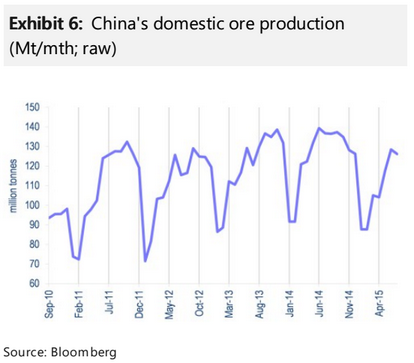

[Chinese] ore production: official data suggest raw ore production is down 13% yoy to 1300Mt (all on a seaborne grade eqv. basis, there’s at least 50Mt of production cut;currently producing at about 250Mtpa):

This is tracking 3% better (for Oz) than I was expecting and helps explain some of the recent price firmness in iron ore, knocking out an extra 10-20mtpa than my forecast.

The other major two factors are miner market manipulation and low Chinese port stocks. I still expect price erosion into year end and no seasonal restock.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.