Simon Cowan from the Centre for Independent Studies (CIS) has released a well-argued piece today in Business Spectator backing the Productivity Commission’s call for the family home to be included in the assets test for the Aged Pension in the interests of equity and Budget sustainability:

A properly functioning retirement system enables retirees to use their assets to have a decent standard of living in retirement, with the pension there as a safety net for those who can’t support themselves. Exempting the family home from the pension means test undermines the whole system…

Typically, those on the full rate of the age pension who own their home have more than $400,000 in additional net worth over those who receive a similar pension but don’t own their home. This is a clear equity issue; we should be providing the most assistance to those who need it most.

It is not only unfair to non-homeowners, it is also unfair to taxpayers.

It is particularly galling for young people — who already feel locked out of the housing market… to be asked to fund welfare for pensioners refusing to touch the $700bn they have in housing wealth.

…including the family home in the assets test, boosting the take-up of reverse mortgages through a government backed-product, and deeming that income under the pension income test could save taxpayers $14.5 billion a year and boost incomes for 98 per cent of pensioners by an average of just under $6000 per annum.

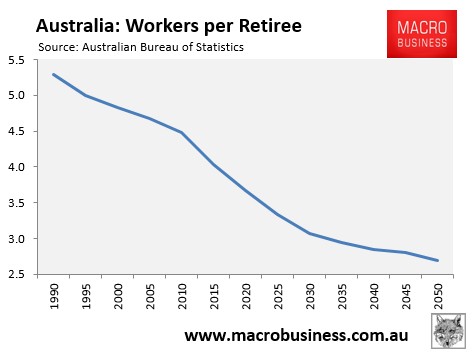

For mine, the CIS’ reasoning is impeccable. With the ratio of workers supporting retirees set to decline for decades, reforming the Aged Pension system will become inevitable, so better to achieve reform by targeting cuts at wealthier pensioners while helping the poorer ones.

Indeed, just to show how out-of-whack the Aged Pension has become, analysis released earlier this year by the National Centre of Social and Economic Modelling (NATSEM) showed that around 260,000 Australian households have a net worth of more than $3m and yet are enjoying welfare payments of about $800 million a year:

Within the group of Australian households worth more than $3m, those of pension age are receiving about $3700 a year in cash payments, NATSEM found…

This shows starkly the ease with which retirees can qualify for the Age Pension — the federal government’s biggest and among the fastest-growing expense…

Ben Phillips, a principal researcher at NATSEM, confirmed the main cash payment going to high-wealth retiree households was the Age Pension..

As I noted earlier this week, around 80% of retired Australians own their homes of which $926 billion in equity is locked up. Meanwhile, the Aged Pension (currently $43 billion per year) is the largest and one of the fastest-growing Budget expenses. This makes reform an absolute priority. My solution is:

- For one’s principal place of residence to be included in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Replacing stamp duties for everyone with a broad-based land values tax.

- Extend the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HECS-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under this plan, house-rich pensioners could continue to receive an income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers. The stamp duty to land tax switch would also deliver more efficient use of the housing stock.

While the economics is simple, unfortunately the political economy is not. Watch retirees fight like wounded bulls against reform, just like National Seniors chief executive, Michael O’Neill, did earlier this week:

National Seniors chief executive Michael O’Neill said he did not believe either the current government or the opposition would favour the suggestion of including the family home in the pension assets test…

“The family home is sacrosanct. It very much defines who we are and what we aspire to as a nation”…

“Australians would fiercely resist any government that forced them to take up reverse mortgages in retirement,” he said.

The sub-text of which is: young people should bear the full burden of balancing the Budget.

unconventionaleconomist@hotmail.com