Asian markets have struggled to hold their strong open today. The weight of China seemed to steadily push the steam out of the markets in the lead up to the Chinese cash market open.

Unfortunately, Chinese markets quickly lost yesterday’s gains at the open. The ambitious call-to-arms by a group of 28 companies on the ChiNext does not look it will lead to sustainable gains in that market either, although it is outperforming the Shanghai Composite today.

In credit to the People’s Bank of China’s efforts, the daily CNY fix has increasingly become a dull affair. But with volatility quelled in the CNY, FX traders are increasingly turning to proxies to express their bearish views. This should be an increasing concern for the Aussie and Kiwi dollars, both of which dropped more than 0.5% immediately after the CNY fix at 12.15 pm AEDT.

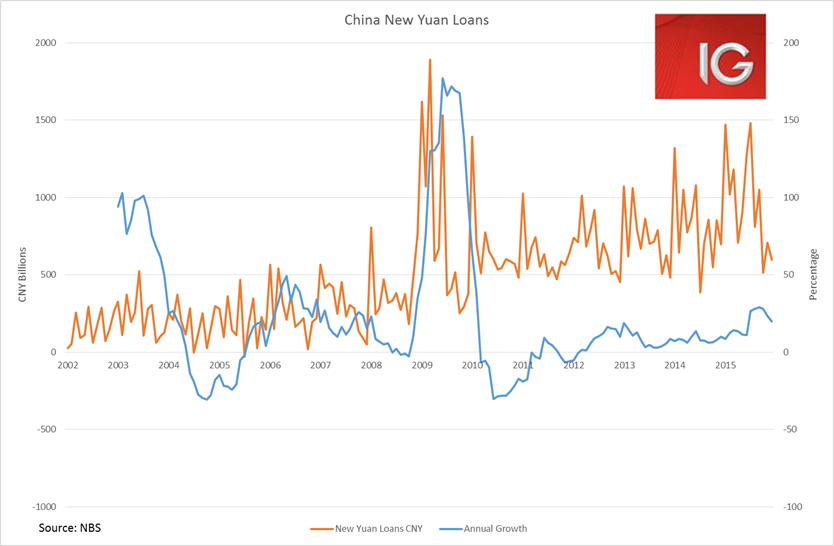

China’s latest monetary and credit data have underlined the growing issue of access to capital to small and medium enterprises (SMEs) in China. While Total Social Financing (TSF), China’s broadest credit measure, was better than expected, seeing a net increase of RMB 1.82 trillion, new yuan loans had another very weak month. Growth in new yuan loans has weakened considerably in Q4 after what was quite strong growth throughout 2015.

The other pertinent aspect of this data is the big increase in off-balance-sheet financing, which is evident in the breakdown of the TSF data. There was a big jump in entrusted loans, which saw a net increase of RMB 353 billion, its biggest month since December 2014. Bankers’ Acceptances also saw a major jump, seeing an additional RMB 154.5 billion, which have mostly been in contraction throughout the year; it was the biggest addition seen since January 2015.

The drop off seen in SMEs in the NBS and Caixin PMIs does increasingly look like it is related to a lack of access to capital. The rising NPLs at Chinese banks are likely crimping their desire to extend new yuan loans, which is forcing SMEs to increasingly turn to off-balance-sheet funding. The fact that China’s fiscal and monetary stimulus is not reaching China’s most important part of the economy should be a major concern. China’s ongoing consumption and tertiary sector growth requires the SME and private sectors to continue to thrive. Despite the improvement in aggregate statistics, there does look to be a growing issue here.

Australia

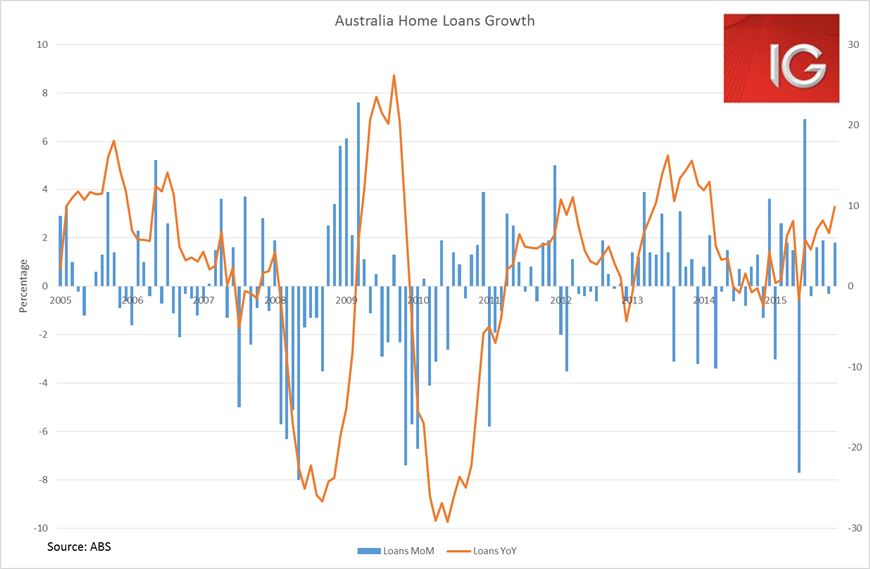

Despite the vicious selloff we’ve seen in the ASX in 2016 the domestic economy has not fallen off a cliff. Yesterday’s employment figures emphasised that there was still momentum in job growth. While today’s home loans data also came in better than expected with notable increases seen in owner occupied and investor lending in November. While total home loan growth expanded at 9.9% year-on-year, its strongest growth since February 2014.

Nonetheless, this did not help lift the ASX. The continued selloff in Chinese equities has seen the ASX trading back at its lowest levels since mid-2013.

BHP announced a US$4.9 billion write down of its US shale assets. Ahead of the announcement its ADR was pointing to a 7.4% gain at the open. But the scale of the write down appears to have taken a lot of the steam out of the stock although it managed to stay in positive territory. Unfortunately, it does not look like we have seen the bottom in BHP. Iron ore is still trading above US$40 and there is a good possibility that we may see a cut to its dividend policy, changes to either are both likely to see the stock go even lower.

Despite a few sectors remaining in positive territory today, the banks sold off heavily. Financials as a whole were down 0.9%, one of the worst performers on the index. And with the dramatic reweighting that we have seen of the ASX towards the financials now, it is very difficult to see much of a turnaround until the banks start catching a buy.