New Zealand’s opposition housing spokesperson, Labour’s Phil Twyford, continues to impress.

Back in August, Twyford gave a brilliant sermon on how unaffordable housing is destroying the New Zealand economy, increasing inequality, and damaging the younger generations:

“The housing crisis is a disaster for the country; it’s driving up inequality and sucking vast amounts of investment into unproductive real estate speculation. No one wants to see Auckland house prices go bust. But the biggest risk to the Auckland property market is National’s hands off approach to the housing crisis which has allowed a bubble to develop in our biggest city.”

“John Key is happy to talk down concerns about the Auckland housing crisis because with the collapse of dairy prices and the Canterbury rebuild coming to an end, the bubble is all that’s left”…

“It’s a pretty cynical political calculation that there are enough home owners who stand to gain from Auckland’s housing crisis and skyrocketing house prices that he’s willing to throw under the bus the half of people in Auckland who are renters and a generation of young New Zealanders who are locked out of the housing market,” he said…

“There is a realisation this is bad for our families, bad for our kids, bad for our communities and bad for New Zealand. The Auckland housing economy that John Key is comfortable about is bad for the whole economy. We’re ploughing billions of dollars of capital into unproductive speculation in real estate and watching a generation of young New Zealanders being condemned to being renters and tenants in their own land in the Prime Minister’s words”…

“That’s the sort of Ponzi logic of this housing economy that John Key is comfortable with, and that’s why you can’t blame people under this Government’s housing policy for thinking that the only way to get rich in New Zealand is by speculating in residential property.”

Today, Twyford has appeared in the NZ Herald backing the Productivity Commission’s call to fund housing-related infrastructure through 30-year local government bonds, thus allowing development to be paid for over the lifetime of the infrastructure and not lumped onto the initial price of the home:

“There’s no question that given Auckland’s population growth trajectory and given what is currently a structural shortfall in housing — a deficit in the number of dwellings that is getting worse — that it must grow both out and up” [Twyford says]…

“If we were to reform the way we re-finance infrastructure, we could make a major difference in just a few steps”…

“When linking a new development to the network at the moment, some of the costs are charged to the developer in levies, but the bulk of it ends up being passed on to the end buyer and tacked on to the price of the house and subsequently the mortgage of that house”.

“What that does is pump up the price of the new house and it gets capitalised into the market value of all houses across the market. It’s an incredibly inefficient way to do things, it creates a barrier to home ownership and means infrastructure costs are funded at commercial banking rates on people’s mortgages”.

What Twyford is effectively arguing against is the “First-User-Pays-All Model”, which has been used to fund housing-related infrastructure in both New Zealand and Australia. This model replaced the old bond financing model in the 1990s, and has been a key roadblock to affordable greenfield development ever since.

As explained by regular MB reader, Pfh007, the First-User-Pays-All Model works as follows:

- Developers are forced to provide the long lasting housing infrastructure, that largely benefits the entire community;

- Developers then dump almost the entire cost on the first user of the land (usually a first home buyer), who then tries to pay for it with a jumbo-sized mortgage, much of which our banks borrow offshore;

- Local or state governments are then motivated to try to load as much expense on the home buyer as possible, and often also whack on a nice assortment of fat levies and contributions as well;

- The end result is a system that encourages gold plating and over charging when bringing land to market and forces the most vulnerable and less financially secure people pay the cost with hundreds of billions of foreign debt that requires a taxpayer guarantee.

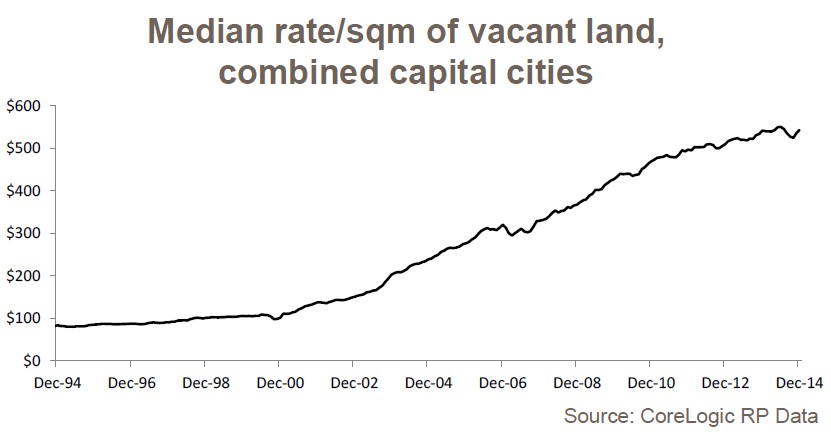

In Australia’s case, the First-User-Pays-All Model is a key reason why fringe lot values have experienced hyper-inflation over the past 15 years:

It is also why first home buyers are being gouged circa $500,000 to live in a basic 3 bedroom house 50 kms from Sydney and why there is almost no-demand for expensive new housing like this unless interest rates stay close to zero.

There has been similar price escalation across the pond in New Zealand, particularly in Auckland.

As noted by Twyford, instead of the First User Pays All model for financing development costs, a much smarter solution is for the government to pay the servicing and development costs of bringing the land to market and then recover part or all of the cost from rates or taxes on the land over the next 30 years.

If the government remains reluctant to fund such vital infrastructure, it could instead set up a Municipal Utility bond model (explained here and here), like the one operating in Houston Texas, and then let the growing pension fund (superannuation) sector do the funding. The returns will be secure if the rates/taxes are a first charge on the property, and the pension industry is begging for simple secure long term investments that generate a steady return.

Regardless, Phil Twyford appears to be one of those rare breeds of politicians that actually understands the housing issue. We could do with him in Australia.