Hot on the heels of the Australian Prudential Regulatory Authority’s (APRA) admission that it acted too late on dodgy lending, the Reserve Bank of Australia’s (RBA) deputy governor, Philip Lowe, has admitted that the level of investor participation in the housing market has been greater than it first thought:

As lenders have looked more closely, what they have found has surprised and, to some extent, concerned us.

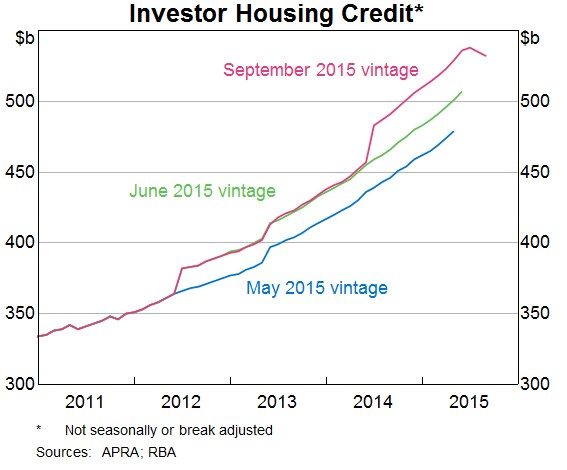

The first is that over the past six months there have been very large upward revisions to the value of investor loans outstanding, with offsetting downward revisions to owner-occupier loans. Material revisions have been made by more than 10 institutions, including two of the largest lenders. The scale of these revisions can be seen in Graph 1, which shows the stock of investor credit outstanding as reported in each of May, June and September this year. The cumulative effect of the upward revisions has been to increase the stock of investor credit outstanding by around $50 billion, or 10 per cent. According to these new data, investor loans now account for 40 per cent of total housing loans outstanding, not the 35 per cent reported earlier in the year.

While the reasons for some of these earlier errors have been identified, in other cases the reasons are unclear and lenders have not been able to provide comprehensive back data. As a result, when calculating growth rates for investor and owner-occupier credit, the RBA has had to make adjustments for what are effectively breaks in the series…

The second data issue has emerged over the past couple of months and has worked in the other direction, with lenders reporting that some loans that were previously recorded as investor loans were really loans to owner-occupiers…

These various data problems have reinforced our view that the supervisory focus on investor lending has been entirely appropriate. And it is disappointing that some lenders’ internal systems have not been up to the task of reporting accurate data on the split between investor and owner-occupied housing loans.

This issue was discussed at the most recent meeting of the Council of Financial Regulators, with Council members considering what steps could be taken to improve the quality of data. Among other things, it has been decided that APRA, the RBA and the Australian Bureau of Statistics will, next year, undertake a thorough review of the data collected from authorised deposit-taking institutions regarding their domestic books.

Unbelievable. For nearly four years, this site and others called for macro-prudential controls to prevent high risk mortgage lending, only to then face stiff resistance and ridicule from Australia’s policy makers, including from both the RBA and APRA.

Now both institutions have belatedly acted to reign-in speculative investor lending long after the horse has already bolted.

Advertisement

Robust prudential supervision necessarily involves preventative policies, not the types of reactive policies we are experiencing currently, which are inherently pro-cyclical and risk exacerbating the downside as the Great Australian Housing Bubble bursts.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.