From The AFR’s Karen Maley comes a report that China’s authorities are stepping-up action to prevent money from being illegally transferred out of the country:

On Tuesday, the People’s Bank of China, announced changes that will make it more expensive for investors to hedge against further drops in the Chinese yuan against the US dollar.

At the same time, China’s largest banks are stepping up their checks on large foreign-exchange conversions by corporate clients, while China’s financial regulators are targeting illegal money-transfer agents who help wealthy Chinese transfer funds out of the country…

And Chinese officials are cracking down on underground banks that help Chinese nationals to shift money out of the country…

Already-affluent Chinese investors, worried by the oversupply problems in the Chinese property market, the country’s volatile sharemarket and Beijing’s crackdown on corruption, have been sending large amounts of money offshore.

Earlier this year, the Paris-based Financial Action Task Force (FATF) on money laundering warned that Australian residential property is a haven for international money laundering, particularly from China – a view supported by the Australian Transaction Reports and Analysis Centre (AUSTRAC).

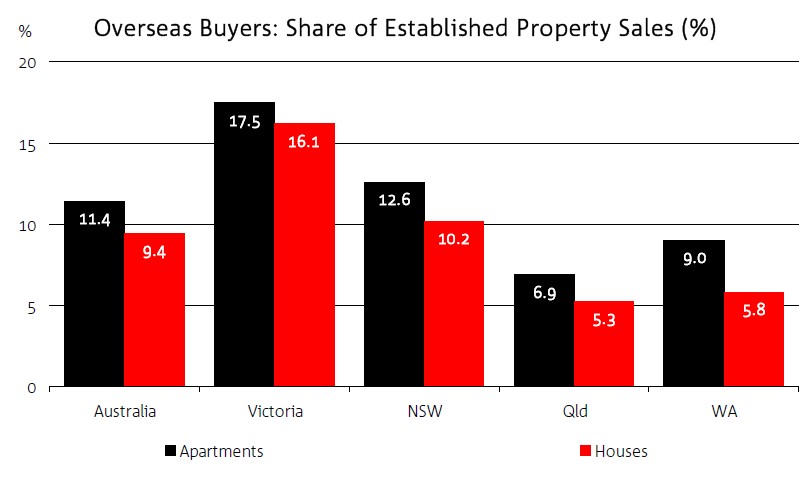

We also know that foreign buyers – especially from China – are active in Australian real estate, particularly in Melbourne and Sydney:

If China’s authorities are successful is stemming the tide of illegal money transfers, then it would obviously reduce the amount of overseas funds flowing into Australian property, thereby reducing price pressures and potentially exacerbating the inevitable housing downturn.

unconventionaleconomist@hotmail.com