The global steel industry roughly doubled in size from 2000-2014 at a CAGR of 4.8%. For this to transition to an expectation of zero growth was always going to be a shock, but the speed with which the industry hit the buffers over 2015 was certainly more aggressive than previously expected. As we have recently noted, we currently have the wrong type of global economy for metals demand, and this has hit steel worse than others. Global steel consumption looks set to fall 3% this year, only surpassed by 2009 in recent history. And even then, the decline was an exChina story (where demand fell 23.6% YoY) – Chinese demand rose 12% YoY in 2009. This year, both China and ex-China will be negative, highlighting the global nature of the problem. On a regional basis, only India, ASEAN, Africa and Europe have seen apparent consumption growth over 2015.

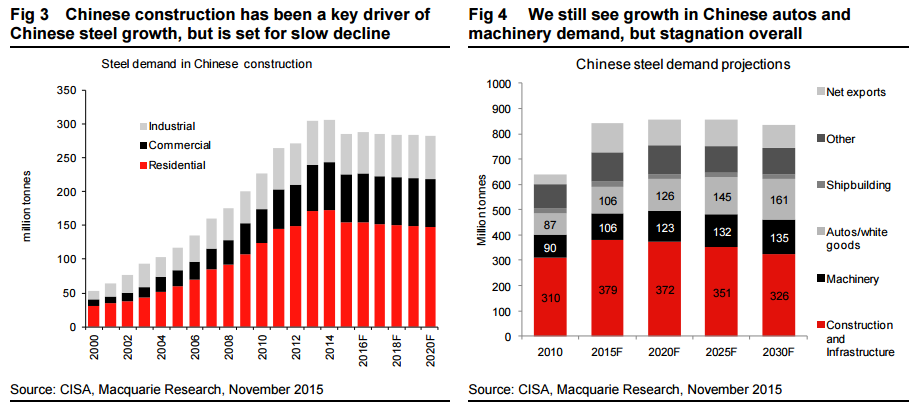

Part of the reason for the rapid demand transition has been one of the key factors which drove growth also went into decline – the Chinese construction market. With new starts suffering, we expect demand for steel in residential Chinese construction will have fallen 10% over this year, and even though sales are recovering we don’t expect aggressive rebounds in demand. In future years autos and machinery offer some offset, but we are now looking at a Chinese steel market in the ‘peaking out’ period, something we discussed further in this Commodities Comment from earlier in 2015.

As a result, for the first time in 20 years, China is not expected to be the key driver of demand growth in the coming five years. While nervous about demand potential in 2016 given the capital flows and currency moves seen this year, we still see some potential for growth in other emerging markets, adding 80mt of demand growth through 2020. However, this takes absolute growth rates back to levels more prevalent in the 1990s – not a great time for global steel. The only people who still seem to think there is significant upside in global steel consumption akin to the past decade are the major iron ore producers – for example BHP’s belief global steel consumption will hit 2.5bn tonnes by 2030 – just a further 50% upside required there!

…So who lives and who dies? This will likely come down to a combination of banks and governments. The former will be under pressure, globally, not to extend lending to the steel industry until the prospects stop declining – something now helped by aggressive and misplaced expectations of recovery in consensus prices. The latter will be under increased pressure to support local jobs in a highly emotive climate – and this will force hard decisions to be made. While the entire world is facing industrial overcapacity in many sectors, we feel that steel is the one where decisions will be forced upon them first, given the scale of the problem.

Exactly right. All I would add is that I expect Chinese construction and steel output to decline a little more swiftly and thus see almost no global demand growth for the next five years.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.