Readers will recall that the ongoing MB thesis for the trajectory of the global economy is that a healing US economy, tightening monetary policy and a US dollar bull market, combined the Chinese structural adjustment to lower and less commodity intensive growth, as well as financial market destocking of commodities, will drive prices of same to undreamed of lows. Moreover, that that process will culminate in a cycle ending crisis of some sort in commodity producer and emerging market debt that will accelerate the supply side shakeout in global excess supply.

We do not particularly foresee a Chinese “hard landing” as a necessary precondition of this. Indeed, all China has to do is successfully rebalance away from its “old economy” towards consumer-led growth and it will happen anyway. That’s how great is the supply imbalance.

Usefully, today Barclays assesses where global asset classes are pricing versus its own model of a slowing China:

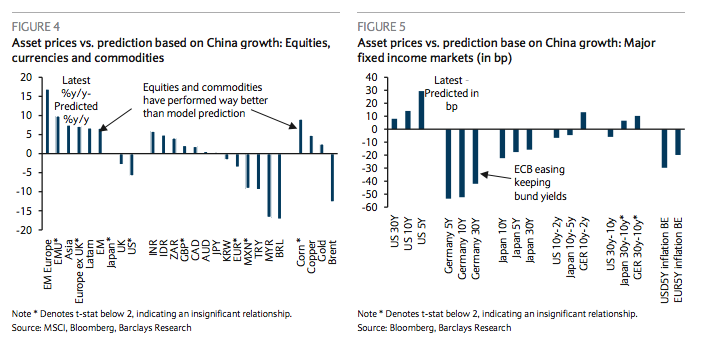

The underperformance of China-sensitive assets raises the question of whether they are already pricing in weaker activity. We compare asset performance over the last year to that implied by slower China growth and the controls; these residuals help us assess whether China-linked assets are reflecting the weaker growth backdrop. We complement this analysis with various valuation frameworks that help us gauge what may be priced into assets, given the risks to Chinese growth. Our analysis shows that EM equities and some commodity price residuals are currently very positive, suggesting the slowing in Chinese activity over the past year is not fully priced (Figure 4). Within equities, EM countries are most expensive relative to the Chinese cycle. The residuals for some of the usual beneficiaries of China’s growth, such as LatAm, Korea and Chinese equities, are very positive, suggesting the bounce in these assets following the August sell-off was overdone. In FX, the most interesting finding is that most Chinasensitive currencies appear cheap, especially commodity currencies and high beta EM. Notably cheap currencies are those of oil producers (the RUB, MYR and COP). The BRL and TRY are examples of currencies that are weak due to domestic issues. The high-beta IDR bounced back strongly at the beginning of Q4 and now looks expensive. The INR also has a positive residual because of idiosyncratic factors. In commodities, Brent looks cheap to the China cycle, while gold and copper are expensive.

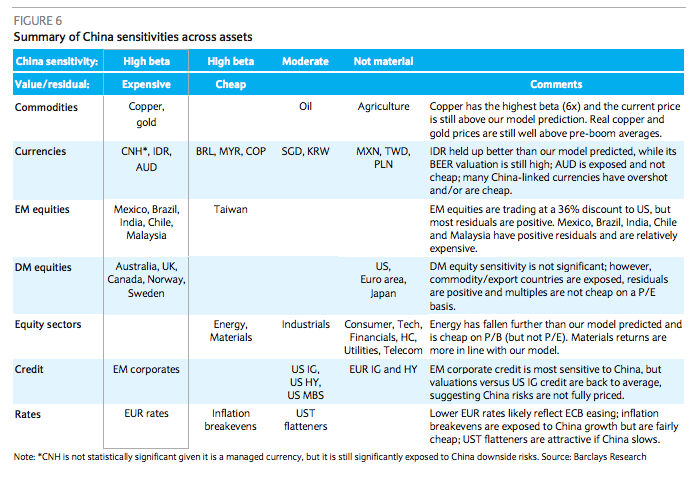

In fixed income markets (Figure 5), US yields are higher and Europe and Japan yields are lower than what Chinese activity, US 2y yields and the VIX would predict. The negative deviation in Europe suggests that ECB easing expectations are the main reason for the gap. Similarly, Japanese yields are also lower than predicted, but to a lesser extent. US 5y yields are higher than predicted, as the Fed is set to hike as other central banks are still easing. While US nominal rates are higher than predicted, inflation expectations are lower, suggesting US real yields are relatively attractive. In credit markets, corporate spreads are in line with predicted, though elevated HY spreads reflect oil exposure. EM corporate and sovereign spreads are in line with our model results. Residuals for US IG spreads are also close to zero. On the other hand, US HY spreads are much higher relative to the model predictions, likely reflecting oil and commodity exposure. Finally, US MBS spreads are slightly tighter than predicted.

We analyze the sensitivities for over 100 assets and present a summary of our findings in Figure 6. Many China-sensitive assets are vulnerable to renewed losses, as they have performed better than our model predictions. These include copper, gold, EM equities (local terms), IDR and EM corporate credit. Such assets are not necessarily cheap, either, and in some cases are still expensive based on various valuation measures. Real copper and gold prices are still well above pre-super cycle averages, and many China-sensitive currencies are still over- or fairly valued (CNY, AUD, NZD, SGD, RUB, etc).

EM equity valuations are relatively cheap, but the headwind from slower China growth is notable and EM FX is still an overhang. EM corporate credit versus US IG relative spreads are back to average levels, suggesting China risks are not fully priced. However, a number of high yielding EM currencies have already been hard hit and valuations are already cheap for idiosyncratic reasons (BRL, MYR, COP, ZAR). DM equities and credit are less sensitive to China, but we find that energy and materials credit spreads have risen by much more than earnings yields.

Advertisement

In short, in no way are global assets yet priced for a mining GFC. Not in equity, debt or FX, especially in Australia.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.