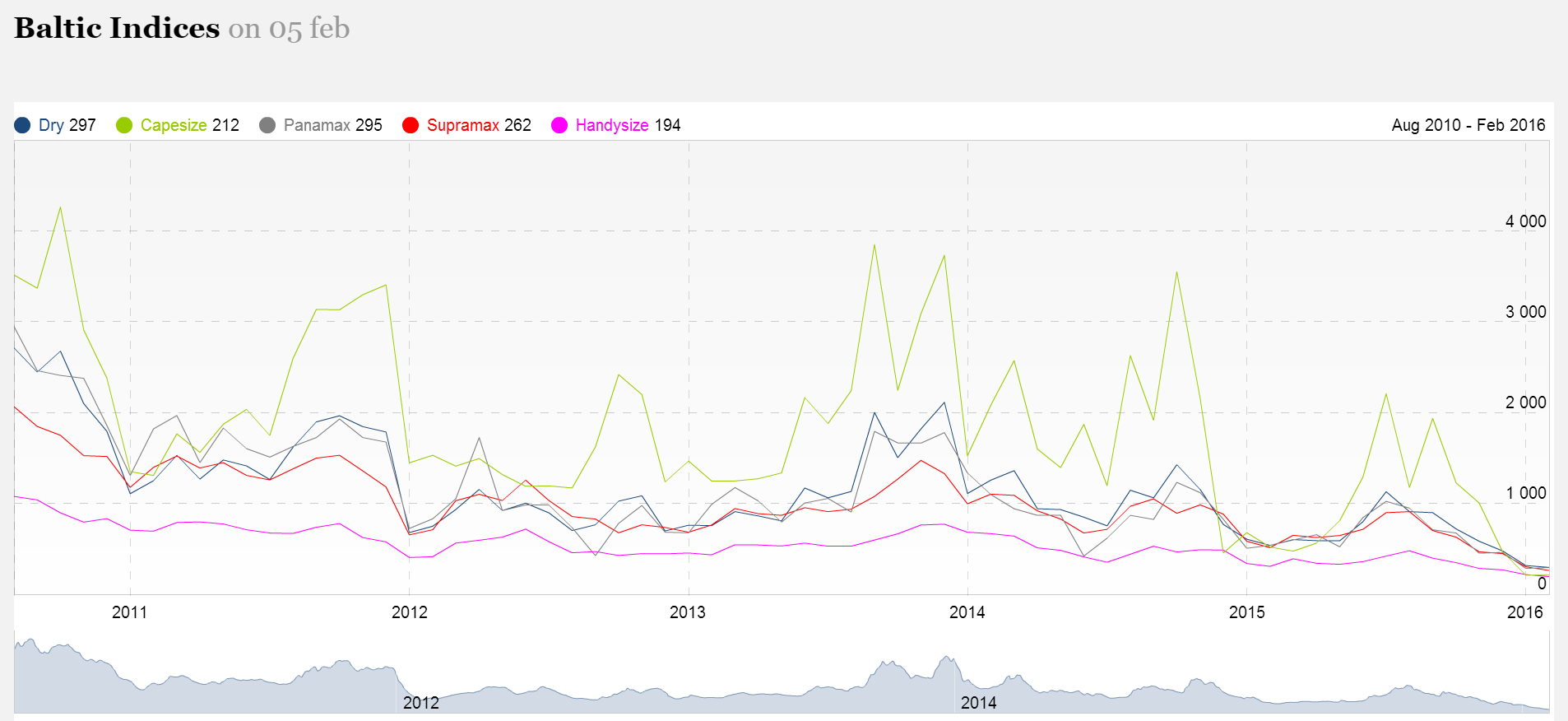

Nothing gets the bears roaring like a crash in the Baltic Dry Index (BDI) and right now it is trading at record lows:

Bears like to point to falls in the BDI as an indicator of imminent doom. In truth, it lost much of its correlation with growth in the GFC.

The BDI is useful now in two ways. First, it’s relentless slide is not a cyclical indicator, it is structural. During the boom, ships were overbuilt:

And, just like the last boom, during Japan’s build out and commodity spike, we’re left with a large glut afterwards when the party slows. So, the BDI is telling us not so much that China or the global economy is falling off a cliff but it is changing permanently towards a different pattern of less commodity-intensive growth to what was expected.

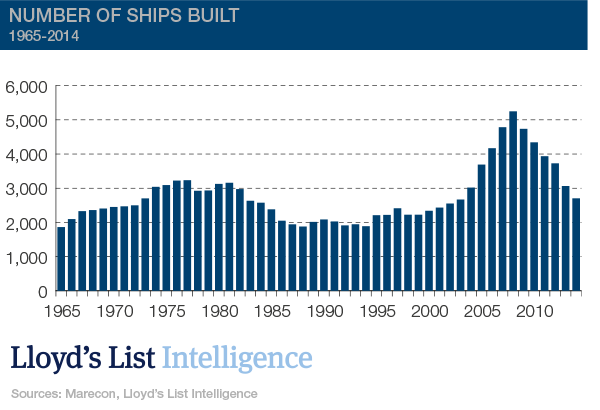

Second, this giant shipping glut is a quite useful metaphor for how much further the commodities bust has to run, especially in steel. The build-out of the global shipping fleet is a nice illustration of how the steel cycle feeds upon itself. During the boom, it takes a lot more steel to make a lot more steel. And as we head down the slope on the other side of that boom, the world will consistently be shocked by declining demand in part because the commodities supply chain itself will no longer be consuming steel.

In the case of ships that will not only mean less construction but one mighty pile of scrap to recycle.