$50/t short-term target; larger shake-out expected in 1H16 – Chinese iron ore inventories are once again rising on the back of improving Australian exports, which we expect to pressure prices lower to around $50/t over the next two months.

However, a true shake-out will need to await Chinese steel mills giving way. We expect a combination of such cutbacks and continued supply growth to push prices below $40/t in the first half of 2016.

Iron ore demand is expected to remain relatively stable in the short-term – Despite contracting domestic demand and some of the worst steel margins ever, steel production has remained relatively stable. Mills are focused on preserving cash flow and the short-term drivers of steel production have shifted to balance sheet and financing considerations. We expect output to remain relatively steady over the next two months, but for production to fall significantly in Q1.

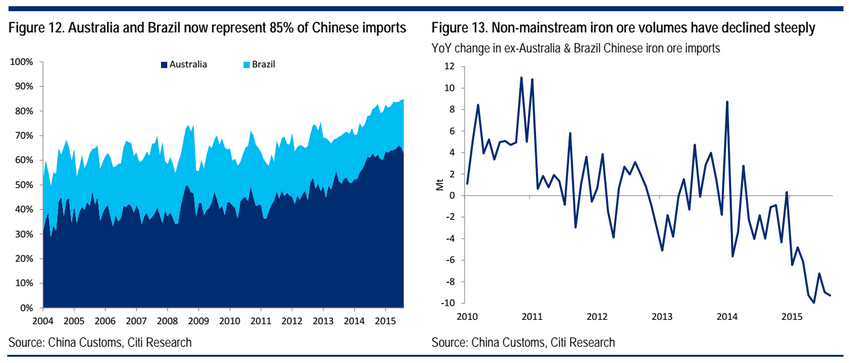

Supply has been volatile but has improved and major capacity is still to come – Supply is increasingly concentrated amongst Australia and Brazil, which now account for 85% of Chinese imports. Volatility in Australian exports has been the #1 driver of iron ore prices this year and volumes are now increasing. First shipments from Roy Hill are expected in October, with its ramp-up likely to have a large price impact. Risks also come from the resumption of mining in Goa and Tonkolili.

Lump and pellet premiums have declined sharply – Lumps have been hit particularly hard, falling from $23/t in March to $4/t currently. The declines have largely been driven by increased supply, but also by soft demand for quality products from Chinese mills. We expect premiums to recover into year-end, but largely on seasonal factors, and for strong growth of both products to keep premiums capped in 2016.

The market share battle shows why there has been a little pricing power for major miners over recent months. But with the Roy Hill “whale” swimming in and a Tonkolili resumption I have to say that $40 is conservative.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.