The mining GFC has made it onto the screen of the apologists now and the Madometer has wasted no time in confirming the validity of the thesis:

As the countdown to a US rate hike begins, fears are mounting that capital outflows from emerging markets might intensify, crunching growth and perhaps even sparking some form of debt crisis.

No one should expect these lower inflows to be permanent though. Advanced economy assets — equities, bonds, property, you name it — are already extremely expensive in comparison. Not to forget that China and many other emerging nations have much better debt/deficit metrics than most of the advanced world. In particular, investors won’t overlook the fact that many of the emerging market nations have negligible public and foreign debt, huge foreign exchange reserves and budget balances that many Western nations can only dream about. Otherwise, corporate debt consists primarily of local currency bank loans, with foreign currency bonds constituting only a small proportion of that debt. Even the IMF’s own analysis shows that much of the concern over non-financial corporate debt, especially in China, is wildly exaggerated.

Against that backdrop, the kind of crisis envisaged by some is not very likely.

Yes, emerging markets are better placed that previous cycles. But this is not an ordinary cycle. China is the trigger but not the crisis. It is commodity producing emerging markets that are most in the gun, those nations (and private firms) that have the unfortunate combination of commodity export exposure to a slowing China and external funding exposure to a rising US dollar largely in the corporate sector. If you wish to see what the IMF actually said about that then find it here.

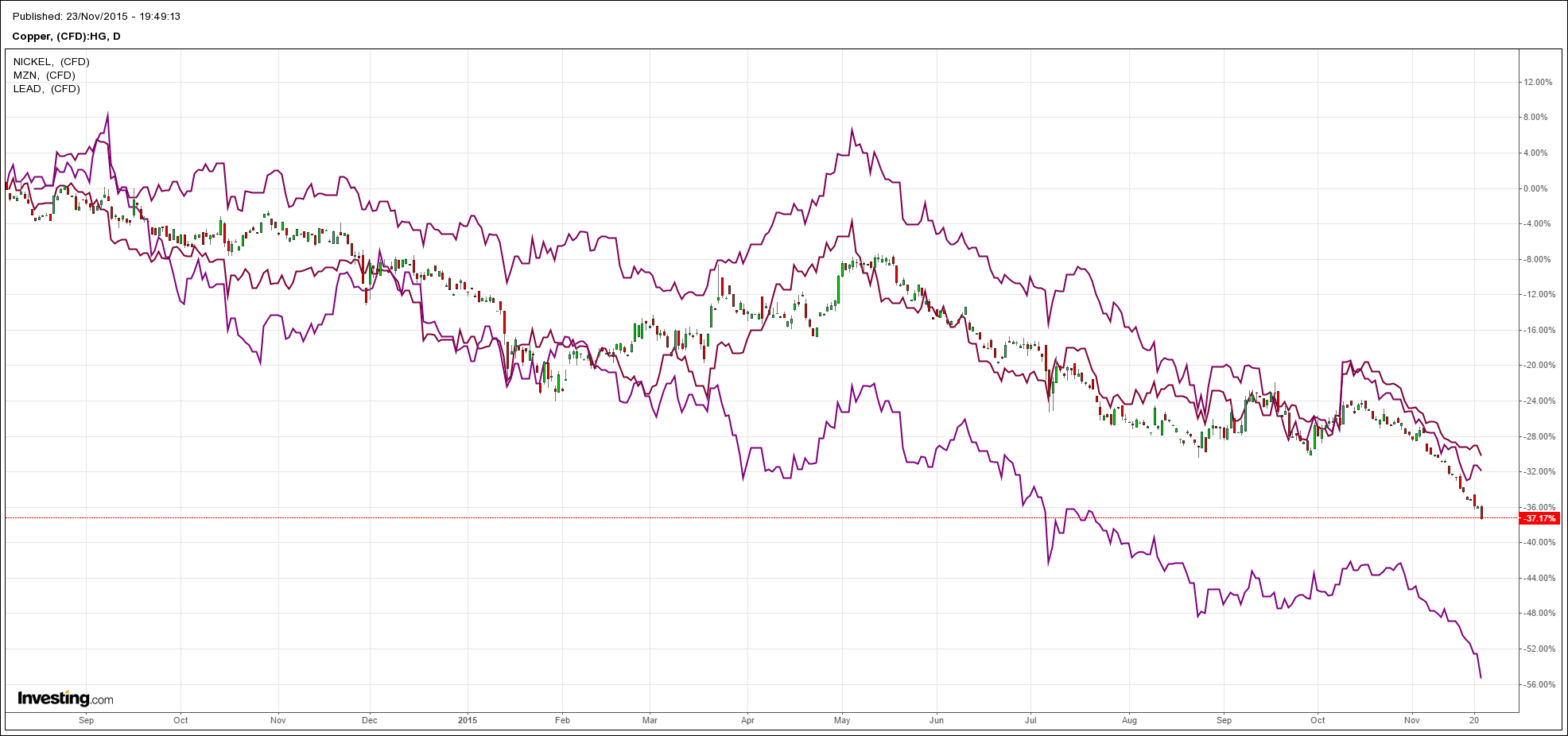

Meanwhile, markets continue to price this very deterioration. Copper fell below $2 briefly and base metals were pounded as nickle (another input into steel) collapsed 5%:

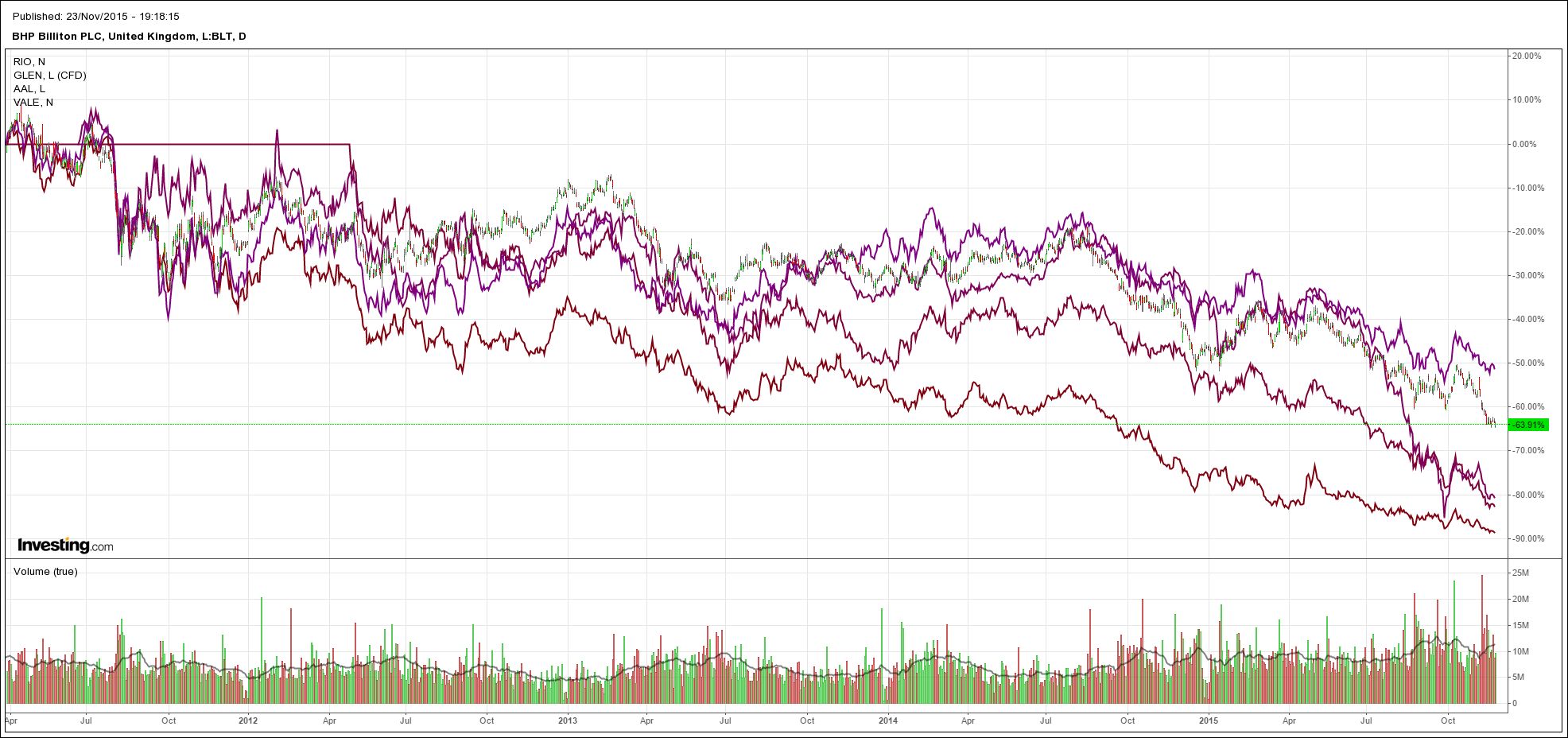

Big miners were hammered again with BHP at new record lows and everyone else nearly there:

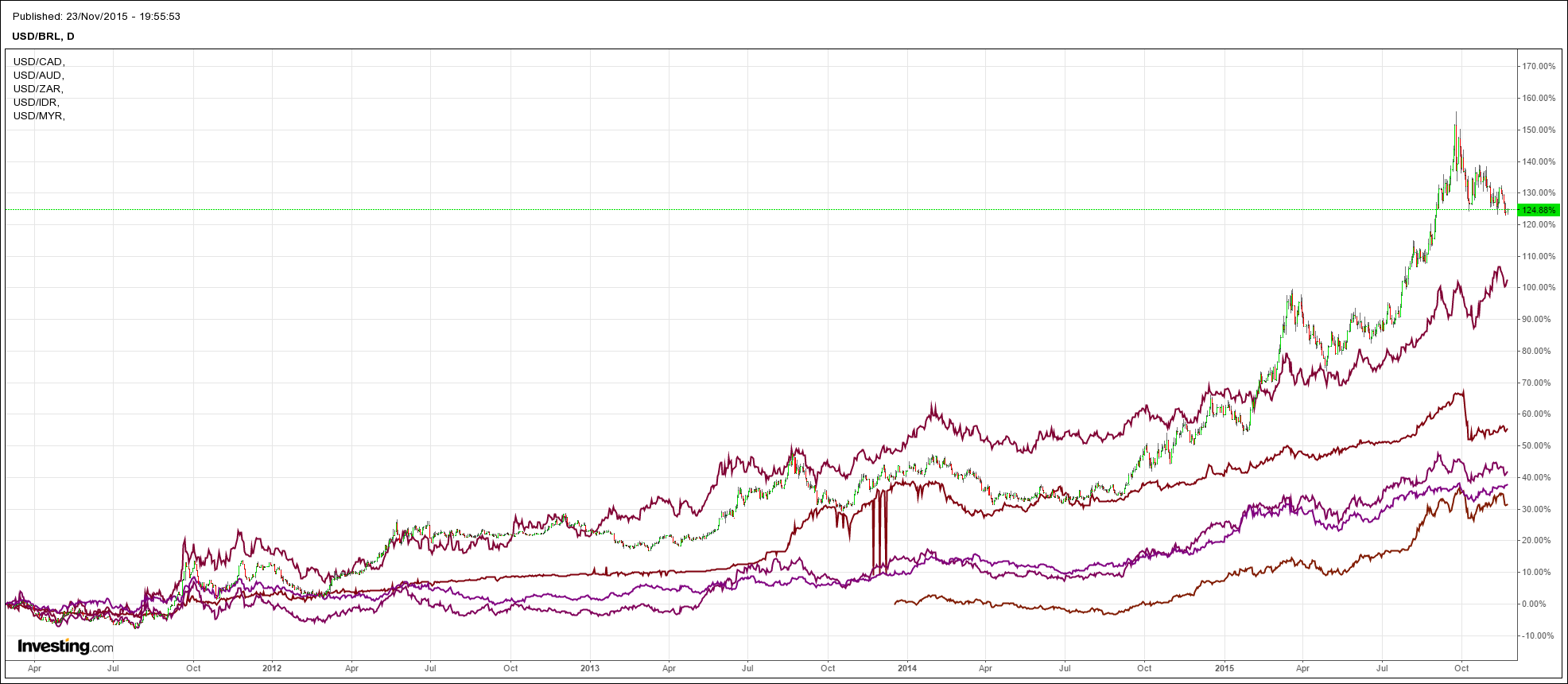

The US dollar index broke 100 briefly and is simmering:

It made ground against all commodity currencies:

High yield debt broke towards 2015 lows but recovered:

And, most disconcertingly, the downgrade cycle has started for commodity traders with S&P putting Noble Group on downgrade watch and sending its cost of funds through the roof (chart is from Zero Hedge):

The CreditWatch action reflects our view that Noble’s liquidity and financial leverage have weakened and breached levels that we consider appropriate for the current rating. However, management’s commitment to raise new capital could support the company’s credit profile.

Noble’s liquidity deteriorated in the third quarter of 2015 following a 27% decline in the company’s net available readily marketable inventory to US$1.48 billion as of September 2015 from US$2.0 billion in June 2015. The deterioration was largely related to the fall in commodities prices. The company’s available and undrawn committed credit lines fell almost 50% during the period to about US$1 billion. The company’s cash sources are less than 1.5x cash uses as of September 2015, below the threshold for a “strong” liquidity assessment.

Noble’s financial leverage is also weak for the rating. The company’s ratio of funds from operations (FFO) to debt is 19.8% as of September 2015 on a rolling 12-month basis. This is a similar level to that in June 2015, but down from 24% in March 2015. In our view, the company’s cash flow and earnings visibility are poor amid a challenging market. We expect that the company will commit to its stated strategy of focusing on profitability, and having prudent working capital management and cost controls to help offset market volatilities.

We believe the Noble management’s commitment to raise at least US$500 million in new capital could help restore the company’s liquidity position and financial leverage, which will be key to maintaining the current rating. In our opinion, if Noble were able to raise at least US$500 million in capital to offset its outstanding debt, the ratio of FFO to debt could improve to about 22%. The company has a good track record of raising capital through recycling assets and attracting new investors, in our opinion.

We aim to resolve the CreditWatch placement in three months. We will review Noble’s liquidity trends and financial leverage to see if the company’s capital-raising and cost-cutting measures are adequate to weather the heightened volatility in the global commodities market.

We may lower the rating by one notch if: (1) Noble’s liquidity does not improve, such that its cash sources are unable to cover uses by at least 1.5x. This could happen if the company is unable to raise sufficient capital per its commitment or its cash generation and working capital controls are weaker than we expect; or (2) Noble’s financial leverage does not improve over the next three months, such that the ratio of FFO to debt remains below 25%. This could happen if the company cannot raise new capital or if its earnings and profitability deteriorate. We could lower the rating by two or more notches if both conditions above are not met within the next three months.

We could also downgrade Noble if the company’s trading risk position weakens. Possible indications of such weakness include increases in fair value relating to long-term commodity offtake contracts, concentration risk of counterparties, or lower cash realization of commodity contracts than the company expects.

We could affirm the rating if we believe the weakening of Noble’s liquidity is temporary and the company has a credible plan and shows strong execution to restore its financial strength. Noble’s ratio of cash sources to cash uses staying above 1.5x and its FFO-to-debt ratio rising above 25% on a sustained basis could indicate such improvement. At the same time, we expect the company to demonstrate continued cash realization of marked-to-market gains and prudent risk management of fair value financial assets, including offtake contracts.

How long before Glencore joins it? How long before the panic of August returns to broader commodity debt markets?