Following yesterday’s explosive report by Bob Birrell and David McCloskey from the Australian Population Research Institute, which projected that there will be an increasing scarcity of family-friendly housing in both Melbourne and Sydney, thereby having deleterious impacts on younger Australians wishing to start a family, several of Australia’s think tanks have proposed sensible reforms to Australia’s tax and welfare system to encourage empty nesters to downsize. From The Canberra Times:

Simon Cowan, from the Centre for Independent Studies, says including the family home in the pension assets test would be a good way to encourage older Australians to downsize.

“At the moment, you have a disincentive to downsize because it can lead to a reduction in pension income and, when you add in the cost of stamp duty and the cost of moving, the amount of capital you release from downsizing is not that high.”

Grattan Institute director John Daley said another way to encourage downsizing would be to significantly reduce or abolish stamp duties, and replace them with property levies instead.

“That way you would be charged more for living in a house and less for selling it,” Mr Daley said.

“At the moment we’ve got the incentives in completely the wrong direction. You’re paying the stamp duty when you sell the house, but you don’t pay much for living in it. We need to flip that around so you don’t pay a penalty for selling your house but you do pay extra for living in something bigger than you really need.”

Both think tanks have made eminently sensible suggestions.

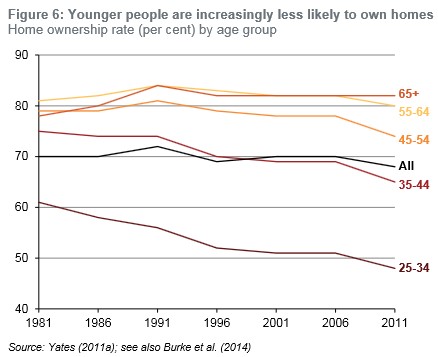

As argued yesterday, it is the height of unfairness that the biggest asset most households retiree with – their principal place of residence – is essentially excluded from their capacity to fund their own retirement. It is also especially unfair to expect younger generations – who are either struggling under the weight of the high mortgage debt legacy they inherited or unable to afford a home altogether (see below chart) – to bare the full cost of their parents’ and grandparents’ retirement while they live in homes they themselves cannot afford.

Including the family home in the pension assets test would greatly improve intergenerational equity as it would remove the requirement for the younger generations to subsidise oldies with significant assets. It would also encourage empty nesters to downsize to smaller accommodation, thus freeing-up larger family-friendly homes for young families.

As argued by The Australian Institute, extending the Pension Loans Scheme to everybody of pension age would also facilitate reform.

The Pension Loans Scheme is a state-run reverse mortgage scheme that allows eligible retirees to borrow against their homes to receive payments from the government equivalent to the full Aged Pension.

The interest rate through the Pension Loans Scheme is only around 5%, repayable upon their estate or sale. Therefore, home-owning retirees that no longer qualify for the Aged Pension could continue to receive income payments whilst living in their homes. For all intents and purposes, they would experience no change in their living standards, but with far less drain on the Budget and, by extension, younger Australians.

The important thing is to get rid of the incentive to shelter assets in housing to avoid the pension assets test. With housing included in the assets test, there would be better incentives to move to homes that better suit retirees’ needs. Many may choose to stay put, but they would lose access to the Aged Pension, thus forcing them to rely on the Pension Loans Scheme instead for income.

Replacing stamp duties with a broad-based property tax also makes good sense. In addition to vastly improving tax efficiency, such a tax shift would also encourage households to move to homes that best suit their needs by removing the punitive tax on moving (stamp duty), encouraging the highest value use of land, and penalising land banking and vagrancy.

That said, the scarcity of family-friendly homes has not just been caused by hording from empty nesters, although it is a major cause. Australia’s excessive immigration intake, half of which has flowed to Sydney and Melbourne, has also greatly increased demand and competition for dwellings, thereby creating severe housing indigestion and congestion, and lowering the living standards of pre-existing residents (especially the younger generations).

Any policy response should therefore, also seek to curb immigration

At the same time, artificial constraints on fringe land supply must also be abolished, along with better provision and funding of housing-related infrastructure, and replacing the “first-user-pays-all” tax on new housing with long-term bond financing recovered through rate payers over time.

If the Government is going to persist with a high immigration intake, the least it can do is facilitate this growth via an adequate release of new land and the provision of housing-related infrastructure, as it did for prior generations (e.g. the baby boomers).

Unfortunately, the prospects for a meaningful discussion have dampened somewhat with the lobby groups for older Australians howling in protest at the thought of being encouraged out of their large family-friendly homes:

National Seniors Australia chief executive Michael O’Neill said the idea that older people should move out of their own homes was “offensive”.

He said people who had bought their homes decades ago – often in what were in humble areas – and had since worked, saved and paid 18 per cent interest rates in the 1980s to own their homes…

Council on the Ageing chief executive Ian Yates agreed there were “good reasons” for people staying in their homes… Along with stamp duty, asset-rich, income-poor older people risked taking a hit to their pension if they sold the family home and were left with more cash, which would be taken into account in assessments for pension eligibility.

Mr Yates – who described any pressure on older people to move as “ludicrous”… he cautioned policy makers and planners to think more imaginatively about how to create space for young families, noting that in many European cities, for example, children are raised in apartments and then taken to parks to play.

What is “offensive” and “ludicrous” is that the wealthiest generation in history expects today’s children to be raised in apartments while they occupy empty large homes, all while they continue to be supported via the Aged Pension.

What these senior’s groups are effectively telling the younger generations is not to expect the same opportunities in housing as they enjoyed, but to continue providing them with welfare while they live in homes they will never afford.

Now that’s what I call a sense of entitlement.