The report is unique because it uses water use data from Melbourne’s three main metropolitan water retailers to determine whether a home is being used, with very low recordings of water consumption data used as a proxy to determine vacant dwellings.

Speculative Vacancies (SVs) are measured as properties with abnormally low water usage. That is, any residential landholding using less than 50 litres per day (LpD), averaged over a 12 month period is deemed a speculative vacancy. Average per capita water usage in Melbourne over 2014 was 160LpD.

In many cases, these are likely held for speculative gain by property investors. And because these properties are not for rent, they are overlooked by current short-term vacancy measures reported by real estate firms.

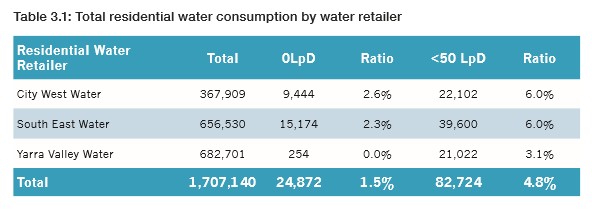

Analysis was undertaken of 1,707,140 residential properties across 254 postcodes over the calendar year 2014, with data sourced from Melbourne’s three main metropolitan water retailers, City West Water (CWW), South East Water (SEW), and Yarra Valley Water (YVW), who made their data available for this report.

Data indicates that 82,724, or 4.8% of Melbourne’s total housing stock appeared to be vacant over 2014, having consumed less than 50LpD. No water was consumed in 24,872 (1.5%) dwellings – therefore being demonstrably unoccupied.

If just those residential properties consuming 0LpD were placed onto the market for rent, this would increase Melbourne’s actual vacancy rate to 8.3%. Moreover, if 82,724 properties using under 50LpD were advertised for rent, the vacancy rate could rise to an alarming 18.9%.

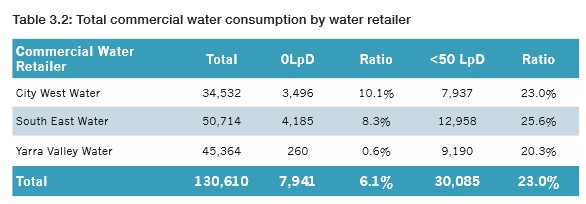

An examination of 130,610 non-residential properties across 254 postcodes over the same period identifies 7,941 or 6.1% of Melbourne’s commercial stock was also vacant over 2014, that is having consumed 0LpD.

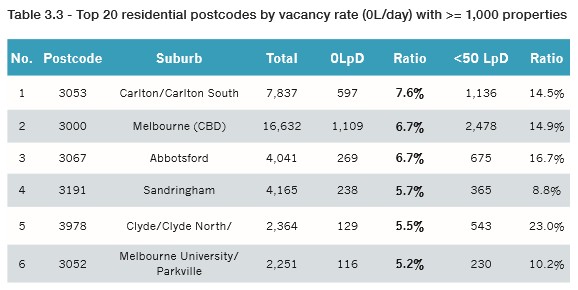

Mirroring the trend in previous reports, a large proportion of speculative vacancies can be found in the City of Melbourne and its immediate surrounds.

The breakdown by suburb shows that Carlton/Carlton South, Docklands in Melbourne’s CBD, and Abbottsford have the largest proportion of vacant homes, with a whopping 7.6%, 6.7% and 6.7% of homes respectively consuming zero water over the the 2014 calendar year, and around 15% using less than the 50LpD threshold (see below table).

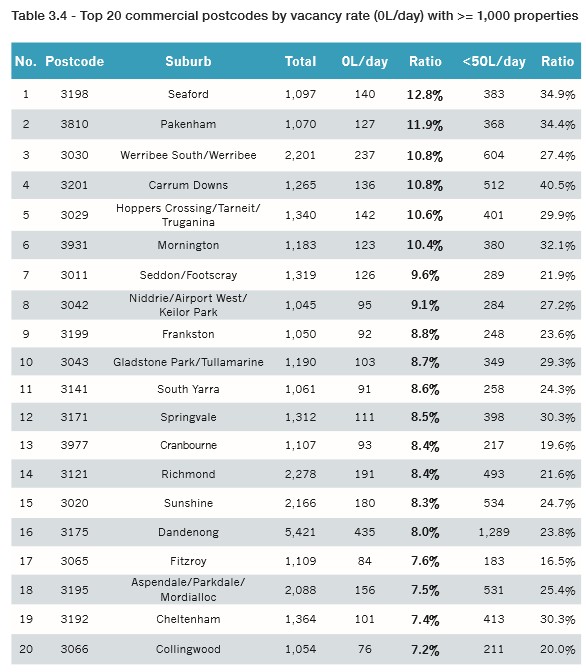

By contrast, the outer suburbs top commercial SVs (see below table).

The report likens the SV rate to the unemployment rate for land. If there were an 11% unemployment rate in a municipality, politicians would be under substantial pressure to rectify the situation. Yet in an alleged housing supply crisis these empty dwellings are largely ignored.

Vacant properties impose a needless economic burden, and residents and businesses are thereby forced to leapfrog vacancies to lesser sites at great cost, increasing commuting times and placing upward pressure on prices.

Moreover, latent supply is usually not visible without a significant downturn in economic activity. If withheld stock were put to use, it would reduce cost-of-living pressures for tens of thousands of low and middle-income families and businesses marginalised by the cost of land.

The report explains four key factors inflating apartment costs, which precludes affordable homes from being built:

Zoning Laws – “Plan Melbourne’s” zoning regulations sterilise a large percentage of primary neighborhoods from dense development. “Neighbourhood Residential Zones” (NRZs) are spread across many affluent suburbs, restricting development to dual subdivisions of no more than two stories. Additional design constraints enforced by some municipalities add to the complexity of the system – extending the time it takes for developers to gain planning approval.

In the limited areas where high-density development is permitted, story plus apartment blocks have been densely packed into streets where family homes previously dominated. This tightly limits land supply where high-density construction is possible and further elevates the already inflated values in the areas deemed suitable.

Construction costs – Development levies and lumpy infrastructure contributions are a prerequisite to construction and naturally passed to the buyer in the form of higher prices. Additionally, the physical impediments of building residential towers raises efficiency costs relative to low rise considerably, with increased floor areas required for structural supports, elevators, service ducts and so forth. Even if building costs were to reduce, the value would simply devolve to higher land prices.

Supply elasticity – Many developers currently gain funding offshore. However, financing can require up to 100 per cent debt coverage from pre sales. Projects take a number of years from concept to ‘lock up’ before supply can filter onto the market – a 3-6 year window not being unusual. Hence, supply cannot immediately cater to increased demand.

Inflated Commissions and Rental Guarantees – Buyers typically purchase the stock through financial intermediaries who receive inflated commissions to achieve necessary pre-sale targets. Meanwhile, investors are commonly ‘lured in’ with rental guarantees that promise a return that exceeds current market yields.

It also notes how supply policies on the fringes of the city are politically manufactured to keep prices elevated:

Precinct Structure Plans – Although an area may be zoned for residential development, building cannot commence until a precinct structure plan (PSP) has been completed.

Supply Elasticity – The PSP takes a lengthy 3 to 4 years from start to completion – during which time, speculation builds and land prices naturally increase.

Withheld land within PSPs – Once the process has been finalised, it does not guarantee housing will be constructed. For example, upwards of 50 per cent of a completed PSP can be held by existing landowners who have no intention of building, and until they do are excluded from making contributions toward infrastructure financing. This leaves active buyers paying the passed on premium without receiving the associated amenities – perhaps for years.

Development Levies – Total development levies and taxes on a house and land package can be partially passed onto the home buyer, in the form of higher prices. This would be alleviated by the infrastructure financing reforms in the recommendations of this report.

Staged Releases – When land is developed, plots are released onto the market in limited numbers to ensure supply does not exceed demand and owners receive a healthy return on profit. The drip-feeding is a form of price manipulation – ignored by State Government. In the process, land sizes (not land prices) are cut to maximise yield.

As a result, Melbourne is building the wrong type of housing:

The type of housing Melbourne is crying out for is accommodation suited to our biggest buyer demographic – families with children. However, with unit construction outpacing housing construction by a significant margin, it’s clear we have an over supply of poor quality dwellings and SVs that will not become visible until an economic crisis hits.

This trend of widespread vacancies is also noticeable in Europe. In Spain for example, 15 per cent of the dwelling stock is permanently vacant.

Studies have labelled it the ‘Mediterranean Paradox’ in which high vacancy rates and high house prices go hand in hand. As with Australia, dwellings are constructed and bought for speculation rather than housing need. With a large proportion of the new housing stock left unoccupied, increases in housing construction have not produced the expected surge in supply to aid future demand.

Finally, the report notes the damage caused by supply-side barriers:

Land banking is an especially damaging form of rent-seeking. Urban growth boundaries reduce contestability and the ability of competition (or the threat of competition) to hold down prices. They effectively allow oligopolistic returns by conferring market power upon landowners who reap the gains they did not sow.

The only statistic that matters for affordability is the volume of vacant land current owners plan to release onto market in the immediate future.

Under current policy, large developers have every incentive to drip-feed sites onto the market to keep prices elevated.

The process results in a type of ‘preventative speculation.’ Developers buy large land banks in advance of rezoning to protect and increase their profit margins.

There is no incentive to release this land in Victoria. The previous Victorian Planning Minister Matthew Guy issued a blanket exemption from State Land Tax for all land within Melbourne’s Urban Growth Boundary, even ‘shovel ready’ land in completed Precinct Structure Zones.

The huge economic burden is borne by citizens of modest means who are obliged to take on a greater proportion of mortgage debt for fringe land that should be dirt-cheap.

Families with children are Melbourne’s biggest demographic. They require inexpensive well-facilitated family housing, not high-density apartment blocks with thousands upon thousands of SVs.

Needless to say, with a broad based land value tax, holding land off market would be unprofitable. Land hoarding would be discouraged, and there would be little advantage in land-banking large volumes in advance of development.

It also recommends fundamental reform of the housing/taxation system to help free-up supply and reduce incentives to speculate:

Current property taxes discourage investment into new housing, inflate the cost of land, stagnate housing turnover and hinder putting property to its highest and best use.

The report advocates that profound inefficiencies could be significantly alleviated if current transaction taxes were phased out and replaced with a holding tax levied on the unimproved value of land, alongside enhanced infrastructure financing methods for new developments.

The Speculative Vacancies report can be downloaded from the Prosper website. It is well worth reading.