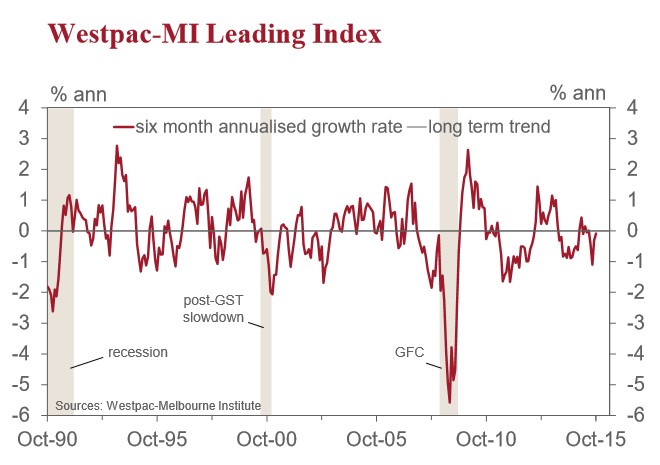

The Westpac-Melbourne Institute today released its Leading Index for October, which indicates the likely pace of economic activity three to nine months into the future.

The Index increased from minus 0.30% in September to minus 0.08% in October, with growth in the index running below trend for the last six months.

But don’t worry, Bill Evans spots a recovery:

While the growth rate in the Leading Index remains below trend there has been some steady improvement in the last two months from the biggest negative deviation from trend in 3½ years that we saw in August to only slightly below trend in October. This print Index is signalling the likely growth pace over the January to October period in 2016. With trend growth in the economy now assessed at around 2.75% today’s read is broadly consistent with growth over that period running at about a 2.75% pace.

That pace is consistent with Westpac’s forecasts of a growth rate of 2.8% through 2016. If achieved, that growth rate will represent a marked improvement on the 2.3% we expect for 2015.

A critical source of that improvement is expected to come from a lift in household expenditure growth from the 2.2% we expect for 2015 to 3.2% for 2016. To achieve that lift in household expenditure we will need to see a lift in nominal income growth and a further moderation in the savings rate. Critical to that lift in nominal income growth will be a more stable year for Australia’s terms of trade compared to 2014 and 2015 which have registered falls of around 10% a year.

The second key boost should come from net exports. In 2015 we expect that net exports will add 1.0 percentage point to GDP growth whereas in 2016 we are anticipating a lift of around 1.3 percentage points. This improvement will be partly driven by a further contribution to net export growth from services. An important feedback from rising net services exports is through the impact on employment.

Also assisting this more positive growth outlook for 2016 will be a modest improvement in non-mining investment and a smaller drag from mining investment, particularly in the second half of 2016.

Over the last six months the six month annualised growth rate has been fairly steady moving from 0.05% below trend to 0.08% below trend. However, there have been some notable shifts in the index components. This period has seen increased drags on from the ASX 200 (–0.56ppts) and dwelling approvals (–0.26ppts). On the positive side we have seen a reduced drag from commodity prices (the RBA commodity price Index, in AUD terms, effectively adding 0.34ppts to the growth rate), US industrial production (0.24ppts); and improved positive momentum in the labour market including aggregate monthly hours worked (+0.16ppts) and the Westpac-MI Unemployment Expectations Index (+0.04 ppts). There have been only minor adjustments coming from the other components of the Index: the Westpac-MI Consumer Expectations Index and the yield spread.

The Reserve Bank Board next meets on December 1. Some weeks ago market pricing was close to a 100% probability of an RBA rate cut by December. With no move in November and the Bank indicating that prospects for a strengthening economic environment had improved a little there is virtually no chance of a move in December. Westpac has consistently held the view that rates would remain on hold throughout the second half of 2015 and over the course of 2016. Discouraged markets which had been expecting at least two cuts by mid-2016 have now backed away giving around a 50–50 chance of one cut by mid next year. This pricing looks more realistic with the risks to rates remaining to the downside.

With the triple shocks of falling mining investment, falling housing (both and construction and prices), and the car industry’s closure very likely to hit the economy in tandem in 2016-17, Westpac’s forecast of an improving domestic economy look badly mistaken.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.