Here it is from from Macquarie:

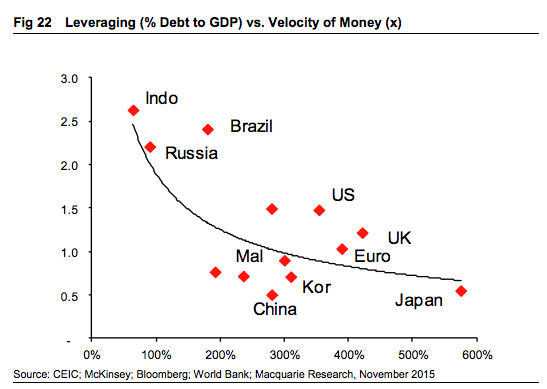

The only area of further leverage is in lower income global categories where both leverage is low and correspondingly velocity of money is high.

Whilst some of these countries are relatively large (such as India and Indonesia), the group (~80 countries) mostly consists of small countries in Africa, Middle East and select few Latin American nations. However by the time we rule-out G4 plus Australia, NZ, Canada and most other European nations as well as China, Korea, Taiwan, Thailand, Malaysia, Brazil, Mexico, South Africa, Russia and Turkey, the rest of the global economy (i.e. low and low middle income categories) represent less than 10% of global demand(vs. ~25% of global GDP commanded by upper middle income grouping, which includes countries like China, Thailand, South Africa, Turkey and Malaysia).

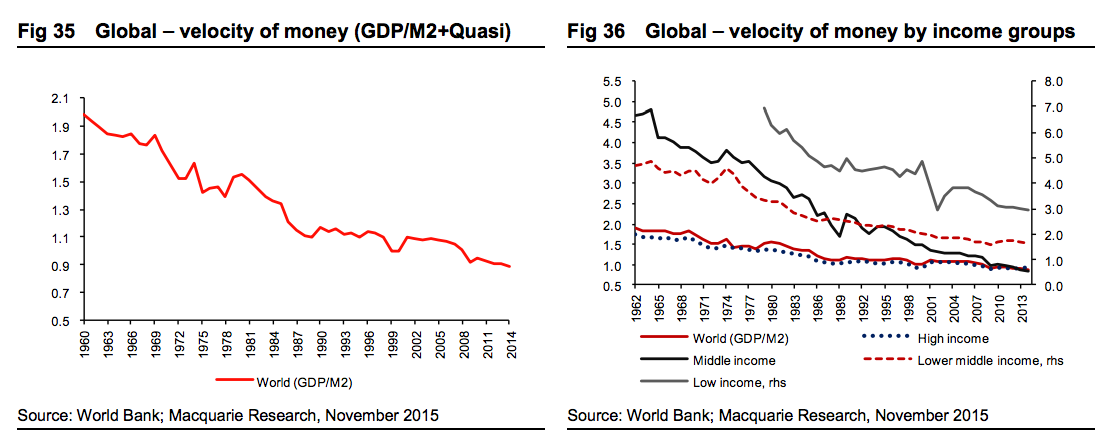

Whilst the World Bank tracks a broader concept of M2 (inclusive of quasi-cash, rather than our preferred narrower version), nevertheless, given that the overall trends are similar, it is interesting to note that upper middle-income countries now have a broadly similar velocity of money as developed nations and not dissimilar to global averages. However velocity of money remains much more robust in under-developed and under leveraged poorer nations.

Whilst some of the lower middle income and even upper middle income countries (under US$13,000 GDP per capita) are clearly not as leveraged as China, Malaysia or Thailand, it seems unlikely that much more than 15% of global demand (at best) currently resides in the regions of very low depth of financialization.

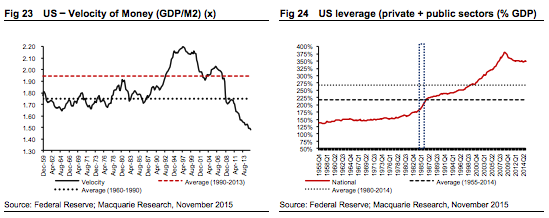

… global reflation is not possible without Fed. Unless velocity of money recovers and/or Fed embarks on QE4, global liquidity is likely to continue to erode; US$ is likely to appreciate, further compressing aggregate demand, trade and liquidity. Indeed, the more aggressive other CBs become (against tightening Fed), the greater would be the ultimate demand compression and stronger deflationary pressures.

Correct.