By Redom Syed, republished with permission from Property Chat:

Last week the APRA chairman delivered a telling speech about the future of the lending market in Australia.

The speech was the best public indication yet of what APRA is thinking, what they have done and what they’re likely to do next. Importantly, they also provided insights into the timeframe for some of the changes that have been implemented.

How did people grow large portfolios before APRA?

One of APRA’s primary concerns has been investor’s borrowing capacity.

In the pre-APRA environment, you could work out their borrowing power with an individual lender, and then ‘recycle’ that borrowing power over and over again by simply switching lenders. This is what some brokers called the ‘finance multiplier’.

The overall ‘multiplier’ meant investors had the capacity to potentially grow portfolios 4-5 times the amount of an individual calculator amount.

Individual lender borrowing X Finance Multiplier = Overall potential portfolio value

For example, if ANZ said you could borrow $1million, a quick back of the envelope calculation for your potential ‘portfolio value’ would be above $4-5 million. To do this, you’d need some good loan structuring, effective switching of lenders, utilising interest only loans, a 5-6% yield and historically low interest rates. More on this is available in this post.

APRA got wind of all of this, and worried about the build up of risk that investors may be taking on.

So, what did APRA do to serviceability?

A bank works out your borrowing power by calculating your income and subtracting your ‘assessed’ expenses. The left over balance is then used to calculate your borrowing power.

APRA have targeted the ‘assessed’ expense. Note that as a general rule, for every $1 that your expenses increase by, your borrowing power falls by ~$12.

APRA initiated four main changes to serviceability calculators over the last quarter.

- Increases to living expenses calculations that are tiered by income/location.

- Changes to the treatment of your existing mortgage debt held with other banks (OFI). This is the big one for investors!

- Higher effective assessment rates applied for interest only loans.

- They have also asked lenders to discount non-consistent income (overtime, etc).

What do the APRA changes mean?

Well, both aspects of your potential borrowing power have taken a hit:

- Your borrowing power with individual lenders has fallen sharply.

- Your borrowing ‘multiplier’ has fallen; it’s typically more difficult to ‘recycle’ your borrowing power and have a multiplier of 4+.

How has an individual’s borrowing power fallen?

The simplest way to work this out is to break down individual APRA changes, and then add them together to work out the total effect on you.

While everyone’s situation will be different, in the next post [below], I have provided a visual representation of how APRAs changes could effect investors. Its purpose is to provide a general picture on what APRA have done, so speak to your broker for individualised advice.

What is the ‘finance multiplier’ now?

Significantly lower than in the past and its become a little more complex in a world where there aren’t any ‘actual repayment’ lenders, but I’d say somewhere around 1.5-2 (excluding small lenders who may change policies soon).

Did his speech indicate how long these will last?

Yes, but unfortunately there’s not much good news to tell here. APRA made very clear references to the fact that these changes are part of prudent lending in ALL environments and represent good behaviour.

Some references from his speech:

· APRA were ‘puzzled’ by lender calculations of OFI debt

- Code for – are you kidding banks, you took actual repayments? How irresponsible is that!

· ‘Sound lending standards – prudent estimating of borrower income and expenses…are just as important in an environment where price growth is subdued as they are in markets where prices are rising quickly’

- Code for – THESE CHANGES ARE HERE TO STAY.

Did his speech indicate what APRA will do next?

Yes, he specifically mentioned that the changes are relatively recent and it is still too early to see if further intervention is necessary. The aim of these changes is to simply slow the growth of investment lending down, rather than to stop the growth altogether.

So its very much a ‘wait and see’ from here.

He did for the first time publicly flag the possibility of geographic based measures. He also basically ruled out LVR based intervention, showing that it’s not a problem in Australia.

What risks does this mean for borrowers?

I’ve talked about some of the risks while growing a portfolio, particularly on extending interest only terms. Given this latest insight, I’d recommend increasing buffers, as the chances of borrowing power policy reverting back just got a bit smaller.

Furthermore, brokers are seeing more and more unusual ‘risk based’ outcomes from lenders now.

What should a borrower do?

The ‘permanence’ of these changes should be factored into your strategies. Brokers have had to become proactive by seeking alternative strategies for their clients, seeking out new funding lines (there’s a few credit unions out there that have great calculators), repositioning advice to longer term goals, forming active capital/income transitions, etc.

In this new environment you can still grow large portfolios and achieve your property goals – it just might require creating solutions and tweaking strategies to maneuverer around APRAs changes.

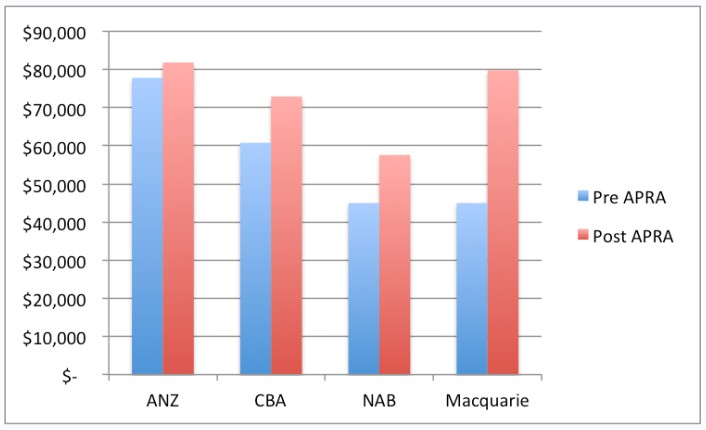

Chart 1, OFI debt – Change in the yearly expense number banks take for $1 million worth of debt held with another financial institution

With $1million worth of debt, Macquarie have increased your ‘assessed’ expense from ~$45,000 per year to around $80,000. A $35,000 p.a. increase in your expenses!

This means, that if you have $1million worth of debt with Westpac, your borrowing power with Macquarie is over $400,000 lower today because of this change.

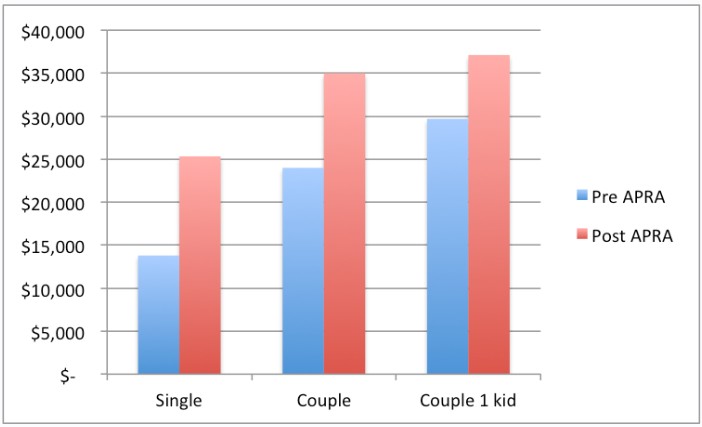

Chart 2, Living Expenses – How ‘assessed living expenses’ the banks take have increased per annum, broken down by household type

The minimum living expense that lenders use for single person earning more than $73k has nearly doubled. This has reduced their borrowing power by over $130k.

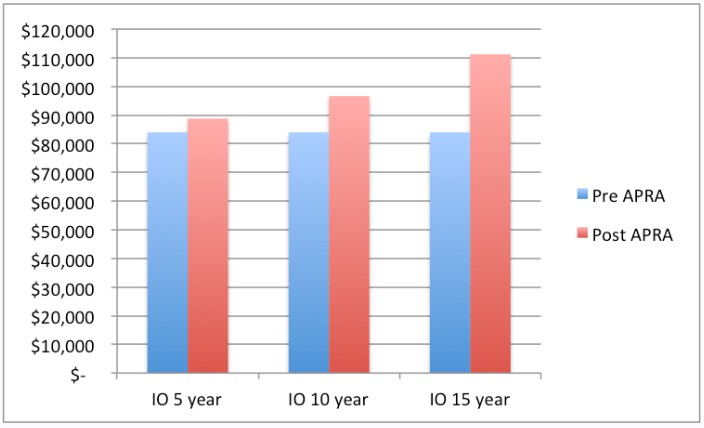

Chart 3 – Interest Only terms have also increased your yearly assessable expenses

Previously, lenders calculated your ‘assessed repayments’ on P&I terms, so essentially 30 years of P&I repayments in most cases.

However, lenders now discount the loan term by any IO period. This means the ‘assessed repayments’ on IO debt are now calculated over a shorter loan term and thus have higher ‘assessed repayments’.

For example, based on $1 million worth of lending on 5 year IO terms, your assessable repayments have increased by ~$5000 p.a. and reduced your borrowing power by ~$60,000.

The longer the interest only period on the debt you hold, the greater the reduction in your borrowing power.

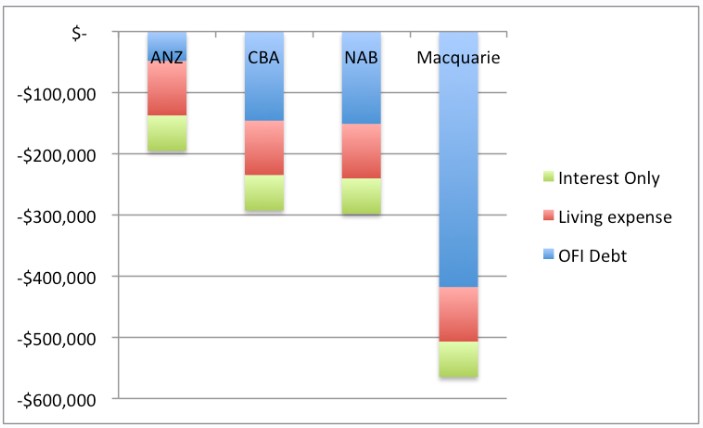

Chart 4 – Overall reduction in borrowing power broken down by certain lenders

This chart shows how these changes can combine together to affect your borrowing power. I’ve used a hypothetical test case, a couple with 1 dependant and $1 million worth of existing debt on 5 year IO terms.

The chart breaks down how this investors borrowing power has fallen with different lenders. Please note that for simplicity, I’ve assumed each lender has symmetrical treatment of living expenses and IO debt. In reality each lender treats these slightly differently, but they are becoming more closely aligned over time.

Obviously everyone’s circumstances are unique but hopefully this steps out how these ‘market level’ changes flow through to individual deals. Like I said in the first post, with the right advice and strategies growing a large portfolio is still very achievable!