The Australian press is falling over itself to defend doomed miners. From Bartho:

A price below $US40 a tonne isn’t inconceivable – it would represent a return to the long-term trends that long-established producers like Rio and BHP used to predicate their investment on. At those levels, only Rio and BHP would generate meaningful profits – but those profits would still be high-margin and would still be very meaningful.

That’s why it would be in their interests for the price to fall, in the short term, to whatever level is necessary to drive out excess and higher-cost supply and re-balance the market.

In the recent past the obvious casualty of the kind of disruption an iron price in the low $US40s a tonne or less would generate would have been Fortescue. It has, however, done a remarkable job on its costs and is steadily strengthening its still-leveraged balance sheet.

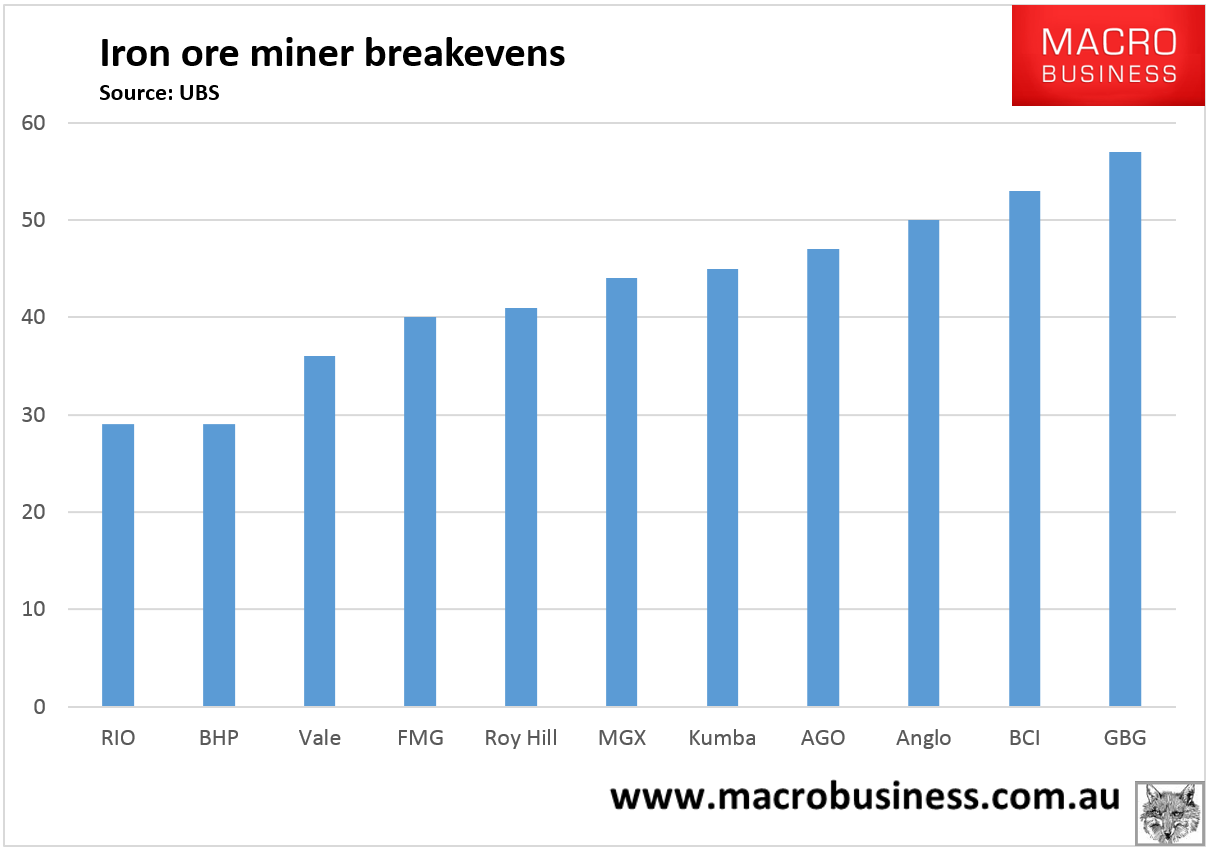

There is a sophisticated view in the market that the price will settle in the long term at the marginal cost of production for the highest-cost of the major low-cost producers – Rio, BHP, Vale and Fortescue.

Where that role would almost automatically have been assumed to devolve to Fortescue until relatively recently, there is now an effective contest between Fortescue and Vale for the less-than-desirable role as the marginal (and marginally profitable) producer.

Vale’s overly leveraged balance sheet – and the uncertain but obviously very large cost of the liabilities associated with the Samarco tailings dam disaster that it will share with BHP – is going to create financial stresses at the current prices for iron ore and the other base metals and energy commodities it produces.

Poppycock! BHP and RIO shareholders are being destroyed just as certainly as everyone else. The market share battle was never planned for, it is simply what is required now that everyone so horribly mistook the the cycle. Sub-$20 is very possible not sub-$40.

As for FMG vs Vale, it’s a no contest:

Moreover, S11D will get Vale below $30 by my numbers while FMG is scraping the bottom of its barrel already. Both have lousy balance sheets but Vale is a former government owned colossus and you can be quite certain that if there is any trouble then its status as national champion will see it given some preferential treatment. For now at least it is Fortescue and Roy Hill that are fighting it out for emerging marginal producer (then it will be Vale!).

Bartho’s jibber jabber is matched by similarly limited pieces at Dumbfax:

Fortescue Metals Group has serviced $US750 million of its $US8.81 billion gross debt, pushing its repayments during the past four months past $US1 billion.

…”Moving forward we remain committed to utilising our accumulated cash balances for further debt reduction,” he said.

“We targeted those two that are sub-par at the moment and that gives us the best bang for our buck in the current marketplace,” he said last week.

…”It could be general market views, it could be balancing their own book, it could be a lot of reasons why they would buy and sell a debt piece just like an equity piece,” he said.

“It could be around views on China, iron ore or whatever.”

Or it could be that you’re stuffed and the bond market knows it. Tess Ingram is still mining her recent junket too:

“The ability of those smaller guys to pull costs out and stay alive, that’s really going to prolong how long these [low] prices last for,” he said.

“There is no good news in that. Production has to go away to balance the market because we don’t see increasing demand.

“We are going to be in this cost curve-limited world for a long time and however low the cost curve goes, that’s where the price is going to go. It is delaying the inevitable.”

…Fortescue chairman Andrew Forrest told the company’s annual meeting earlier this month that prices were likely to head in to the $US40s per tonne, but that Fortescue could withstand this after reducing its C1 costs to $US16.90 a tonne from $US32 a tonne 12 months ago.

The larger Pilbara producer is targeting C1 costs of $US15 a tonne by the end of this financial year, with its confidence buoyed by the better than expected performance of its wet ore processing facilities and the impact that has had on its mining costs.

It won’t help, alas, though at least we got some fair dinkum quotes this time.

Finally we come to the BHP dividend, which has been mercilessly sold by the media as the be-all and end-all of mining investment, but no longer, from the AFR:

Former BHP chairman Don Argus, who introduced the policy of never cutting its $US6.6 billion dividend, says it wasn’t designed to be a permanent strategy.

Mr Argus introduced the so-called progressive dividend policy when BHP merged with Billiton in 2001. He told The Australian Financial Review that it wasn’t meant to be a long-term policy for use of the company’s cash, which is under pressure from plunging commodity prices.

“It was never meant to be a forever thing, it was not meant to be written in stone,” he said.

The comments are likely to provide ammunition to a growing chorus of investors who say the policy could weaken BHP’s balance sheet and threaten its credit rating at a time when its share price is under $20 for the first time in a decade.

You’re being softened up, folks. The dividend is history.