If you want a prime example of why Australia’s pension means testing needs to be tightened, then look no further than the below example of a 73-year-old pensioner considering buying a second home for a relative:

Q: I am a single, 73-year-old pensioner. I am thinking about buying a second house to allow my relatives live in it rent free.

They kindly did the same for my family many years ago and are now struggling to pay their rent.

Is it a requirement of Centrelink to charge them rent?

A: Net income from real estate (after allowable deductions) is assessable income for social security purposes.

However, there is no requirement that a person use their property to produce income. If no money is received from a property, then no income is taken into account.

However, the net value of the property would be included in the customer’s assets test.

If they gave the property to somebody else, then the value (less up to $10,000) would be assessed as a deemed asset for five years and would fall under both the income test and the assets test.

The question that immediately springs to mind is: why is somebody that can afford to purchase a second home for a relative receiving the Aged Pension? Surely they are wealthy enough to look after themselves, rather than sucking from the taxpayer teet.

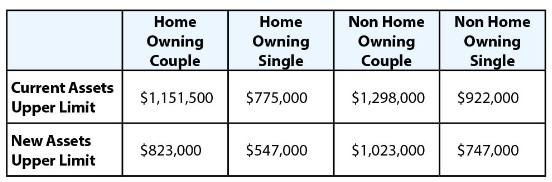

While the last Federal Budget did make some important reforms to thresholds for the Aged Pension, so that those with financial assets (in addition to the family home) of $547,000 for singles ($823,000 for couples) would no longer qualify for the part-pension (see below table).

It did not address the bigger issue of including one’s principal place of residence in the pension assets test.

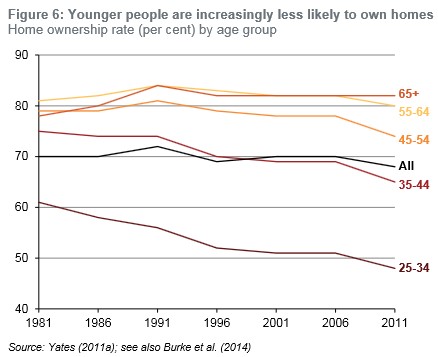

More than 80% of retirees own their homes (see next chart).

Therefore, it makes absolutely no sense that the biggest asset that most retirees hold – their principal place of residence – is excluded entirely from their eligibility for the Aged Pension, particularly given the massive increase in housing wealth that they have enjoyed.

It makes even less sense to expect younger Australians, whose home ownership rates are falling and many of whom will never be fortunate enough to own their homes, to continue subsidising oldies with significant assets. The irony of which is clear our flush pensioner’s offer to buy a home for someone that he has himself helped price out.

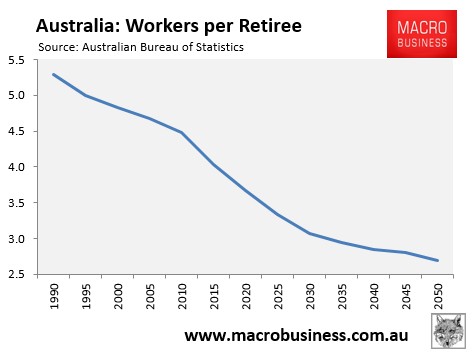

With the Aged Pension costing the Budget some $40 billion this financial year, growing by 7% annually, and the ratio of workers supporting the elderly shrinking (see next chart), the system as it stands is unsustainable and inequitable from an inter-generational perspective.

As argued by The Australian Institute, extending the Pension Loans Scheme to everybody of pension age would facilitate reform.

The Pension Loans Scheme is a state-run reverse mortgage scheme that allows eligible retirees to borrow against their homes to receive payments from the government equivalent to the full Aged Pension.

The interest rate through the Pension Loans Scheme is only around 5%, repayable upon their estate or sale. Therefore, home-owning retirees that no longer qualify for the Aged Pension could continue to receive income payments whilst living in their homes. For all intents and purposes, they would experience no change in their living standards, but with far less drain on the Budget.

If policy makers truly cared about equity, they would argue to have the family home included in the assets test for the Aged Pension, with part of the money saved redirected to increasing the base rate of the pension as well as the assets test threshold. This way, welfare would be far better targeted and those pensioners without any significant assets – either financial or non-financial – would be made far better-off.