by Chris Becker

Calm descended on most risk markets overnight as the fallout from the NY day volatility on Chinese equity markets started to dissipate. A small bounce on stocks in Europe and the US was extended into slight gains on bond markets, but commodities were mixed as oil dropped but precious and industrial metals gained. Germany’s all-important unemployment print and the final CPI print for the EU saw the Euro sold off against the USD.

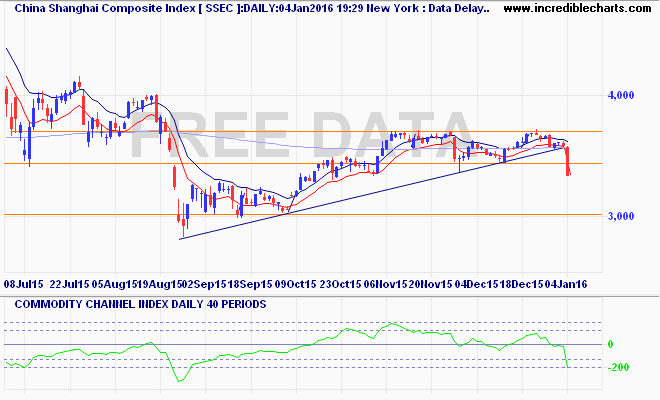

Recapping Asia’s session where the Shanghai Composite initially gapped down but recovered after the lunch session, only falling a quarter of a percent following its 7% loss the day before. This is the calm before the storm for mind – terminal support at 3000 points is key here- if that’s broken, think 2000 points real quickly:

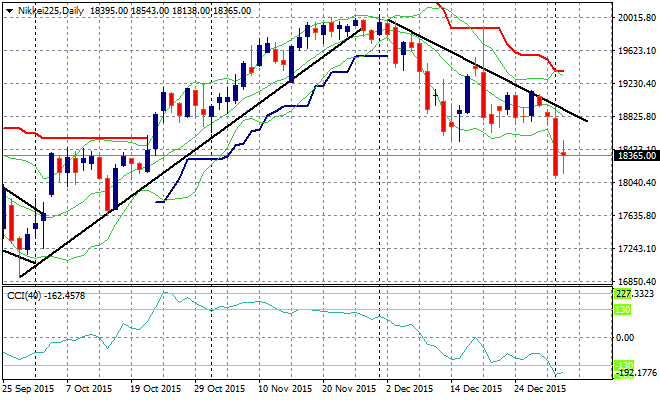

The Nikkei 225 fell slightly but regained most of this in overnight futures trade, following the positive US lead. The ever strengthening Yen is putting the brakes on any recovery here as the downtrend remains well intact, but momentum is extremely oversold. I’m looking for a swing up to that trendline, but again watch the real trend in Yen:

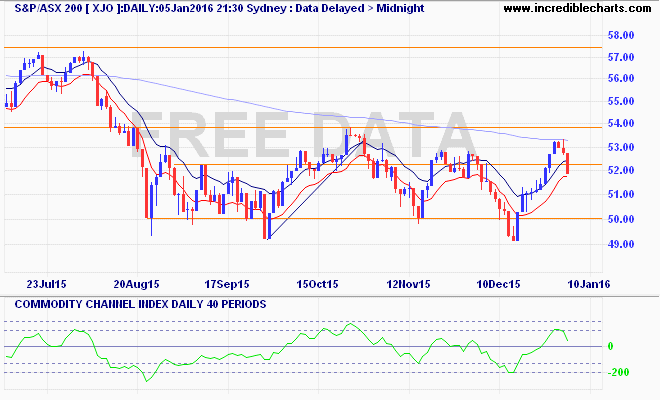

The ASX200 fell sharply yesterday, finally catching up to its Asian brethren, down 1.65%, although SPI futures are pointing to a small rise on the open. As I thought yesterday before the open, bank stocks were heavily hit – perhaps on the Dick Smith fallout, more likely on general bearishness – as the 200 day moving average is rejected on the daily chart. We’re setting up a long sideways move from support at 5000 points and resistance at 5400 points that has a downwards bias:

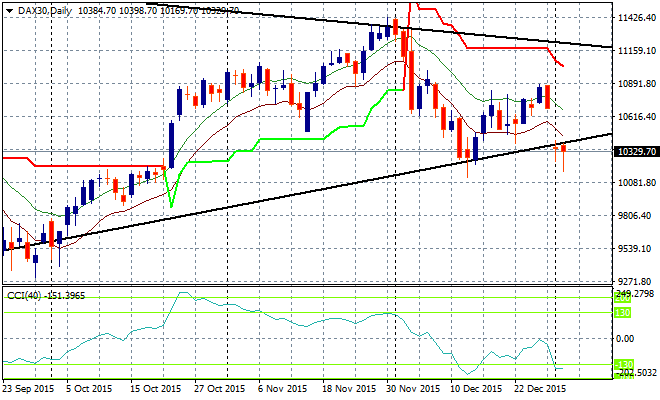

On to Europe, where the German DAX came back after its 4% loss on Monday, but only just. Its hovering around the mid-December lows just above 10,000 points but remains under its longer term trendline as well:

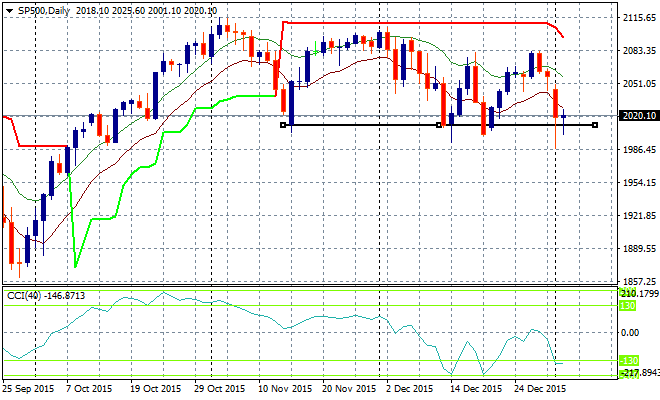

US stocks continue to looking stretched, but there was general recovery overnight, except in the NASDAQ. The S&P500 is still finding support at 2000 points as daily lows remain unbreached but the lack of confidence here in price action is very telling:

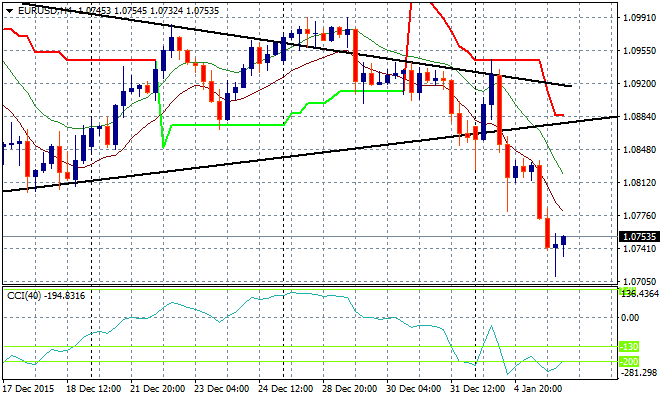

On to currencies, where the Euro fell straight through the 1.08 handle again, without my expectations of a small swing in the middle of the session. It almost went through 1.07 against the USD before settling at the 1.0750 level and ripe for a swing today. But the longer term position is now down as that daily trendline is broken:

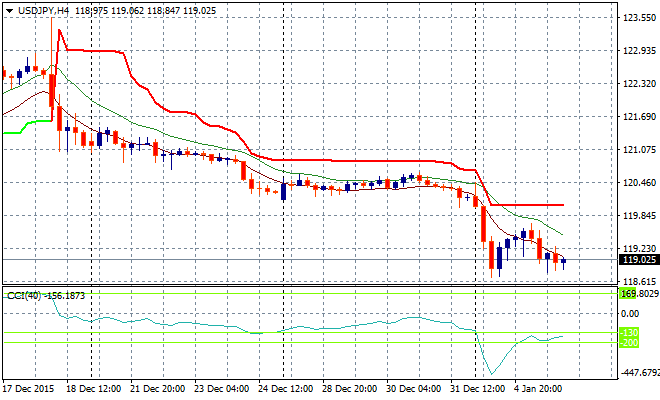

Yen remains strong against the USD with the USDJPY pair falling through the 119 handle in a large downmove that continues to surprise. I’m still expecting a bounce here, as we’re getting very close to the August and October 2015 lows from the last bouts of USD strength:

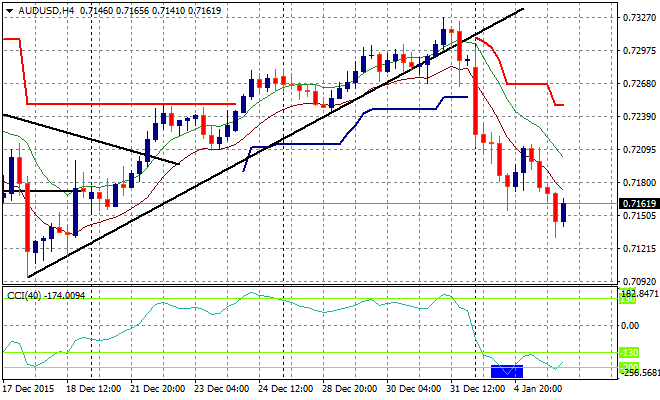

The Australian dollar continues to deflate going into 2016, now solidly below the 72 cent handle against the USD. This week, as more data rolls in, I’m watching the weak uptrend from the 71 handle support level for signs of a breakdown, but for mind we’re setting up for a swing particularly if the data surprises on the upside:

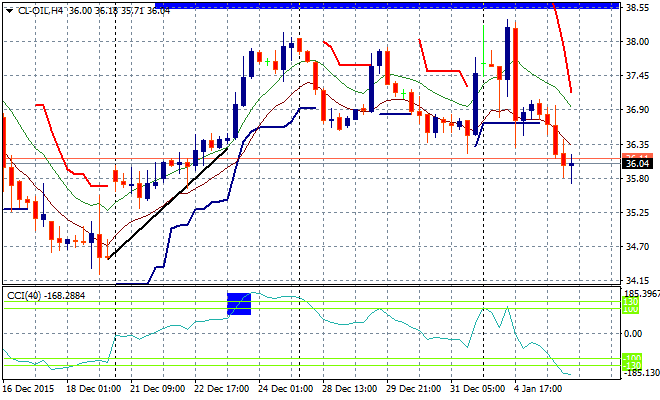

Oil is now definitely showing signs of breaking down as the Middle East roils with both Brent and WTI falling over 2% overnight. Support at $36.30 has been taken out on the four hourly WTI chart, with the $34 low the next target here:

Is gold finding a base here? Its not falling, so thats a good start for 2016, with the shiny metal – plus the other precious and more useful metals – rising overnight to $1077USD per ounce. ATR resistance at $1100 is the key level to break on the upside, while support at the $1060USD level remains the key breakout level going forward:

The data calendar rolls on with some important prints out today in Asia – Australian, Japanese and then Chinese services PMIs in that order. In Europe its the UK services PMI, then the US trade balance and ADP employment stats before the equally important US ISM-services and factory orders print. A big night!