Right on cue, the property lobby has re-emerged to caution against any changes to negative gearing, arguing that it would not boost the Budget. From The Australian:

Cutting back negative gearing would add nothing to the government’s bottom line…

Aussie Home Loans founder John Symond warned of the ripple effect of targeting individual parts of the tax system, saying “it was fraught with danger” for the government to change parts of the system in isolation. “A piecemeal band-aid job won’t be effective and could well provide more negatives than positives”…

Susan Lloyd-Hurwitz, the chief executive of Mirvac — one of Australia’s largest developers — also warned of unintended consequences. “At a time of massive volatility and value destruction in global markets, we would hope that any consideration towards changes in negative gearing be thoroughly thought through, as Australia’s housing markets have been a source of great stabilisation, stimulus and confidence in a time of widespread transition and disruption”…

Forecaster BIS Shrapnel modelled a number of scenarios where negative gearing was pared back, and said the government would have to compensate lower income earners, undermining any savings.

All smells like blatant rent-seeking.

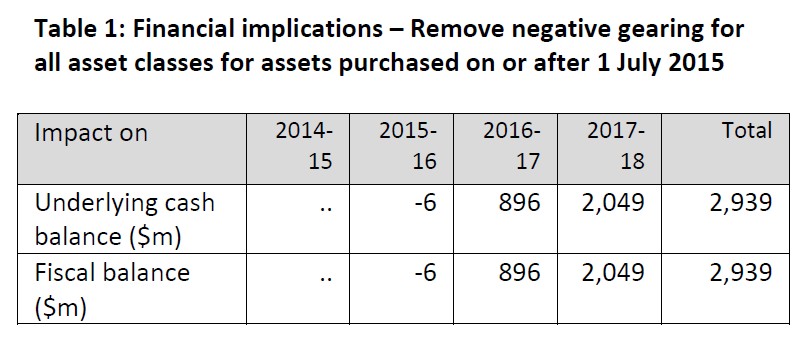

Last year, the Parliamentary Budget Office (PBO) costed the Greens’ plan to quarantine negative gearing so that rental losses on both houses and shares could no longer be claimed against unrelated wage/salary earnings, with those already holding negatively geared investments grandfathered, so that the reforms would only affect new investors from a specific date.

The PBO estimated that the Greens’ plan would increase Budget revenue by $2.94 billion over the 2014-15 forward estimates, assuming the policy was implemented for all asset classes purchased on or after 1 July 2015. This includes $2.95 billion in revenue and $11 million in departmental expenses to administer (Table 1).

Moreover, the PBO estimated the proposal would increase revenue by $42.5 billion over the period to 2024-25.

As I argued at the time, the Greens’ proposal is the best way to reform negative gearing.

By grandfathering existing investors, political backlash would be minimised from the circa 1.3 million Australians holding negatively geared properties, thus making it a realistic reform option (as opposed to a pipe dream).

Nevertheless, there would still be a significant dampening effect on the housing market, since home prices are set at the margin by new entrants.

The resulting ‘correction’ in home prices resulting from the Greens’ policy would likely also be far more orderly than if negative gearing was banned outright, since it would not cause a sudden flood of sales from existing investors exiting the market.

Including both property and financial assets in the Greens’ negative gearing policy is also sensible, since it would minimise tax distortions and overcome concerns about unequal tax treatment between asset classes.

In short, there are great gains to be had from genuine negative gearing reform. And the property lobby is merely talking its book.

As an aside, compare Aussie John Symond’s comments on negative gearing above with his comments in 2014:

Aussie Home Loan founder John Symond told AFR Weekend the tax break [negative gearing] favoured investors and was distorting the property market.

“Negative gearing is a great tax break, but it needs a total overhaul to make it fairer. First home buyers have no hope of getting into home ownership these days unless they’re helped by their families,” Mr Symond said…

“They’re walking away from what used to be the great Australian dream,” he said. “But with interest rates at their lowest point in history, and house prices only just coming off the bottom, if first home buyers can’t afford property now, they never will,” he said. “I’m very pessimistic on the outlook for them.”

Inconsistent much?