Australian Treasury Official, Roger Brake, gave an interesting speech late last week on tax reform and the major issues raised in submissions to Treasury’s “Tax White Paper”.

First, Brake outlined the reform imperative:

Tax reform can improve our economic productivity (and participation) and lead to a significant boost to living standards. Many argue it would lead to a bigger boost than any other single area of government policy.

But before I go into that, it is worth spelling out clearly why tax has negative economic effects. As a general rule, taxes impose costs on the economy by distorting the decisions of households, firms and investors. That is, they distort key economic choices – eg, about to engage in paid work or not; how much to save and in what form; how much to invest in skill acquisition. All real-world taxes impact some of these choices. A more efficient tax system is one that reduces these distortions from an economy-wide perspective.

He then gave Australia’s current tax structure a lousy score:

So, given that framework, how does our current system stack up? The short answer is not as well as it could.

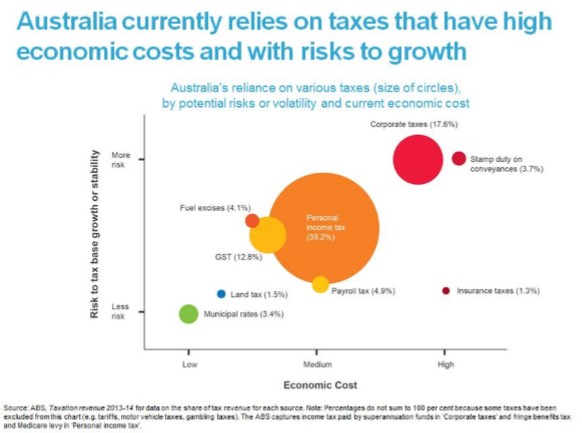

This is clear from the following chart.

This chart shows the economic cost of the more significant taxes in Australia. They could be roughly grouped into three categories in terms of economic efficiency.

Advertisement

Not surprisingly, Australia’s heavy reliance on stamp duties is making our tax system inherently inefficient:

Stamp duties are one of the most inefficient taxes levied in Australia. Unlike broad-based taxes on consumption or payrolls, stamp duties are applied to the total transaction value rather than the ‘value added’ component. Stamp duties, when expressed as a percentage of the economic value associated with a transaction, are actually levied at very high rates.

The economic cost of a tax increases with the square of the rate. So at high tax rates, stamp duties on conveyance have significant economic costs. On top of this, by discouraging the exchange and reallocation of residential and business property, stamp duties discourage the allocation of property to those who value it most. This distortion adds to the economic cost of stamp duties.

Other modelling also suggests that insurance taxes have high costs for a similar reason; it has very high effective rates.

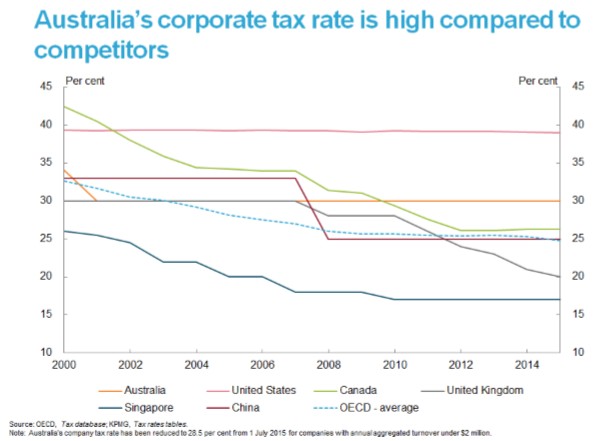

Australia’s high reliance on company taxes is also problematic:

Advertisement

Australia’s company tax rate is high by global standards, particularly given that many other countries have substantially reduced their corporate tax rates:

With this higher rate of company tax, Australia has a much greater reliance on company tax than comparable jurisdictions.

Why does our high company tax rate matter? It matters because it affects the level of investment into Australia, and in turn our stock of capital and productivity of workers. And as Paul Krugman says, productivity isn’t everything, but in the long run it is almost everything…

In the longer run, the higher capital stock [from lowering company taxes] would also lead to greater productivity and hence higher real wages for Australian workers. This contributes to an improvement in GDP and welfare.

Treasury has estimated that a reduction in the company income tax rate to 25 per cent, with a corresponding shift to more efficient taxes on labour or consumption, could generate long term gains to GDP of 1 per cent over 20 years. This is associated with an increase in real wages of around 1 per cent. Treasury also estimates that the second-round economic gains, although slow to accrue, would fund around 40 per cent of the direct revenue cost of a 25 per cent company tax rate…

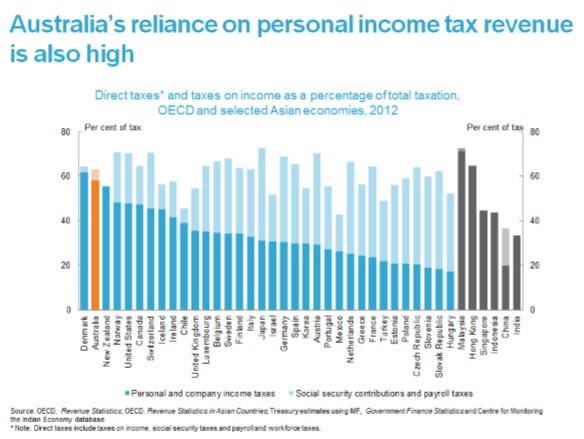

Brake also believes that Australia’s relies too much on personal income taxes:

High marginal tax rates, including through the interaction with the social security system, can dampen participation, investment in human and physical capital and entrepreneurship. Other countries rely much less than we do on progressive taxes, and more on flat rate consumption or social security taxes…

Brake also alludes to reform of Australia’s tax concessions, which need to be considered as a whole:

Advertisement

There are features in our tax system that are contentious. We have seen, for example, an active debate on issues like superannuation, negative gearing and dividend imputation. It is important these issues are considered from a broad perspective, and consultation is very important to achieve that. It is also important that the trade-off between changes in one part of the system with potential changes in other parts is considered. A tax preference in one area may be desirable, but is it more desirable than a reduction in tax elsewhere? Thus, in undertaking tax reform, reforms must also be assessed from a whole tax system perspective as there will always be interlinkages causing both positive and negative flow-on effects.

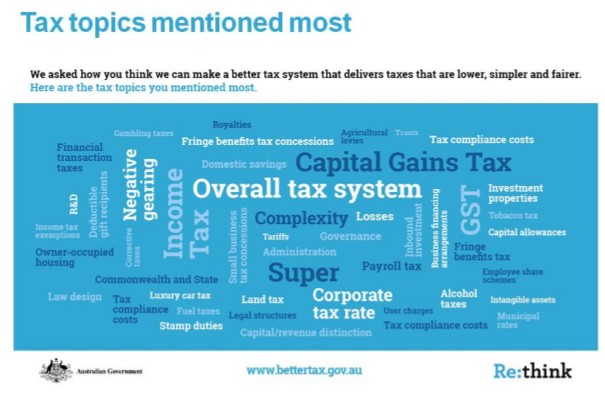

To date, the review has received 870 formal submissions – 470 from individuals and 400 from organisations.

The top areas of discussion are illustrated in the below Word Cloud:

Advertisement

The top five tax topics mentioned the most from submissions were superannuation, GST, income tax, the overall tax system, and capital gains tax (CGT).

Encouragingly, there is support for reducing existing superannuation concessions, but no clear agreement on how this should occur. Ditto CGT, where there is support for less concessional treatment.

Advertisement

There is also overwhelming support for the reduction/abolition of stamp duties, along with similar treatment for the different types of savings.

The next major step in the process is the release by the Government of the Options (Green) Paper. Treasury is assisting the Government work through the various options and choices which could be included.

Overall, the process looks promising, particularly given the reform-minded Malcolm Turnbull is now in charge.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.