How low are LNG prices going to fall? Real low, from the AFR:

The slump in liquefied natural gas prices still has further to go, even after plunging 60 per cent from last year’s peak, according to FGE, an energy consultant.

LNG prices may sink as low as $US4 ($5.60) per million British thermal units by 2017 because of a glut and probably won’t rise above $US8 before 2020, FGE chairman Fereidun Fesharaki said. That compares with the latest spot price of $US7.10 for LNG shipped to northeast Asia, according to Energy Intelligence Group.

“It’s an ugly environment,” Fesharaki said.

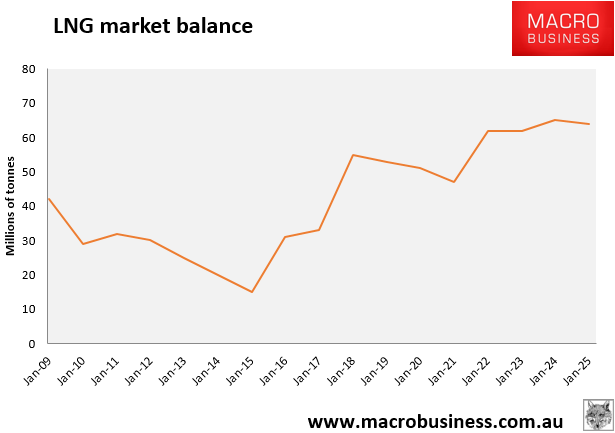

$5.60mmBtu is well below east coast cash costs and would result in volume cuts if sustained for any length of time. It would also be low enough to place immense pressure on contracts. On the upside, there’d be no east coast gas shock. The chart:

This is one reason why I said yesterday that the WPL bid for OSH is way overpriced, extraordinarily so given the sector is literally falling apart. From The Australian:

Woodside Petroleum is under pressure from investors to abandon its pursuit of smaller rival Oil Search amid fears a drastic increase in the takeover bid will savage the Perth-based company’s share price.

Oil Search’s board gave short shrift to an $11.6 billion all scrip offer earlier this month. The prevailing market view is that the figure needs to be lifted by at least 25 per cent, taking the price to $9.50 a share, for the deal to stand a chance of being consummated. But the prospect of a substantially higher bid has drawn an angry reaction from Woodside shareholders.

One large investor described the mooted increase as “financial suicide”, as it implies Oil Search’s scrip is more expensive than Woodside’s.

Rather than forge on, he argued Australia’s largest oil and gas player should walk away from the bid. “This is a more plausible scenario,” he said.

WPL is still twice the value of OSH so I’m not sure where that comes from. Nonetheless, WPL has a clean balance sheet and will have the pick of the wreckage before too long but has instead moved too early, strategically wedging itself in the process. The bid suggests that it sees the market somewhere near the bottom but it also intrinsically undermines its commitment to brown fields development so Browse is now an open question (or wound).

The share price is now going to fall if it proceeds or withdraws from the bid. It was going to fall anyway but there was no need to push it (it’s up today on the oil rebound).