From Society Generale:

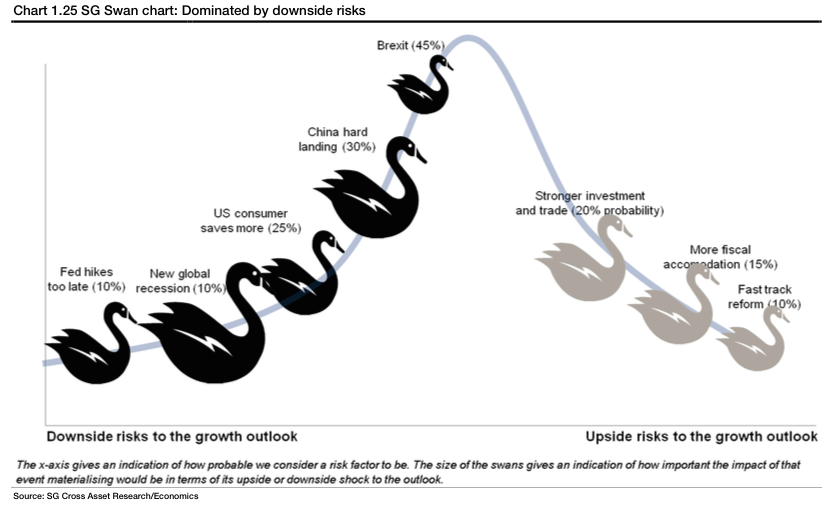

Brexit at a probability of 45%, remains our highest probability risk. At this time, a date has yet to be set for the referendum but 3Q16 seems a likely timing, based on the idea that Prime Minister Cameron will want to hold the referendum within a reasonable timeframe on concluding an agreement with his EU partners (which could come as early as the December 2015 Summit, but more likely in March 2016).

China hard landing remains a significant risk at 30%. Medium-term, we set an even higher probability of 40% on a lost decade scenario. As opposed to a hard landing, however, such a risk scenario would manifest itself only gradually. The most likely trigger for a China hard- landing is policy error with miscalculation of how much financial risk management or structural reform the system can absorb. We identify three main triggers. In practice, a combination thereof seems the most likely cause of such a risk scenario.

- Credit crunch: An intensification of capital outflows, a growing number of non-performing loans and an insufficient response from the PBoC could result in a credit crunch. Such risks could be further exacerbated by pressure coming from Chinese corporations’ foreign exchange denominated debt and overall high level of leverage.

- Dry-up in housing demand: Should a new housing shock emerge, triggering a buyers strike, then real estate developers (also burdened with foreign currency loans) could suffer renewed stress, triggering a significant scaling back of investment.

- Capacity overhang: The still-large excess capacity in the manufacturing sector would be further exacerbated in such a scenario, weighing on corporate margins and profits. The risk is to see bankruptcies and unemployment increase in such a bleak scenario.

China hard landing and/or a renewed EM crisis are both potential triggers for a shock that could trigger global recession (10% probability).

Consumers hold the key to recovery in the advanced economies. We place a 25% probability on the risk that consumers in the advanced economies save more of the gains in real disposable income than we expect.

Not my choices. I see the big risk factors as:

- a much deeper commodity crash and emerging market debt crisis as China continues to slow, the yuan to fall and the US dollar to rise;

- growing European right wing political influence fatally undermining the euro, tipping into the above, and

- global recession, that is below 2% growth, including a global equities bear market.

The base case is probably still for these things to transpire in 2017 but acceleration is very possible.

There is always the chance that the US consumer parties like its 2006 but I doubt it!