From Macquarie Bank’s monthly Chinese steel mill survey:

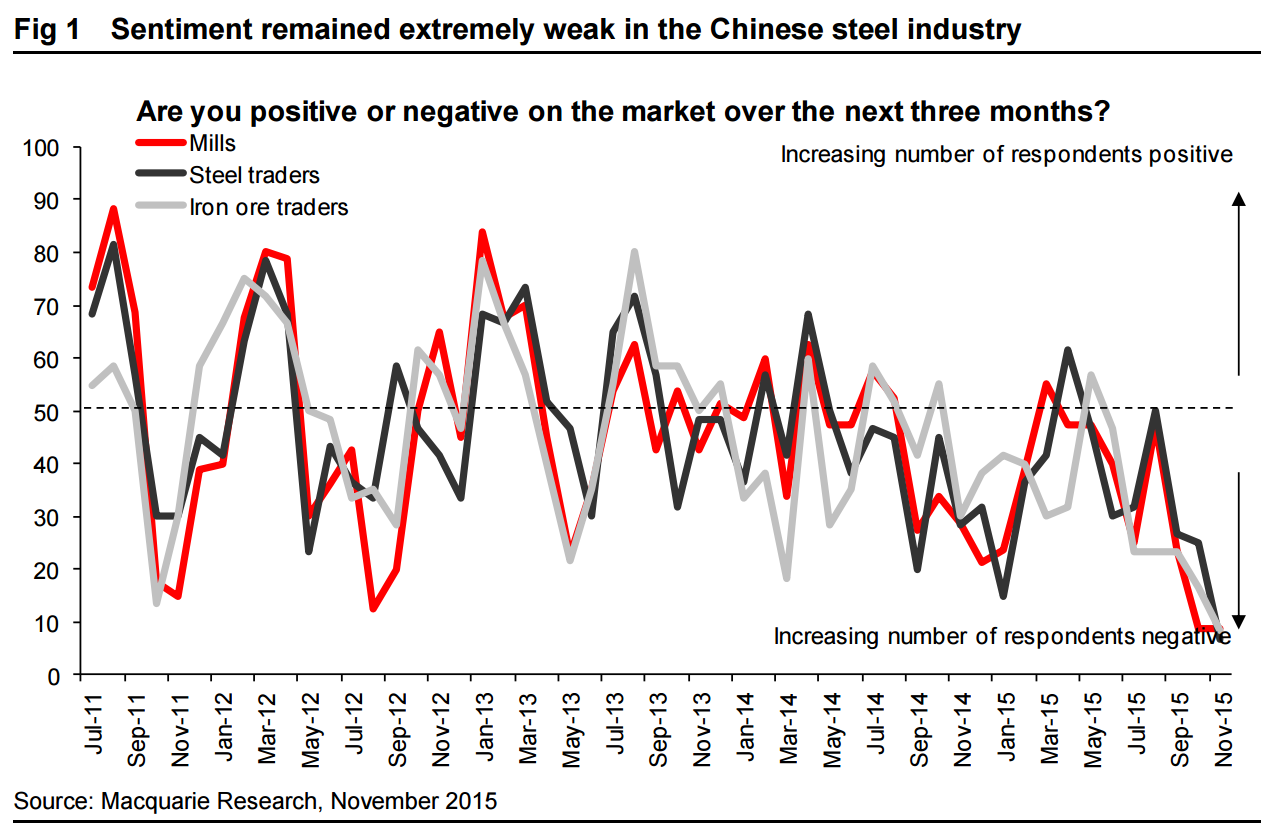

Sentiment remained extremely weak in the steel industry in the first half of November, according to the latest result of our proprietary survey. There was a sharp slump in demand from infrastructure projects, which could be somewhat seasonal, while no other sectors had much improvement and exports slowed down. Although iron ore prices were recently declining, steel mills have barely seen profitability tick up as steel prices dropped rapidly at the same time. It’s thus no surprise that capacity utilisation continued to come down according to our survey, and we would expect more blast furnace closures to take place before year-end, which adds further downward pressure on iron ore prices.

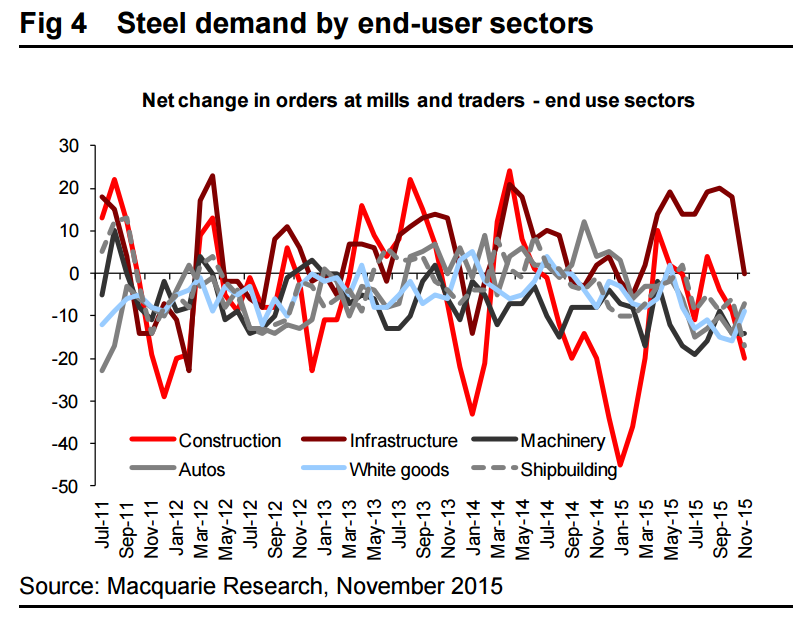

The biggest surprise on the demand side is a sharp fall-off of orders from the infrastructure sector (Fig 4). The declining growth of infrastructure FAI this year (Fig 5) may have contributed, but it should only be a minor factor as the drop of infrastructure orders for steel was quite sudden. The approaching winter may therefore be another reason behind the slump as we have seen similar drops around winter time in previous years. If this is the case, the implication, however, is that demand from infrastructure projects could remain very weak in the next couple of months (particularly in northern China).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.