Readers will know that the current MB base case for global markets is a grind towards a cycle ending crisis of some sort in commodity producer and emerging markets (EM) debt that accelerates the supply side shakeout in global excess supply.

The drivers of this are a healing US economy, tightening monetary policy and a US dollar bull market, as well as the Chinese structural adjustment to lower and less commodity intensive growth. But the crisis is not their’s. The rubber hits the road in EMs (like Australia) that are dependent upon both commodity exports and external US dollar funding.

Goldman today takes a look at who is at risk in the EM universe:

Advertisement

EM FX has been under pressure in 2015. For example, both the ZAR and the TRY have depreciated by 22% against the Dollar year-to-date.

This is not all bad news…but from a sovereign balance sheet perspective (i.e., credit risk perspective), this development is a concern as many emerging economies have issued significant amounts of foreign currency denominated debt (the ‘original sin’) which rises in local currency terms when FX depreciates.

Many emerging economies issue debt in foreign currency (the ‘original sin’) to reduce interest rate payments or because the market will not fund them in their own currency. This makes the country’s debt dynamics vulnerable to sharp currency movements and, as a result, incentivizes the local central bank to hold FX reserves. Exhibit 3 illustrates the level of external debt across EMs, divided into FX and local currency.

The large amounts of FX denominated debt, combined with the sharp FX movements, are a dangerous cocktail from a credit perspective. For example, a 10% TRY depreciation against the dollar will lead to a 3.5pp of GDP rise in Turkey’s external debt level (10% x 35% of GDP), all else being equal. Therefore, at first glance, it is no surprise that EM sovereign credit sold off in sync with EM FX over the summer.

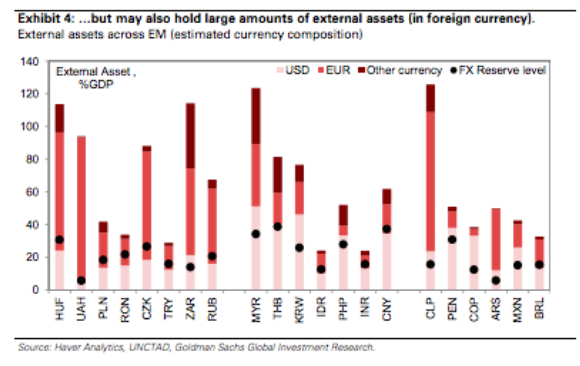

But one also needs to assess the impact on external assets (e.g., FX reserves) when evaluating the credit implications of the sharp FX re-pricing. The asset side of the emerging markets net international investment position (NIIP) is illustrated in Exhibit 4.

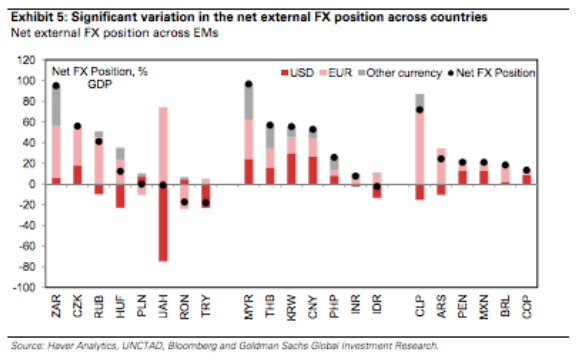

Exhibit 5 illustrates the net external FX position (i.e., external assets minus FX dominated debt), divided into a USD, EUR and ‘other’ component. Within the CEEMEA region, Romania and Turkey are most vulnerable to generic currency weakness, as their net FX position is negative (in sharp contrast to Russia and especially South Africa).

In short, Russia, Turkey, much of Eastern Europe are in jeopardy, parts of South East Asia and Latin America as well. But this analysis is a little misleading. Most of the liabilities are held in the private sector of these nations whereas some smaller portion of the assets is held in the public as FX reserves. This poses something of a maturity mismatch. The reserves can help prevent the currency from falling for a while but if the longer cycle has turned hostile to them (as it has) then the reserves will continue to bleed lower defending the currency until such a time that markets take fright anyway. At that point, the sovereign balance sheet is left with short duration debt matched against illiquid assets (which is why the forex reserve is there in the first place) and trouble is upon them.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.