According to MNI, new loans so far in February were similar to the levels during the same days of January. The total so far in February is seen at around CNY2 trillion already.

MarketNews adds that this was achieved despite fewer working days in February because of the lunar New Year holiday, suggesting even more loans were churned out every working day.

The surge was surprising. As MNI reports, the strong January numbers had been expected to moderate for a number of reasons.

Firstly, Chinese banks typically try to get as much loan money out the door as possible early in the year to maximize interest income for the rest of the year.

Secondly, Chinese companies have been paying down foreign debt on expectations that the yuan would continue to weaken and that process has been expected to slow.

Thirdly, and perhaps the biggest surprise in the February loan growth thus far, loans for government infrastructure projects that helped boost the January data were expected to slow. That does not appear to be happening.

Mizuho said in a note to clients late Wednesday that a massive stimulus package is likely in the pipeline.

“We expect public infrastructure projects to receive another boost to stabilize the economic downtrend. This may include construction of intra-city railways, railways in the central and western provinces and making improvements in the agricultural sector. A new round of massive stimulus, in our view, will be announced around the National People’s Congress, which will likely convene in the second week of March,” said Shen Jianguang, chief Asia economist at Mizuho Securities Asia Ltd.

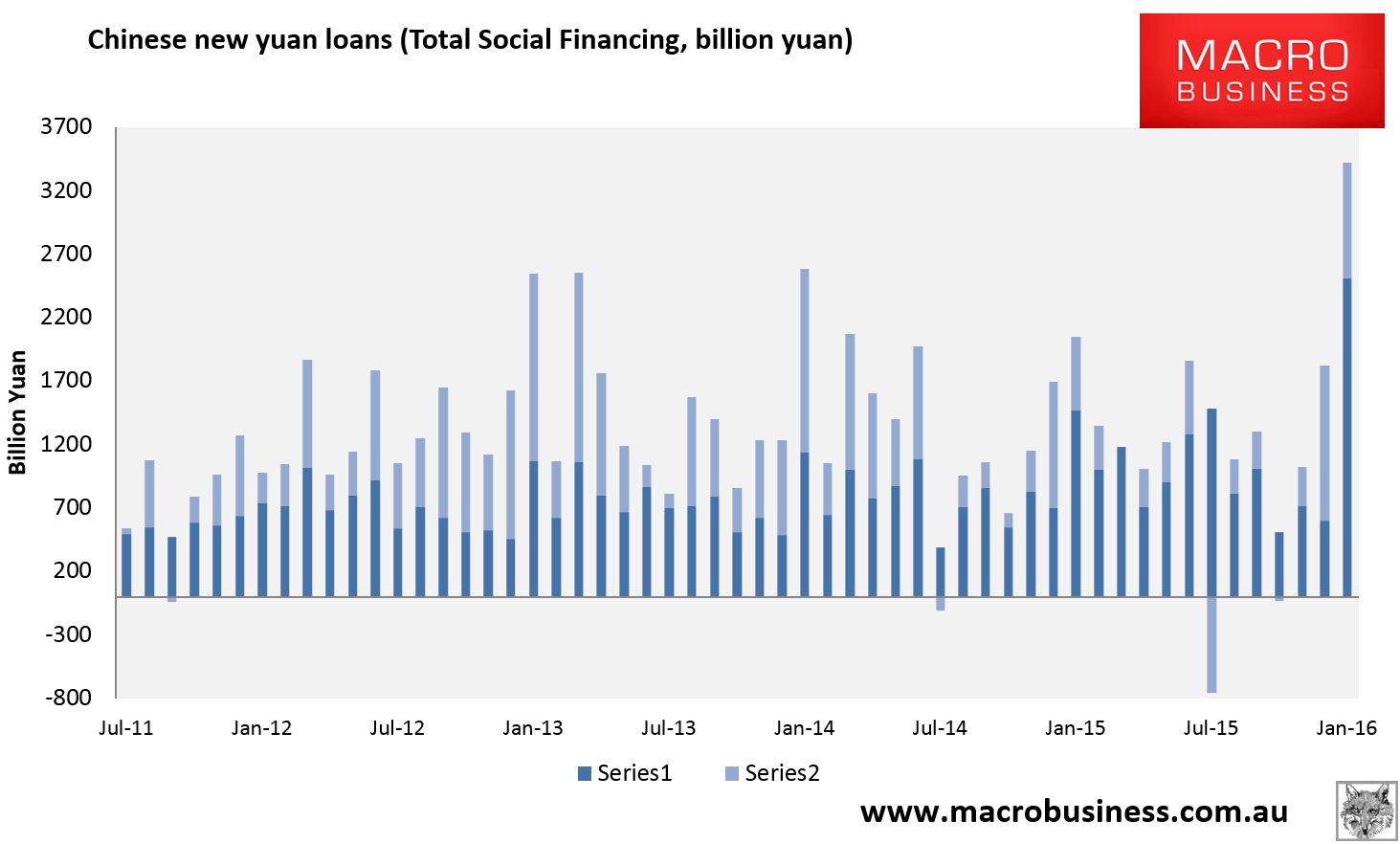

To be sure, the immediate impact from this credit surge will be favorable, if only in the near term as the following chart shows:

On the heels of Li Keqiang saying the government can do more to prop up the economy comes more stimulus rumors. At this point, there’s no evidence to suggest this isn’t more of the same talk/policy we’ve seen over the past two years.

The nation’s chief planning agency is making more money available to local governments to fund new infrastructure projects, according to people familiar with the matter. Meantime, China’s cabinet has discussed lowering the minimum ratio of provisions that banks must set aside for bad loans, a move that would free up additional cash for lending.Some people are happy with more talk though:

“After many complaints about poor communications, Chinese officials seem to have gotten the message,” Win Thin, the global head of emerging-markets strategy at Brown Brothers Harriman & Co. in New York, wrote in a note to clients.The Chinese government has a different way of sending messages. Nothing has fundamentally changed.

And to ram the message home, the biggest economic planning agencies on Tuesday promised to reduce financing costs as they rein in overcapacity. Throw in a record surge in lending in January and a picture emerges of an administration determined to put a floor under growth.That has been one of Li Keqiang’s top reforms. He was focused on lowering financing costs for SME, and 70% of SMEs Have Seen Financing Costs Rise in 2015.

The major changes to date are the push to reduce overcapacity, which now has moving parts such as the worker stabilization fund, and recognition of rising bad loans. The core message hasn’t changed though. No major stimulus, no repeat of 2008, rely on supply side reforms.

That seems to me a better assessment. As I noted earlier this week, the January surge in credit is an unreliable indicator given the huge refinancing underway as US dollar loans are dumped:

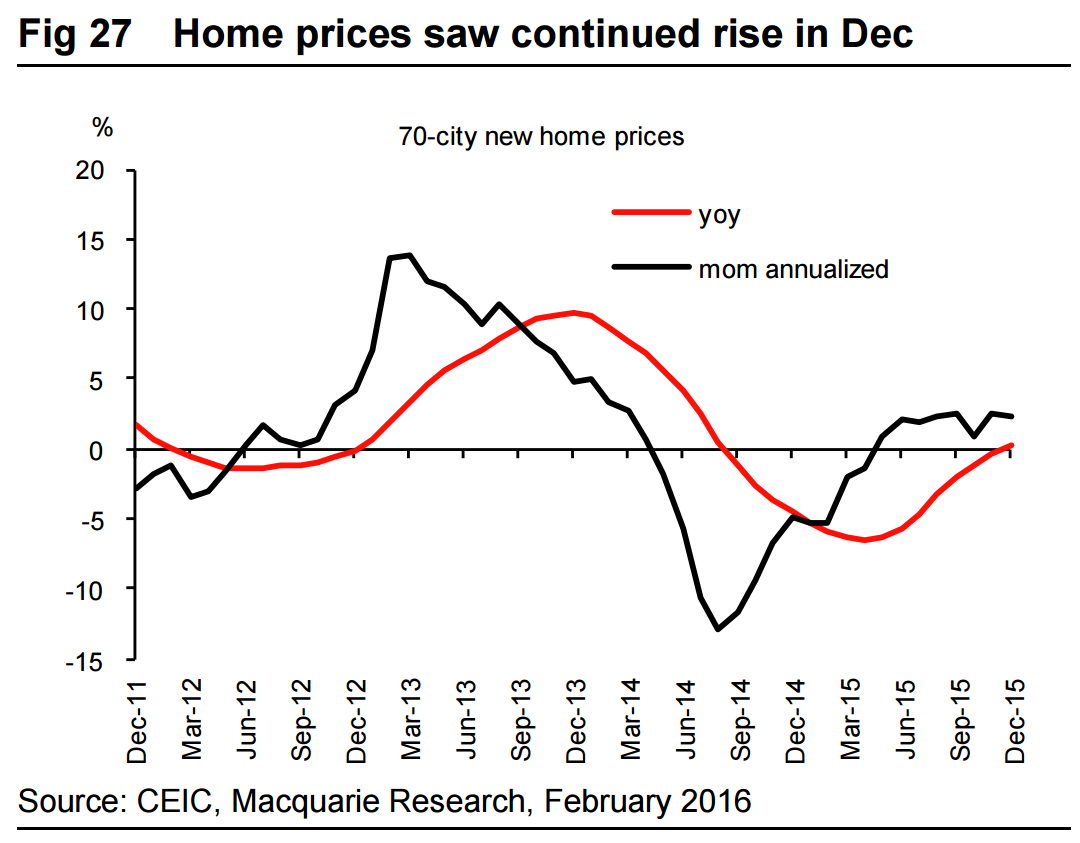

Moreover, I do not expect this “massive stimulus” if it comes to be very effective in raising growth for very long. At best for a quarter or two. The major reason is that it will not reach the real driver of growth, the property market, in any meaningful way. A couple of charts from Macquarie tell the tale. The price recovery is very weak because it is localised to first tier and some second tier cities:

Advertisement

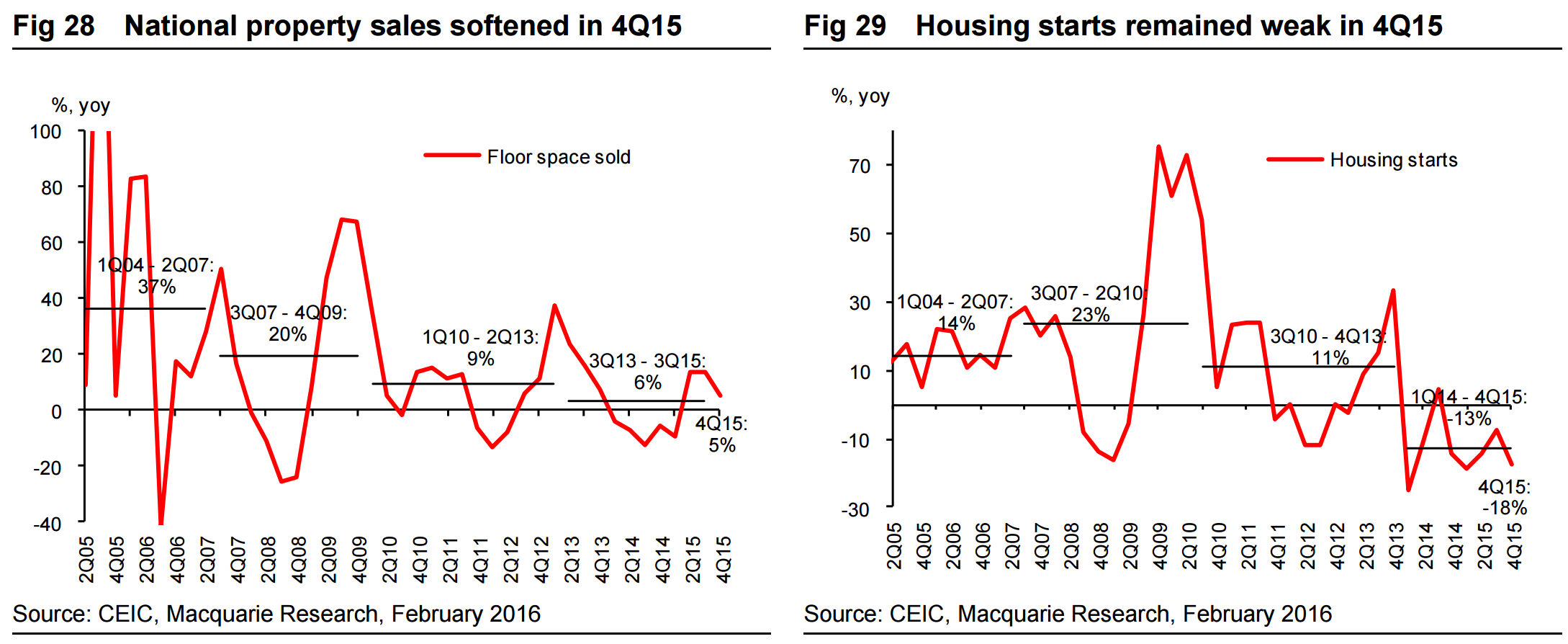

And housing starts by floor space are still down -15% on a rolling annual basis because 75% of construction is in oversupplied third and fourth tier cities:

Advertisement

Residential construction accounts for roughly 40% of Chinese steel consumption and infrastructure half of that. As well, manufacturing is another roughly 30% and it is also contracting.

So, this is more glide slope management not any trend change but given how far China has run down its steel stocks under pressure from falling prices, it may well extend for a few months the current round of restocking for both it and iron ore.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.