The Brent oil price rocketed 9% plus Friday night for no reason beyond the same UAE comments we saw Thursday. Henry Hub gas slumped to $1.96mmBtu:

The UAE rumours are fluff but markets are way short so got squeezed anyway. At some point this empty OPEC jawboning is going wear out on the market.

In other bullish news the US rig count fell sharply again down 30 to 541. The EIA has a nice take on the state of play:

Advertisement

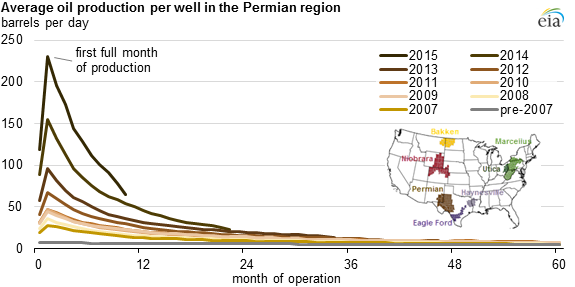

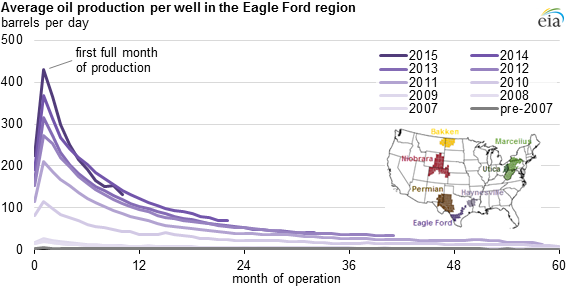

Tight oil production in the United States increased from 2007 through April 2015, based on estimates in EIA’sDrilling Productivity Report (DPR), and accounted for more than half of total U.S. oil production in 2015. Tight oil growth has been driven by increasing initial production rates from tight wells in regions analyzed in the DPR. As drilling techniques and technology improve, producers are able to extract more oil during the initial months of production from new wells.

The average new well in each of these regions produces more oil than previous wells drilled in the same region, a trend that has continued for nine consecutive years. The increasing prevalence of hydraulic fracturing and horizontal drilling, along with improvements in well completions and the ability to drill longer laterals, has greatly improved well productivity. This trend can be seen in the continued increase in initial production rates since 2007, and it has allowed production in major shale basins to be fairly resilient despite high decline rates common to drilling and producing in tight formations and, since 2014, the declining number of rigs drilling for oil.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.