The Grattan Institute has delivered another excellent report entitled Super tax targeting, which argues that the Budget could save a combined $6.6 billion a year by better targeting superannuation contributions (saving $3.9 billion a year), along with implementing a 15% tax on the earnings of retirees (saving $2.7 billion a year).

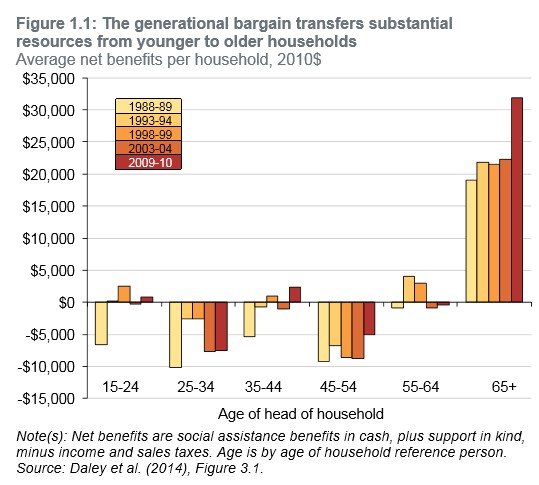

Grattan shows that Australia has a Budget problem brought about mostly by the ageing of the population. Younger generations are being asked to pay more than their fair share, with Commonwealth and state governments combined spending $9,400 more per household aged over 65 in 2010 than they did six years earlier, reflecting increases in the Age Pension and rising health spending per person (see next chart).

Grattan also notes that over the past decade, older households captured most of the growth in Australia’s wealth:

Despite the global financial crisis, households aged between 65 and 74 years today are $400,000 (or 27 per cent) wealthier in real terms than households of that age ten years ago. Meanwhile, the wealth of households aged 25 to 34 years fell by $2,000 (or 4 per cent).

Many older households that could afford to contribute more tax aren’t, in part due to the former Howard Government’s short-sighted decisions to abolish taxes on superannuation withdrawals for over 60s and to increase the effective tax-free threshold to $30,000 for retirees’ earnings outside of superannuation.

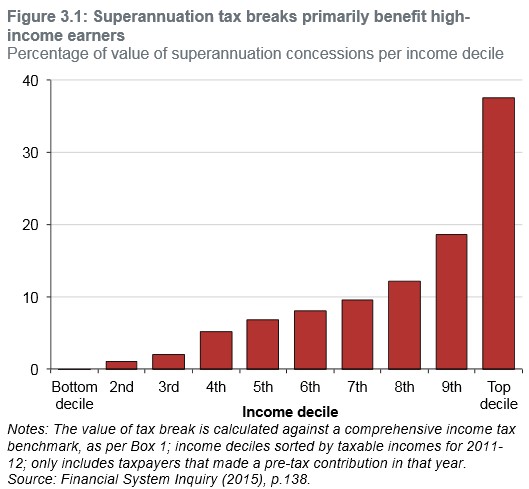

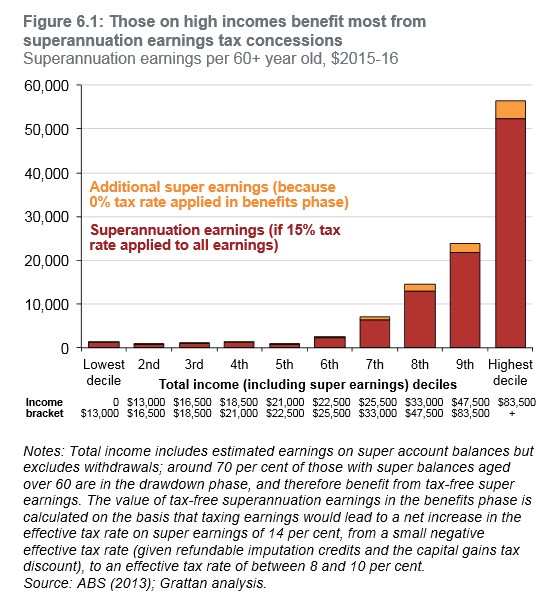

Grattan argues that the current superannuation system is “expensive and unfair”. By value, most superannuation tax breaks go to people on higher incomes, many of whom would never be reliant on the Aged Pension anyway (see next chart).

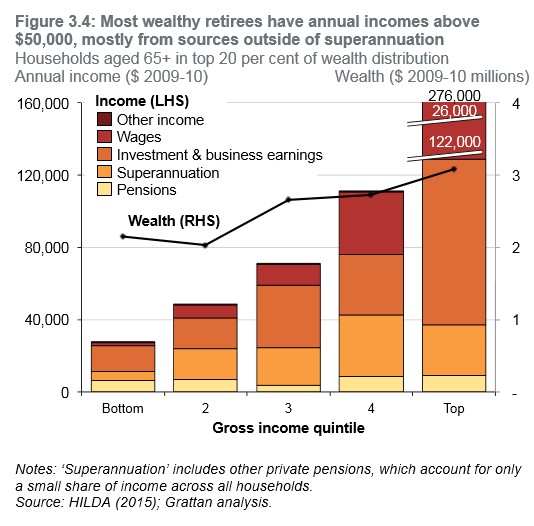

Accordingly, superannuation tax breaks for those on high incomes do not reduce Age Pension costs (see next chart). High-income households are very likely to self-fund their retirement, irrespective of superannuation tax breaks, and consequently they are unlikely to qualify for an Age Pension.

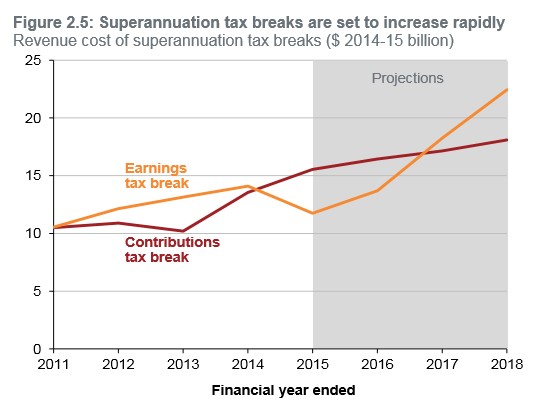

Superannuation concessions are also “the largest and fastest growing leaks from our income tax system, reducing income tax collections by over $25 billion a year” (see next chart).

These costs will increase even more rapidly if the Government raises the superannuation guarantee contribution to 12% without corresponding reform.

Grattan proposes three reforms to better align tax breaks with the goals of superannuation. These reforms could save the Budget $6.6 billion a year according to Grattan’s estimates and would also reduce the transfers between today’s younger taxpayers and older retirees.

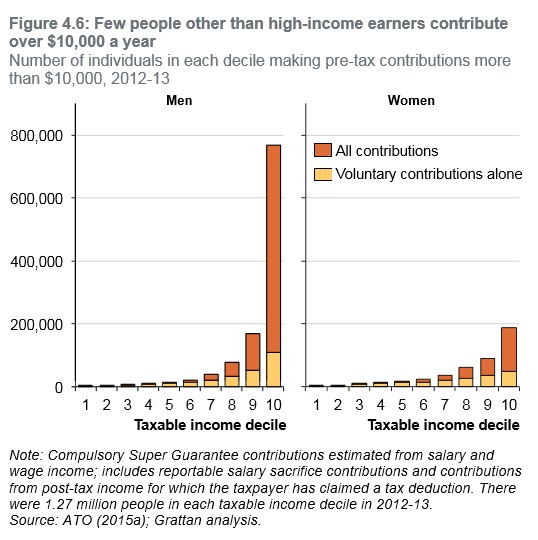

First, Grattan wants to see contributions from pre-tax income limited to $11,000 a year. 80% of contributions above this level come from people likely to retire with enough assets to be ineligible for an Age Pension even without such big super tax breaks (see next chart).

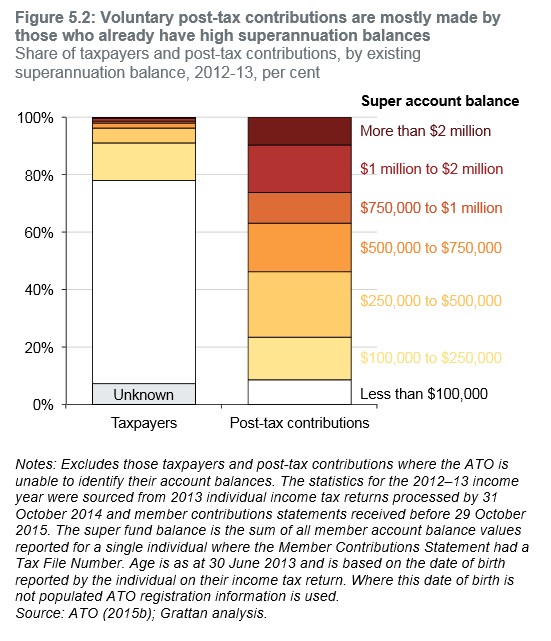

Second, lifetime contributions from post-tax income should be limited to $250,000. In practice, many post-tax super contributions are motivated by tax-planning objectives. They are also mostly made by those who already have high superannuation balances (see next chart).

Finally, earnings in retirement – currently untaxed – should be taxed at 15%, the same as superannuation earnings before retirement. According to Grattan, the wealthiest 10% of retirees pay no tax on their average super earnings of $85,000 a year – a situation that is grossly unfair. It would also simplify the administration of the current system as all accounts would be taxed in the same way, regardless of age.

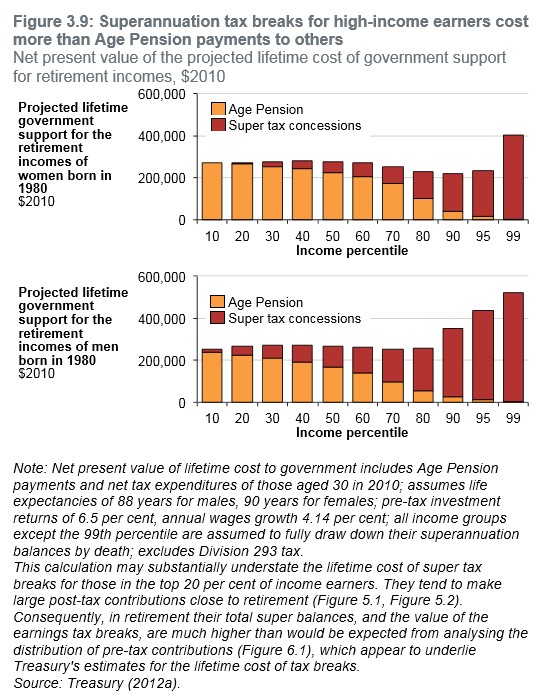

As shown in Figure 2.5 above, the cost to the Budget from superannuation earnings concessions is projected to grow rapidly as super balances rise, and as a greater proportion of the population enters the retirement phase where no tax is paid on earnings. These concessions also overwhelming benefit high income earners (see next chart), and therefore must be reigned-in.

Overall, it is another brilliant report by the Grattan Institute that provides a sensible blueprint for superannuation reform, and would clearly improve both the equity and sustainability of the system.

Let’s hope our federal politicians are paying attention.