As we know, a Morgan Stanley upgrade to big miners triggered a surge in share price last in London. From Business Insider comes more:

“Emerging markets and China in particular remain key to commodities demand,” the team wrote in a note to clients.

“In the next few months we expect the perception around this demand to improve. In particular the acceleration of financial and administrative stimulus policies in China in recent weeks should start to feed through in both actual activity levels and equity market expectations.”

On the back of improving demand led by China, Morgan’s base case scenario is for commodity prices to rise by 14% in 2016 before accelerating by a further 19% in 2017.

“Using those forecasts we estimate 19% upside to our overweight-rated stocks,” they note.

“That would be a sharp reversal from the experience in the last 18 months. This should trigger a tactical re-rating of the sector.”

“Valuation is attractive in a historical context both at sector and company level. That means a change in perception around commodity prices can have a significant impact on the shares in our view,” Morgan’s wrote.

“The sector’s absolute trailing P/B of 0.85 and RoE of 7.9% is the lowest level since the global recession of 1982.”

Morgan Stanley suggests that with returns on capital and equity currently sitting at a four-decade low it will likely ensure supply discipline is maintained.

“Together with weaker project returns this drives large scale cut back of new projects even at the industry’s cost leaders.”

“Furthermore, some of the cost savings made across the industry will prove unsustainable in our view. This could trigger additional capacity exits when some costs reverse.”

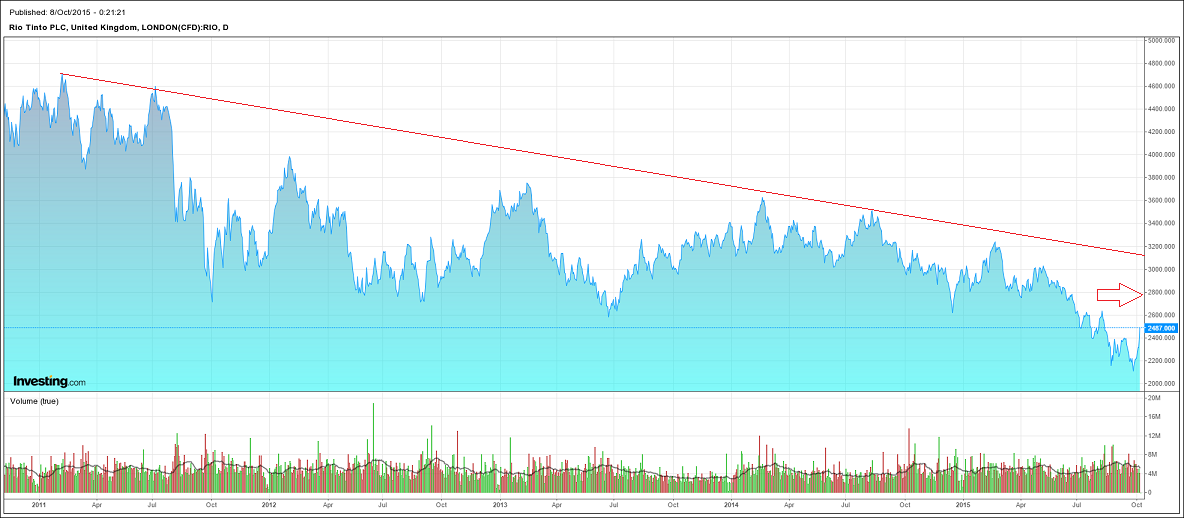

The key word here is “tactical”. In short, this is not a call to end the bear market. Indeed, a 19% gain in RIO would only take its London price to the arrow on the below chart:

That is far from the end of the bear market even if you agree with the analysis, which I do not.

As said already today, I am skeptical that we will see any rebound in China though I fully accept that it is possible for a few quarters before the glide slope resumes. Thus I find the notion that commodities can rise over the next two years very unlikely.

The choice of big miners is also odd. Big miners with exposure to iron ore are not going to benefit. Iron ore is toast regardless on supply expansions.

The only hope of any sustained rise in commodity prices is some kind of massive and open-ended QE4 not Chinese infrastructure stimulus.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

“Emerging markets and China in particular remain key to commodities demand,” the team wrote in a note to clients.

“Valuation is attractive in a historical context both at sector and company level. That means a change in perception around commodity prices can have a significant impact on the shares in our view,” Morgan’s wrote.